Python时间序列分析

时间序列与时间序列分析

在生产和科学研究中,对某一个或者一组变量 进行观察测量,将在一系列时刻所得到的离散数字组成的序列集合,称之为时间序列。

时间序列分析是根据系统观察得到的时间序列数据,通过曲线拟合和参数估计来建立数学模型的理论和方法。时间序列分析常用于国民宏观经济控制、市场潜力预测、气象预测、农作物害虫灾害预报等各个方面。

Pandas生成时间序列:

1 2 | import pandas as pdimport numpy as np |

时间序列

- 时间戳(timestamp)

- 固定周期(period)

- 时间间隔(interval)

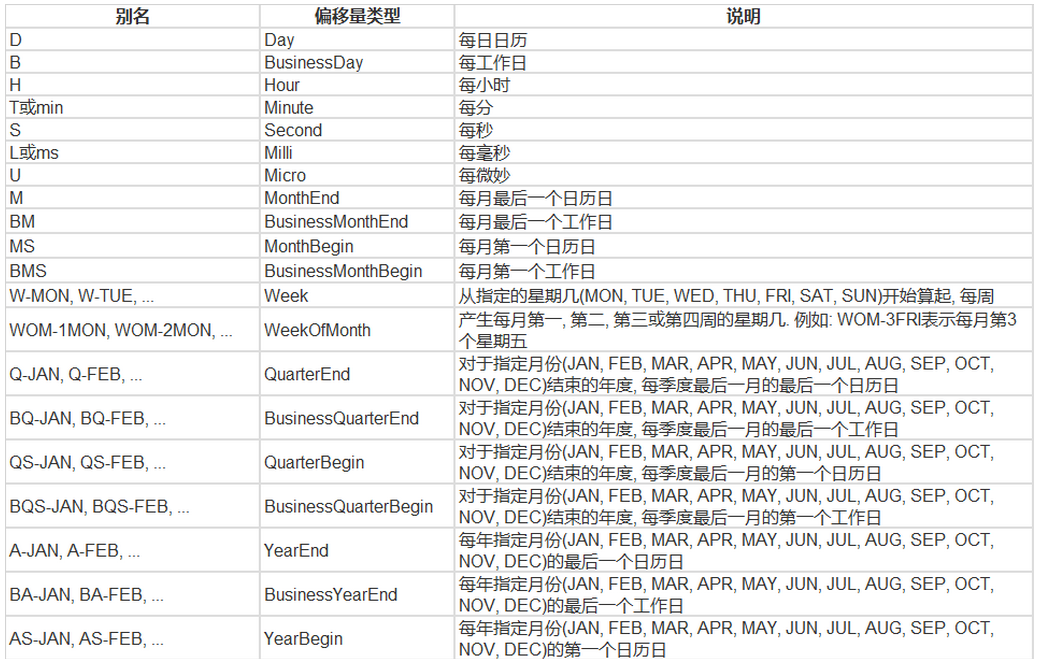

date_range

- 可以指定开始时间与周期

- H:小时

- D:天

- M:月

1 2 3 | # TIMES的几种书写方式 #2016 Jul 1; 7/1/2016; 1/7/2016 ;2016-07-01; 2016/07/01rng = pd.date_range('2016-07-01', periods = 10, freq = '3D')#不传freq则默认是Drng |

结果:

DatetimeIndex(['2016-07-01', '2016-07-04', '2016-07-07', '2016-07-10', '2016-07-13', '2016-07-16', '2016-07-19', '2016-07-22', '2016-07-25', '2016-07-28'], dtype='datetime64[ns]', freq='3D')

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 | time=pd.Series(np.random.randn(20), index=pd.date_range(dt.datetime(2016,1,1),periods=20))print(time)#结果:2016-01-01 -0.1293792016-01-02 0.1644802016-01-03 -0.6391172016-01-04 -0.4272242016-01-05 2.0551332016-01-06 1.1160752016-01-07 0.3574262016-01-08 0.2742492016-01-09 0.8344052016-01-10 -0.0054442016-01-11 -0.1344092016-01-12 0.2493182016-01-13 -0.2978422016-01-14 -0.1285142016-01-15 0.0636902016-01-16 -2.2460312016-01-17 0.3595522016-01-18 0.3830302016-01-19 0.4027172016-01-20 -0.694068Freq: D, dtype: float64 |

truncate过滤

1 | time.truncate(before='2016-1-10')#1月10之前的都被过滤掉了 |

结果:

2016-01-10 -0.005444

2016-01-11 -0.134409

2016-01-12 0.249318

2016-01-13 -0.297842

2016-01-14 -0.128514

2016-01-15 0.063690

2016-01-16 -2.246031

2016-01-17 0.359552

2016-01-18 0.383030

2016-01-19 0.402717

2016-01-20 -0.694068

Freq: D, dtype: float64

1 2 3 4 5 6 7 8 9 10 11 12 13 | time.truncate(after='2016-1-10')#1月10之后的都被过滤掉了#结果:2016-01-01 -0.1293792016-01-02 0.1644802016-01-03 -0.6391172016-01-04 -0.4272242016-01-05 2.0551332016-01-06 1.1160752016-01-07 0.3574262016-01-08 0.2742492016-01-09 0.8344052016-01-10 -0.005444Freq: D, dtype: float64 |

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 | print(time['2016-01-15'])#0.063690487247print(time['2016-01-15':'2016-01-20'])结果:2016-01-15 0.0636902016-01-16 -2.2460312016-01-17 0.3595522016-01-18 0.3830302016-01-19 0.4027172016-01-20 -0.694068Freq: D, dtype: float64data=pd.date_range('2010-01-01','2011-01-01',freq='M')print(data)#结果:DatetimeIndex(['2010-01-31', '2010-02-28', '2010-03-31', '2010-04-30', '2010-05-31', '2010-06-30', '2010-07-31', '2010-08-31', '2010-09-30', '2010-10-31', '2010-11-30', '2010-12-31'], dtype='datetime64[ns]', freq='M') |

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100 101 102 103 104 105 106 107 108 109 110 | #时间戳pd.Timestamp('2016-07-10')#Timestamp('2016-07-10 00:00:00')# 可以指定更多细节pd.Timestamp('2016-07-10 10')#Timestamp('2016-07-10 10:00:00')pd.Timestamp('2016-07-10 10:15')#Timestamp('2016-07-10 10:15:00')# How much detail can you add?t = pd.Timestamp('2016-07-10 10:15')# 时间区间pd.Period('2016-01')#Period('2016-01', 'M')pd.Period('2016-01-01')#Period('2016-01-01', 'D')# TIME OFFSETSpd.Timedelta('1 day')#Timedelta('1 days 00:00:00')pd.Period('2016-01-01 10:10') + pd.Timedelta('1 day')#Period('2016-01-02 10:10', 'T')pd.Timestamp('2016-01-01 10:10') + pd.Timedelta('1 day')#Timestamp('2016-01-02 10:10:00')pd.Timestamp('2016-01-01 10:10') + pd.Timedelta('15 ns')#Timestamp('2016-01-01 10:10:00.000000015')p1 = pd.period_range('2016-01-01 10:10', freq = '25H', periods = 10)p2 = pd.period_range('2016-01-01 10:10', freq = '1D1H', periods = 10)p1p2结果:PeriodIndex(['2016-01-01 10:00', '2016-01-02 11:00', '2016-01-03 12:00', '2016-01-04 13:00', '2016-01-05 14:00', '2016-01-06 15:00', '2016-01-07 16:00', '2016-01-08 17:00', '2016-01-09 18:00', '2016-01-10 19:00'], dtype='period[25H]', freq='25H')PeriodIndex(['2016-01-01 10:00', '2016-01-02 11:00', '2016-01-03 12:00', '2016-01-04 13:00', '2016-01-05 14:00', '2016-01-06 15:00', '2016-01-07 16:00', '2016-01-08 17:00', '2016-01-09 18:00', '2016-01-10 19:00'], dtype='period[25H]', freq='25H')# 指定索引rng = pd.date_range('2016 Jul 1', periods = 10, freq = 'D')rngpd.Series(range(len(rng)), index = rng)结果:2016-07-01 02016-07-02 12016-07-03 22016-07-04 32016-07-05 42016-07-06 52016-07-07 62016-07-08 72016-07-09 82016-07-10 9Freq: D, dtype: int32periods = [pd.Period('2016-01'), pd.Period('2016-02'), pd.Period('2016-03')]ts = pd.Series(np.random.randn(len(periods)), index = periods)ts结果:2016-01 -0.0158372016-02 -0.9234632016-03 -0.485212Freq: M, dtype: float64type(ts.index)#pandas.core.indexes.period.PeriodIndex# 时间戳和时间周期可以转换ts = pd.Series(range(10), pd.date_range('07-10-16 8:00', periods = 10, freq = 'H'))ts结果:2016-07-10 08:00:00 02016-07-10 09:00:00 12016-07-10 10:00:00 22016-07-10 11:00:00 32016-07-10 12:00:00 42016-07-10 13:00:00 52016-07-10 14:00:00 62016-07-10 15:00:00 72016-07-10 16:00:00 82016-07-10 17:00:00 9Freq: H, dtype: int32ts_period = ts.to_period()ts_period结果:2016-07-10 08:00 02016-07-10 09:00 12016-07-10 10:00 22016-07-10 11:00 32016-07-10 12:00 42016-07-10 13:00 52016-07-10 14:00 62016-07-10 15:00 72016-07-10 16:00 82016-07-10 17:00 9Freq: H, dtype: int32时间周期与时间戳的区别ts_period['2016-07-10 08:30':'2016-07-10 11:45'] #时间周期包含08:00结果:2016-07-10 08:00 02016-07-10 09:00 12016-07-10 10:00 22016-07-10 11:00 3Freq: H, dtype: int32ts['2016-07-10 08:30':'2016-07-10 11:45'] #时间戳不包含08:30#结果:2016-07-10 09:00:00 12016-07-10 10:00:00 22016-07-10 11:00:00 3Freq: H, dtype: int32 |

数据重采样:

- 时间数据由一个频率转换到另一个频率

- 降采样

- 升采样

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100 101 102 103 104 105 106 107 108 109 110 111 112 113 114 115 116 117 118 119 120 121 122 123 124 125 126 127 128 129 130 131 132 133 134 135 136 137 138 139 140 141 142 143 144 145 146 147 148 149 150 151 152 153 | import pandas as pdimport numpy as nprng = pd.date_range('1/1/2011', periods=90, freq='D')#数据按天ts = pd.Series(np.random.randn(len(rng)), index=rng)ts.head()结果:2011-01-01 -1.0255622011-01-02 0.4108952011-01-03 0.6603112011-01-04 0.7102932011-01-05 0.444985Freq: D, dtype: float64ts.resample('M').sum()#数据降采样,降为月,指标是求和,也可以平均,自己指定结果:2011-01-31 2.5101022011-02-28 0.5832092011-03-31 2.749411Freq: M, dtype: float64ts.resample('3D').sum()#数据降采样,降为3天结果:2011-01-01 0.0456432011-01-04 -2.2552062011-01-07 0.5711422011-01-10 0.8350322011-01-13 -0.3967662011-01-16 -1.1562532011-01-19 -1.2868842011-01-22 2.8839522011-01-25 1.5669082011-01-28 1.4355632011-01-31 0.3115652011-02-03 -2.5412352011-02-06 0.3170752011-02-09 1.5988772011-02-12 -1.9505092011-02-15 2.9283122011-02-18 -0.7337152011-02-21 1.6748172011-02-24 -2.0788722011-02-27 2.1723202011-03-02 -2.0221042011-03-05 -0.0703562011-03-08 1.2766712011-03-11 -2.8351322011-03-14 -1.3841132011-03-17 1.5175652011-03-20 -0.5504062011-03-23 0.7734302011-03-26 2.2443192011-03-29 2.951082Freq: 3D, dtype: float64day3Ts = ts.resample('3D').mean()day3Ts结果:2011-01-01 0.0152142011-01-04 -0.7517352011-01-07 0.1903812011-01-10 0.2783442011-01-13 -0.1322552011-01-16 -0.3854182011-01-19 -0.4289612011-01-22 0.9613172011-01-25 0.5223032011-01-28 0.4785212011-01-31 0.1038552011-02-03 -0.8470782011-02-06 0.1056922011-02-09 0.5329592011-02-12 -0.6501702011-02-15 0.9761042011-02-18 -0.2445722011-02-21 0.5582722011-02-24 -0.6929572011-02-27 0.7241072011-03-02 -0.6740352011-03-05 -0.0234522011-03-08 0.4255572011-03-11 -0.9450442011-03-14 -0.4613712011-03-17 0.5058552011-03-20 -0.1834692011-03-23 0.2578102011-03-26 0.7481062011-03-29 0.983694Freq: 3D, dtype: float64print(day3Ts.resample('D').asfreq())#升采样,要进行插值结果:2011-01-01 0.0152142011-01-02 NaN2011-01-03 NaN2011-01-04 -0.7517352011-01-05 NaN2011-01-06 NaN2011-01-07 0.1903812011-01-08 NaN2011-01-09 NaN2011-01-10 0.2783442011-01-11 NaN2011-01-12 NaN2011-01-13 -0.1322552011-01-14 NaN2011-01-15 NaN2011-01-16 -0.3854182011-01-17 NaN2011-01-18 NaN2011-01-19 -0.4289612011-01-20 NaN2011-01-21 NaN2011-01-22 0.9613172011-01-23 NaN2011-01-24 NaN2011-01-25 0.5223032011-01-26 NaN2011-01-27 NaN2011-01-28 0.4785212011-01-29 NaN2011-01-30 NaN ... 2011-02-28 NaN2011-03-01 NaN2011-03-02 -0.6740352011-03-03 NaN2011-03-04 NaN2011-03-05 -0.0234522011-03-06 NaN2011-03-07 NaN2011-03-08 0.4255572011-03-09 NaN2011-03-10 NaN2011-03-11 -0.9450442011-03-12 NaN2011-03-13 NaN2011-03-14 -0.4613712011-03-15 NaN2011-03-16 NaN2011-03-17 0.5058552011-03-18 NaN2011-03-19 NaN2011-03-20 -0.1834692011-03-21 NaN2011-03-22 NaN2011-03-23 0.2578102011-03-24 NaN2011-03-25 NaN2011-03-26 0.7481062011-03-27 NaN2011-03-28 NaN2011-03-29 0.983694Freq: D, Length: 88, dtype: float64 |

插值方法:

- ffill 空值取前面的值

- bfill 空值取后面的值

- interpolate 线性取值

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100 101 102 103 104 105 106 107 108 109 110 111 112 113 114 115 116 117 118 119 120 121 122 123 124 125 126 127 128 129 130 131 132 133 134 135 136 137 138 139 140 141 142 143 144 145 146 147 148 149 150 151 152 153 154 155 156 157 158 159 160 161 162 163 164 165 166 167 168 169 170 171 172 173 174 175 176 177 178 179 180 181 182 183 184 185 186 187 188 189 190 191 192 193 194 | day3Ts.resample('D').ffill(1)结果:2011-01-01 0.0152142011-01-02 0.0152142011-01-03 NaN2011-01-04 -0.7517352011-01-05 -0.7517352011-01-06 NaN2011-01-07 0.1903812011-01-08 0.1903812011-01-09 NaN2011-01-10 0.2783442011-01-11 0.2783442011-01-12 NaN2011-01-13 -0.1322552011-01-14 -0.1322552011-01-15 NaN2011-01-16 -0.3854182011-01-17 -0.3854182011-01-18 NaN2011-01-19 -0.4289612011-01-20 -0.4289612011-01-21 NaN2011-01-22 0.9613172011-01-23 0.9613172011-01-24 NaN2011-01-25 0.5223032011-01-26 0.5223032011-01-27 NaN2011-01-28 0.4785212011-01-29 0.4785212011-01-30 NaN ... 2011-02-28 0.7241072011-03-01 NaN2011-03-02 -0.6740352011-03-03 -0.6740352011-03-04 NaN2011-03-05 -0.0234522011-03-06 -0.0234522011-03-07 NaN2011-03-08 0.4255572011-03-09 0.4255572011-03-10 NaN2011-03-11 -0.9450442011-03-12 -0.9450442011-03-13 NaN2011-03-14 -0.4613712011-03-15 -0.4613712011-03-16 NaN2011-03-17 0.5058552011-03-18 0.5058552011-03-19 NaN2011-03-20 -0.1834692011-03-21 -0.1834692011-03-22 NaN2011-03-23 0.2578102011-03-24 0.2578102011-03-25 NaN2011-03-26 0.7481062011-03-27 0.7481062011-03-28 NaN2011-03-29 0.983694Freq: D, Length: 88, dtype: float64day3Ts.resample('D').bfill(1)结果:2011-01-01 0.0152142011-01-02 NaN2011-01-03 -0.7517352011-01-04 -0.7517352011-01-05 NaN2011-01-06 0.1903812011-01-07 0.1903812011-01-08 NaN2011-01-09 0.2783442011-01-10 0.2783442011-01-11 NaN2011-01-12 -0.1322552011-01-13 -0.1322552011-01-14 NaN2011-01-15 -0.3854182011-01-16 -0.3854182011-01-17 NaN2011-01-18 -0.4289612011-01-19 -0.4289612011-01-20 NaN2011-01-21 0.9613172011-01-22 0.9613172011-01-23 NaN2011-01-24 0.5223032011-01-25 0.5223032011-01-26 NaN2011-01-27 0.4785212011-01-28 0.4785212011-01-29 NaN2011-01-30 0.103855 ... 2011-02-28 NaN2011-03-01 -0.6740352011-03-02 -0.6740352011-03-03 NaN2011-03-04 -0.0234522011-03-05 -0.0234522011-03-06 NaN2011-03-07 0.4255572011-03-08 0.4255572011-03-09 NaN2011-03-10 -0.9450442011-03-11 -0.9450442011-03-12 NaN2011-03-13 -0.4613712011-03-14 -0.4613712011-03-15 NaN2011-03-16 0.5058552011-03-17 0.5058552011-03-18 NaN2011-03-19 -0.1834692011-03-20 -0.1834692011-03-21 NaN2011-03-22 0.2578102011-03-23 0.2578102011-03-24 NaN2011-03-25 0.7481062011-03-26 0.7481062011-03-27 NaN2011-03-28 0.9836942011-03-29 0.983694Freq: D, Length: 88, dtype: float64day3Ts.resample('D').interpolate('linear')#线性拟合填充结果:2011-01-01 0.0152142011-01-02 -0.2404352011-01-03 -0.4960852011-01-04 -0.7517352011-01-05 -0.4376972011-01-06 -0.1236582011-01-07 0.1903812011-01-08 0.2197022011-01-09 0.2490232011-01-10 0.2783442011-01-11 0.1414782011-01-12 0.0046112011-01-13 -0.1322552011-01-14 -0.2166432011-01-15 -0.3010302011-01-16 -0.3854182011-01-17 -0.3999322011-01-18 -0.4144472011-01-19 -0.4289612011-01-20 0.0344652011-01-21 0.4978912011-01-22 0.9613172011-01-23 0.8149792011-01-24 0.6686412011-01-25 0.5223032011-01-26 0.5077092011-01-27 0.4931152011-01-28 0.4785212011-01-29 0.3536322011-01-30 0.228744 ... 2011-02-28 0.2580602011-03-01 -0.2079882011-03-02 -0.6740352011-03-03 -0.4571742011-03-04 -0.2403132011-03-05 -0.0234522011-03-06 0.1262182011-03-07 0.2758872011-03-08 0.4255572011-03-09 -0.0313102011-03-10 -0.4881772011-03-11 -0.9450442011-03-12 -0.7838202011-03-13 -0.6225952011-03-14 -0.4613712011-03-15 -0.1389622011-03-16 0.1834462011-03-17 0.5058552011-03-18 0.2760802011-03-19 0.0463062011-03-20 -0.1834692011-03-21 -0.0363762011-03-22 0.1107172011-03-23 0.2578102011-03-24 0.4212422011-03-25 0.5846742011-03-26 0.7481062011-03-27 0.8266362011-03-28 0.9051652011-03-29 0.983694Freq: D, Length: 88, dtype: float64 |

Pandas滑动窗口:

滑动窗口就是能够根据指定的单位长度来框住时间序列,从而计算框内的统计指标。相当于一个长度指定的滑块在刻度尺上面滑动,每滑动一个单位即可反馈滑块内的数据。

滑动窗口可以使数据更加平稳,浮动范围会比较小,具有代表性,单独拿出一个数据可能或多或少会离群,有差异或者错误,使用滑动窗口会更规范一些。

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 | %matplotlib inline import matplotlib.pylabimport numpy as npimport pandas as pddf = pd.Series(np.random.randn(600), index = pd.date_range('7/1/2016', freq = 'D', periods = 600))df.head()结果:2016-07-01 -0.1921402016-07-02 0.3579532016-07-03 -0.2018472016-07-04 -0.3722302016-07-05 1.414753Freq: D, dtype: float64r = df.rolling(window = 10)r#Rolling [window=10,center=False,axis=0]#r.max, r.median, r.std, r.skew倾斜度, r.sum, r.varprint(r.mean())结果:2016-07-01 NaN2016-07-02 NaN2016-07-03 NaN2016-07-04 NaN2016-07-05 NaN2016-07-06 NaN2016-07-07 NaN2016-07-08 NaN2016-07-09 NaN2016-07-10 0.3001332016-07-11 0.2847802016-07-12 0.2528312016-07-13 0.2206992016-07-14 0.1671372016-07-15 0.0185932016-07-16 -0.0614142016-07-17 -0.1345932016-07-18 -0.1533332016-07-19 -0.2189282016-07-20 -0.1694262016-07-21 -0.2197472016-07-22 -0.1812662016-07-23 -0.1736742016-07-24 -0.1306292016-07-25 -0.1667302016-07-26 -0.2330442016-07-27 -0.2566422016-07-28 -0.2807382016-07-29 -0.2898932016-07-30 -0.379625 ... 2018-01-22 -0.2114672018-01-23 0.0349962018-01-24 -0.1059102018-01-25 -0.1457742018-01-26 -0.0893202018-01-27 -0.1643702018-01-28 -0.1108922018-01-29 -0.2057862018-01-30 -0.1011622018-01-31 -0.0347602018-02-01 0.2293332018-02-02 0.0437412018-02-03 0.0528372018-02-04 0.0577462018-02-05 -0.0714012018-02-06 -0.0111532018-02-07 -0.0457372018-02-08 -0.0219832018-02-09 -0.1967152018-02-10 -0.0637212018-02-11 -0.2894522018-02-12 -0.0509462018-02-13 -0.0470142018-02-14 0.0487542018-02-15 0.1439492018-02-16 0.4248232018-02-17 0.3618782018-02-18 0.3632352018-02-19 0.5174362018-02-20 0.368020Freq: D, Length: 600, dtype: float64import matplotlib.pyplot as plt%matplotlib inlineplt.figure(figsize=(15, 5))df.plot(style='r--')df.rolling(window=10).mean().plot(style='b')#<matplotlib.axes._subplots.AxesSubplot at 0x249627fb6d8> |

结果:

数据平稳性与差分法:

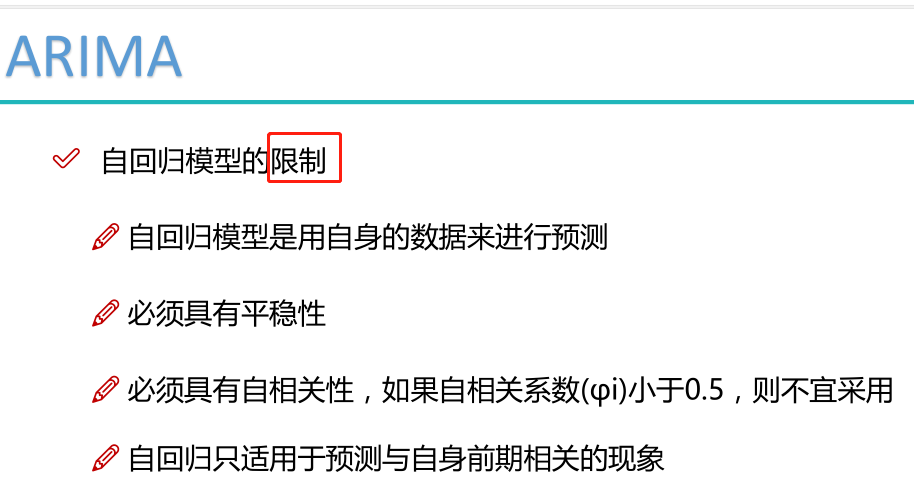

基本模型:自回归移动平均模型(ARMA(p,q))是时间序列中最为重要的模型之一。它主要由两部分组成: AR代表p阶自回归过程,MA代表q阶移动平均过程。

平稳性检验

我们知道序列平稳性是进行时间序列分析的前提条件,很多人都会有疑问,为什么要满足平稳性的要求呢?在大数定理和中心定理中要求样本同分布(这里同分布等价于时间序列中的平稳性),而我们的建模过程中有很多都是建立在大数定理和中心极限定理的前提条件下的,如果它不满足,得到的许多结论都是不可靠的。以虚假回归为例,当响应变量和输入变量都平稳时,我们用t统计量检验标准化系数的显著性。而当响应变量和输入变量不平稳时,其标准化系数不在满足t分布,这时再用t检验来进行显著性分析,导致拒绝原假设的概率增加,即容易犯第一类错误,从而得出错误的结论。

平稳时间序列有两种定义:严平稳和宽平稳

严平稳顾名思义,是一种条件非常苛刻的平稳性,它要求序列随着时间的推移,其统计性质保持不变。对于任意的τ,其联合概率密度函数满足:

严平稳的条件只是理论上的存在,现实中用得比较多的是宽平稳的条件。

宽平稳也叫弱平稳或者二阶平稳(均值和方差平稳),它应满足:

- 常数均值

- 常数方差

- 常数自协方差

ARIMA 模型对时间序列的要求是平稳型。因此,当你得到一个非平稳的时间序列时,首先要做的即是做时间序列的差分,直到得到一个平稳时间序列。如果你对时间序列做d次差分才能得到一个平稳序列,那么可以使用ARIMA(p,d,q)模型,其中d是差分次数。

二阶差分是指在一阶差分基础上再做一阶差分。

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 | %load_ext autoreload%autoreload 2%matplotlib inline%config InlineBackend.figure_format='retina'from __future__ import absolute_import, division, print_function# http://www.lfd.uci.edu/~gohlke/pythonlibs/#xgboost各种python库文件的下载,基本可以找到所有的import sysimport osimport pandas as pdimport numpy as np# # Remote Data Access# import pandas_datareader.data as web# import datetime# # reference: https://pandas-datareader.readthedocs.io/en/latest/remote_data.html# TSA from Statsmodelsimport statsmodels.api as smimport statsmodels.formula.api as smfimport statsmodels.tsa.api as smt# Display and Plottingimport matplotlib.pylab as pltimport seaborn as snspd.set_option('display.float_format', lambda x: '%.5f' % x) # pandasnp.set_printoptions(precision=5, suppress=True) # numpypd.set_option('display.max_columns', 100)pd.set_option('display.max_rows', 100)# seaborn plotting stylesns.set(style='ticks', context='poster')结果:The autoreload extension is already loaded. To reload it, use: %reload_ext autoreload |

1 2 3 4 | #Read the data#美国消费者信心指数Sentiment = 'data/sentiment.csv'Sentiment = pd.read_csv(Sentiment, index_col=0, parse_dates=[0]) |

1 | Sentiment.head() |

结果:

| UMCSENT | |

|---|---|

| DATE | |

| 2000-01-01 | 112.00000 |

| 2000-02-01 | 111.30000 |

| 2000-03-01 | 107.10000 |

| 2000-04-01 | 109.20000 |

| 2000-05-01 | 110.70000 |

1 2 | # Select the series from 2005 - 2016sentiment_short = Sentiment.loc['2005':'2016'] |

1 2 3 4 | sentiment_short.plot(figsize=(12,8))plt.legend(bbox_to_anchor=(1.25, 0.5))plt.title("Consumer Sentiment")sns.despine() |

结果:

1 2 3 4 5 | sentiment_short['diff_1'] = sentiment_short['UMCSENT'].diff(1)#求差分值,一阶差分。 1指的是1个时间间隔,可更改。sentiment_short['diff_2'] = sentiment_short['diff_1'].diff(1)#再求差分,二阶差分。sentiment_short.plot(subplots=True, figsize=(18, 12)) |

结果:

array([<matplotlib.axes._subplots.AxesSubplot object at 0x000001D9383BACF8>, <matplotlib.axes._subplots.AxesSubplot object at 0x000001D939FAB6A0>, <matplotlib.axes._subplots.AxesSubplot object at 0x000001D93A139B70>], dtype=object)

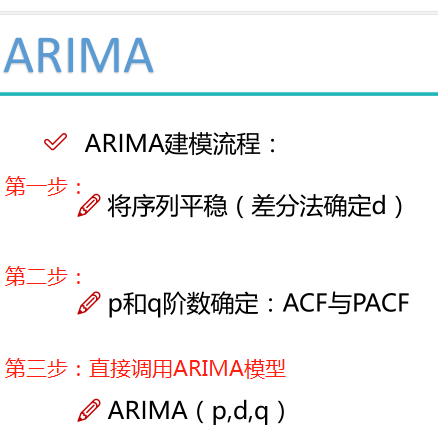

ARIMA模型:

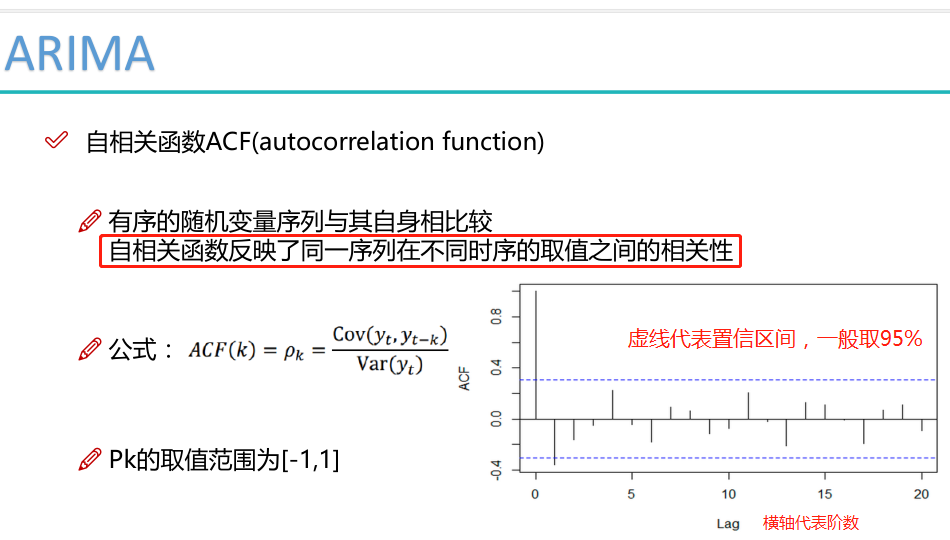

相关函数评估方法:

通过ACF和PACF的图选择出p值和q值。

建立ARIMA模型:

1 2 3 4 | del sentiment_short['diff_2']del sentiment_short['diff_1']sentiment_short.head()print (type(sentiment_short))#<class 'pandas.core.frame.DataFrame'> |

1 2 3 4 5 6 7 8 9 10 11 12 | fig = plt.figure(figsize=(12,8))#acfax1 = fig.add_subplot(211)fig = sm.graphics.tsa.plot_acf(sentiment_short, lags=20,ax=ax1)ax1.xaxis.set_ticks_position('bottom')fig.tight_layout();#pacfax2 = fig.add_subplot(212)fig = sm.graphics.tsa.plot_pacf(sentiment_short, lags=20, ax=ax2)ax2.xaxis.set_ticks_position('bottom')fig.tight_layout();#下图中的阴影表示置信区间,可以看出不同阶数自相关性的变化情况,从而选出p值和q值 |

结果:

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 | # 散点图也可以表示lags=9ncols=3nrows=int(np.ceil(lags/ncols))fig, axes = plt.subplots(ncols=ncols, nrows=nrows, figsize=(4*ncols, 4*nrows))for ax, lag in zip(axes.flat, np.arange(1,lags+1, 1)): lag_str = 't-{}'.format(lag) X = (pd.concat([sentiment_short, sentiment_short.shift(-lag)], axis=1, keys=['y'] + [lag_str]).dropna()) X.plot(ax=ax, kind='scatter', y='y', x=lag_str); corr = X.corr().as_matrix()[0][1] ax.set_ylabel('Original') ax.set_title('Lag: {} (corr={:.2f})'.format(lag_str, corr)); ax.set_aspect('equal'); sns.despine();fig.tight_layout(); |

结果:

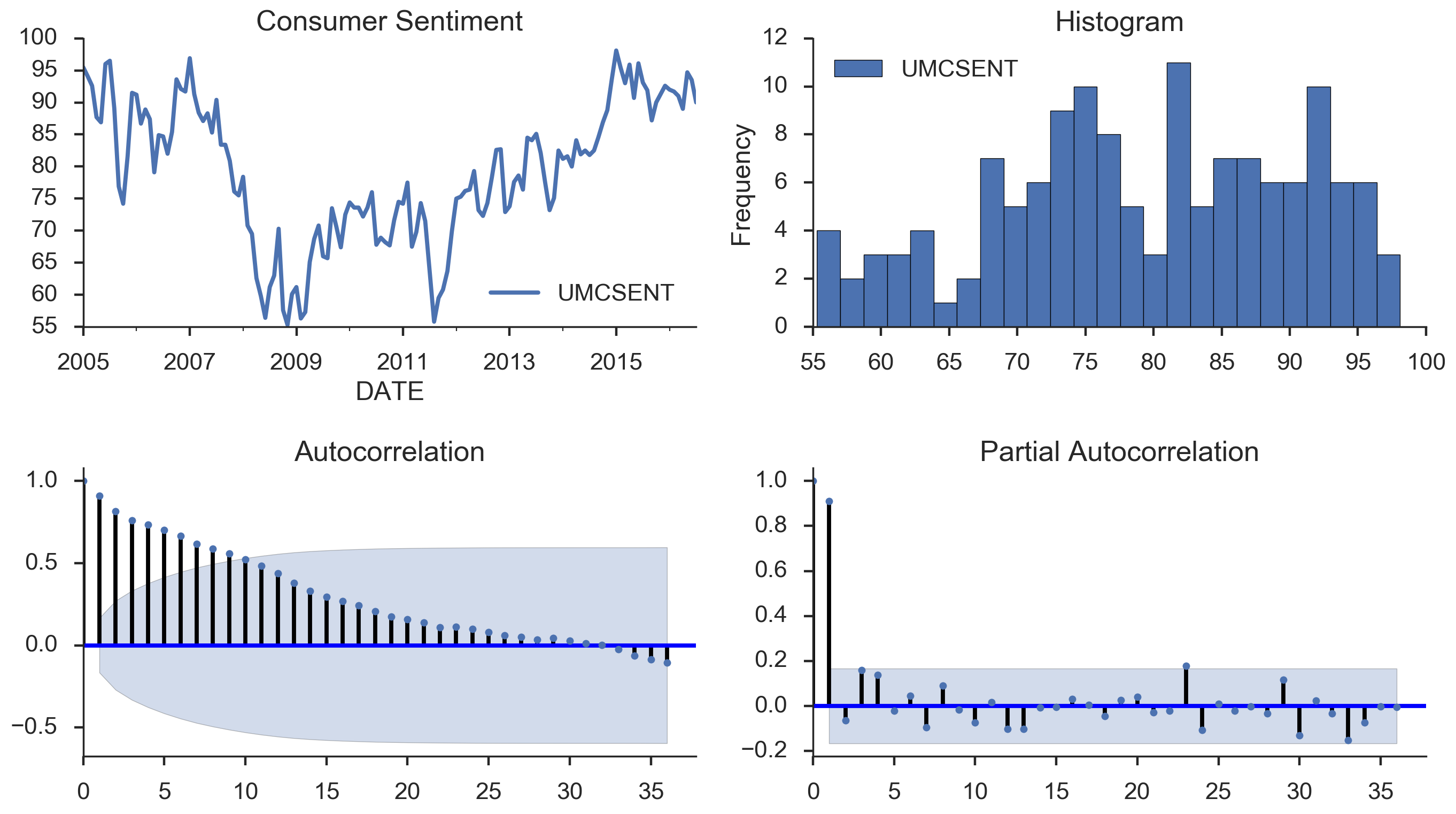

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 | # 更直观一些#模板,使用时直接改自己的数据就行,用以下四个图进行评估和分析就可以def tsplot(y, lags=None, title='', figsize=(14, 8)): fig = plt.figure(figsize=figsize) layout = (2, 2) ts_ax = plt.subplot2grid(layout, (0, 0)) hist_ax = plt.subplot2grid(layout, (0, 1)) acf_ax = plt.subplot2grid(layout, (1, 0)) pacf_ax = plt.subplot2grid(layout, (1, 1)) y.plot(ax=ts_ax) ts_ax.set_title(title) y.plot(ax=hist_ax, kind='hist', bins=25) hist_ax.set_title('Histogram') smt.graphics.plot_acf(y, lags=lags, ax=acf_ax) smt.graphics.plot_pacf(y, lags=lags, ax=pacf_ax) [ax.set_xlim(0) for ax in [acf_ax, pacf_ax]] sns.despine() plt.tight_layout() return ts_ax, acf_ax, pacf_axtsplot(sentiment_short, title='Consumer Sentiment', lags=36); |

结果:

参数选择:

BIC的结果受样本的影响,使用同一样本时,可以选择BIC。

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 | %load_ext autoreload%autoreload 2%matplotlib inline%config InlineBackend.figure_format='retina'from __future__ import absolute_import, division, print_functionimport sysimport osimport pandas as pdimport numpy as np# TSA from Statsmodelsimport statsmodels.api as smimport statsmodels.formula.api as smfimport statsmodels.tsa.api as smt# Display and Plottingimport matplotlib.pylab as pltimport seaborn as snspd.set_option('display.float_format', lambda x: '%.5f' % x) # pandasnp.set_printoptions(precision=5, suppress=True) # numpypd.set_option('display.max_columns', 100)pd.set_option('display.max_rows', 100)# seaborn plotting stylesns.set(style='ticks', context='poster') |

1 2 3 4 | filename_ts = 'data/series1.csv'ts_df = pd.read_csv(filename_ts, index_col=0, parse_dates=[0])n_sample = ts_df.shape[0] |

1 2 3 4 5 6 7 8 9 10 | print(ts_df.shape)print(ts_df.head())结果:(120, 1) value2006-06-01 0.215072006-07-01 1.142252006-08-01 0.080772006-09-01 -0.739522006-10-01 0.53552 |

1 2 3 4 5 6 7 8 9 10 11 | # Create a training sample and testing sample before analyzing the seriesn_train=int(0.95*n_sample)+1n_forecast=n_sample-n_train#ts_dfts_train = ts_df.iloc[:n_train]['value']ts_test = ts_df.iloc[n_train:]['value']print(ts_train.shape)print(ts_test.shape)print("Training Series:", "\n", ts_train.tail(), "\n")print("Testing Series:", "\n", ts_test.head()) |

结果:

(115,) (5,) Training Series: 2015-08-01 0.60371 2015-09-01 -1.27372 2015-10-01 -0.93284 2015-11-01 0.08552 2015-12-01 1.20534 Name: value, dtype: float64 Testing Series: 2016-01-01 2.16411 2016-02-01 0.95226 2016-03-01 0.36485 2016-04-01 -2.26487 2016-05-01 -2.38168 Name: value, dtype: float64

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 | def tsplot(y, lags=None, title='', figsize=(14, 8)): fig = plt.figure(figsize=figsize) layout = (2, 2) ts_ax = plt.subplot2grid(layout, (0, 0)) hist_ax = plt.subplot2grid(layout, (0, 1)) acf_ax = plt.subplot2grid(layout, (1, 0)) pacf_ax = plt.subplot2grid(layout, (1, 1)) y.plot(ax=ts_ax) ts_ax.set_title(title) y.plot(ax=hist_ax, kind='hist', bins=25) hist_ax.set_title('Histogram') smt.graphics.plot_acf(y, lags=lags, ax=acf_ax) smt.graphics.plot_pacf(y, lags=lags, ax=pacf_ax) [ax.set_xlim(0) for ax in [acf_ax, pacf_ax]] sns.despine() fig.tight_layout() return ts_ax, acf_ax, pacf_ax |

1 | tsplot(ts_train, title='A Given Training Series', lags=20); |

结果:

1 2 3 4 5 | #Model Estimation# Fit the modelarima200 = sm.tsa.SARIMAX(ts_train, order=(2,0,0))#order里边的三个参数p,d,qmodel_results = arima200.fit()#fit模型 |

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 | import itertools#当多组值都不符合时,遍历多组值,得出最好的值p_min = 0d_min = 0q_min = 0p_max = 4d_max = 0q_max = 4# Initialize a DataFrame to store the resultsresults_bic = pd.DataFrame(index=['AR{}'.format(i) for i in range(p_min,p_max+1)], columns=['MA{}'.format(i) for i in range(q_min,q_max+1)])for p,d,q in itertools.product(range(p_min,p_max+1), range(d_min,d_max+1), range(q_min,q_max+1)): if p==0 and d==0 and q==0: results_bic.loc['AR{}'.format(p), 'MA{}'.format(q)] = np.nan continue try: model = sm.tsa.SARIMAX(ts_train, order=(p, d, q), #enforce_stationarity=False, #enforce_invertibility=False, ) results = model.fit() results_bic.loc['AR{}'.format(p), 'MA{}'.format(q)] = results.bic except: continueresults_bic = results_bic[results_bic.columns].astype(float) |

1 2 3 4 5 6 7 8 | fig, ax = plt.subplots(figsize=(10, 8))ax = sns.heatmap(results_bic, mask=results_bic.isnull(), ax=ax, annot=True, fmt='.2f', );ax.set_title('BIC'); |

结果:

1 2 3 4 5 6 7 8 9 | # Alternative model selection method, limited to only searching AR and MA parameterstrain_results = sm.tsa.arma_order_select_ic(ts_train, ic=['aic', 'bic'], trend='nc', max_ar=4, max_ma=4)print('AIC', train_results.aic_min_order)print('BIC', train_results.bic_min_order)结果:得出两个不同的标准,比较尴尬,还需要进行筛选AIC (4, 2)BIC (1, 1) |

1 2 | #残差分析 正态分布 QQ图线性model_results.plot_diagnostics(figsize=(16, 12));#statsmodels库 |

结果:

Q-Q图:越像直线,则是正态分布;越不是直线,离正态分布越远。

时间序列建模基本步骤:

- 获取被观测系统时间序列数据;

- 对数据绘图,观测是否为平稳时间序列;对于非平稳时间序列要先进行d阶差分运算,化为平稳时间序列;

- 经过第二步处理,已经得到平稳时间序列。要对平稳时间序列分别求得其自相关系数ACF 和偏自相关系数PACF ,通过对自相关图和偏自相关图的分析,得到最佳的阶层 p 和阶数 q

- 由以上得到的 ,得到ARIMA模型。然后开始对得到的模型进行模型检验。

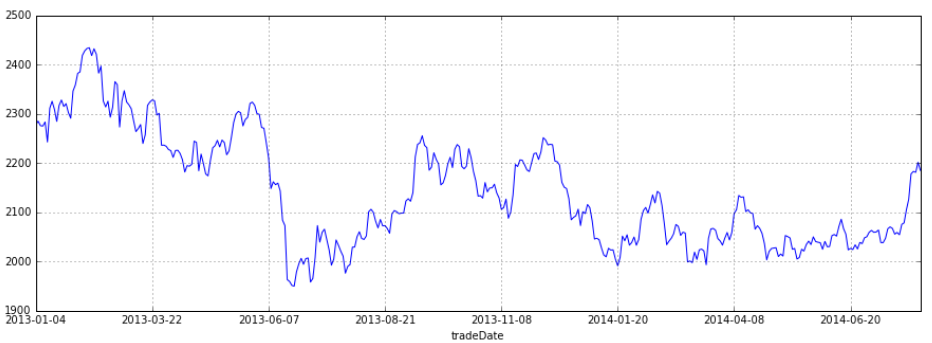

股票预测(属于回归):

1 2 3 4 5 6 7 8 9 10 11 12 13 | %matplotlib inlineimport pandas as pdimport pandas_datareader#用于从雅虎财经获取股票数据import datetimeimport matplotlib.pylab as pltimport seaborn as snsfrom matplotlib.pylab import stylefrom statsmodels.tsa.arima_model import ARIMAfrom statsmodels.graphics.tsaplots import plot_acf, plot_pacfstyle.use('ggplot') plt.rcParams['font.sans-serif'] = ['SimHei'] plt.rcParams['axes.unicode_minus'] = False |

1 2 3 | stockFile = 'data/T10yr.csv'stock = pd.read_csv(stockFile, index_col=0, parse_dates=[0])#将索引index设置为时间,parse_dates对日期格式处理为标准格式。stock.head(10) |

结果:

| Open | High | Low | Close | Volume | Adj Close | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 2000-01-03 | 6.498 | 6.603 | 6.498 | 6.548 | 0 | 6.548 |

| 2000-01-04 | 6.530 | 6.548 | 6.485 | 6.485 | 0 | 6.485 |

| 2000-01-05 | 6.521 | 6.599 | 6.508 | 6.599 | 0 | 6.599 |

| 2000-01-06 | 6.558 | 6.585 | 6.540 | 6.549 | 0 | 6.549 |

| 2000-01-07 | 6.545 | 6.595 | 6.504 | 6.504 | 0 | 6.504 |

| 2000-01-10 | 6.540 | 6.567 | 6.536 | 6.558 | 0 | 6.558 |

| 2000-01-11 | 6.600 | 6.664 | 6.595 | 6.664 | 0 | 6.664 |

| 2000-01-12 | 6.659 | 6.696 | 6.645 | 6.696 | 0 | 6.696 |

| 2000-01-13 | 6.664 | 6.705 | 6.618 | 6.618 | 0 | 6.618 |

| 2000-01-14 | 6.623 | 6.688 | 6.563 | 6.674 | 0 | 6.674 |

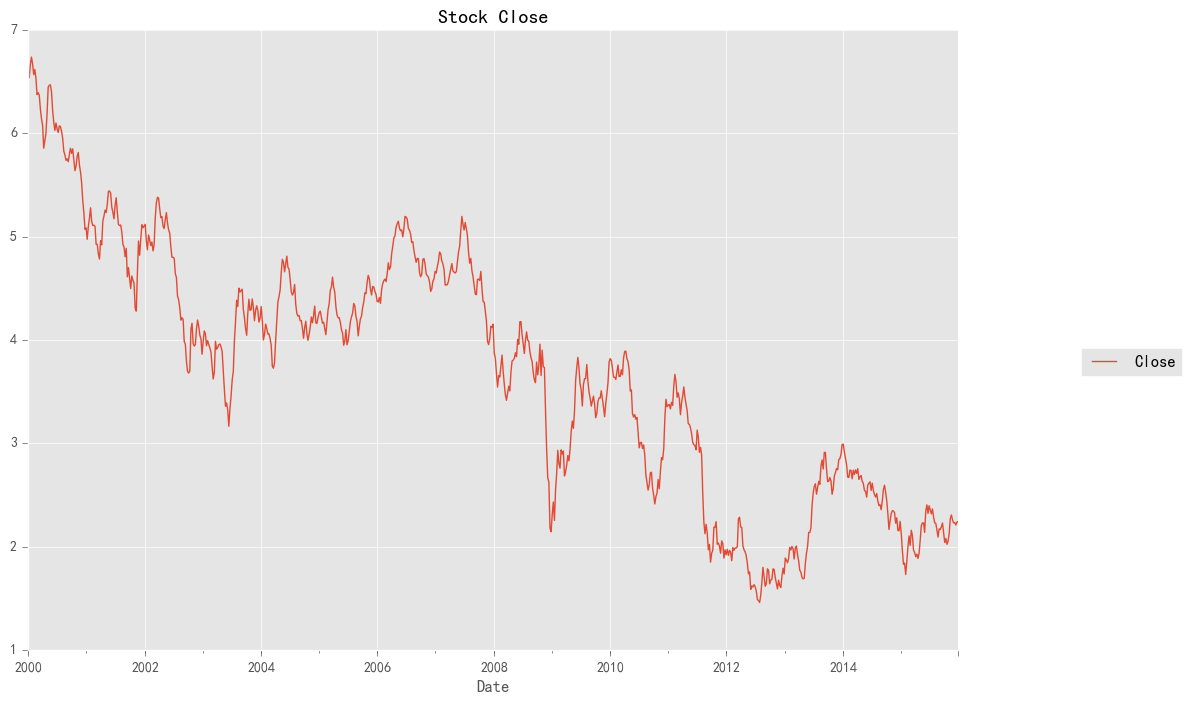

1 2 | stock_week = stock['Close'].resample('W-MON').mean()stock_train = stock_week['2000':'2015'] |

1 2 3 4 | stock_train.plot(figsize=(12,8))plt.legend(bbox_to_anchor=(1.25, 0.5))plt.title("Stock Close")sns.despine() |

结果:

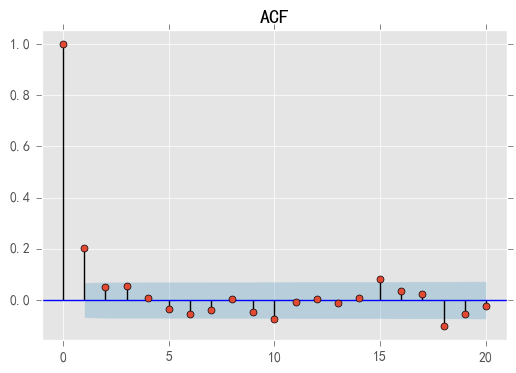

1 2 3 4 5 6 7 | stock_diff = stock_train.diff()stock_diff = stock_diff.dropna()plt.figure()plt.plot(stock_diff)plt.title('一阶差分')plt.show() |

结果:

1 2 3 | acf = plot_acf(stock_diff, lags=20)plt.title("ACF")acf.show() |

结果:

1 2 3 | pacf = plot_pacf(stock_diff, lags=20)plt.title("PACF")pacf.show() |

结果:

1 | model = ARIMA(stock_train, order=(1, 1, 1),freq='W-MON') |

1 2 | result = model.fit()#print(result.summary())#统计出ARIMA模型的指标 |

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 | pred = result.predict('20140609', '20160701',dynamic=True, typ='levels')#预测,指定起始与终止时间。预测值起始时间必须在原始数据中,终止时间不需要print (pred)结果:2014-06-09 2.4635592014-06-16 2.4555392014-06-23 2.4495692014-06-30 2.4441832014-07-07 2.4389622014-07-14 2.4337882014-07-21 2.4286272014-07-28 2.4234702014-08-04 2.4183152014-08-11 2.4131592014-08-18 2.4080042014-08-25 2.4028492014-09-01 2.3976932014-09-08 2.3925382014-09-15 2.3873832014-09-22 2.3822272014-09-29 2.3770722014-10-06 2.3719172014-10-13 2.3667612014-10-20 2.3616062014-10-27 2.3564512014-11-03 2.3512962014-11-10 2.3461402014-11-17 2.3409852014-11-24 2.3358302014-12-01 2.3306742014-12-08 2.3255192014-12-15 2.3203642014-12-22 2.3152082014-12-29 2.310053 ... 2015-12-07 2.0574432015-12-14 2.0522882015-12-21 2.0471322015-12-28 2.0419772016-01-04 2.0368222016-01-11 2.0316662016-01-18 2.0265112016-01-25 2.0213562016-02-01 2.0162002016-02-08 2.0110452016-02-15 2.0058902016-02-22 2.0007352016-02-29 1.9955792016-03-07 1.9904242016-03-14 1.9852692016-03-21 1.9801132016-03-28 1.9749582016-04-04 1.9698032016-04-11 1.9646472016-04-18 1.9594922016-04-25 1.9543372016-05-02 1.9491812016-05-09 1.9440262016-05-16 1.9388712016-05-23 1.9337162016-05-30 1.9285602016-06-06 1.9234052016-06-13 1.9182502016-06-20 1.9130942016-06-27 1.907939Freq: W-MON, Length: 108, dtype: float64 |

1 2 3 4 | plt.figure(figsize=(6, 6))plt.xticks(rotation=45)plt.plot(pred)plt.plot(stock_train)#[<matplotlib.lines.Line2D at 0x28025665278>] |

结果:

使用tfresh库进行分类任务:

tsfresh是开源的提取时序数据特征的python包,能够提取出超过64种特征,堪称提取时序特征的瑞士军刀。用到时tfresh查官方文档

1 2 3 4 5 6 7 8 9 10 11 12 13 | %matplotlib inlineimport matplotlib.pylab as pltimport seaborn as snsfrom tsfresh.examples.robot_execution_failures import download_robot_execution_failures, load_robot_execution_failuresfrom tsfresh import extract_features, extract_relevant_features, select_featuresfrom tsfresh.utilities.dataframe_functions import imputefrom tsfresh.feature_extraction import ComprehensiveFCParametersfrom sklearn.tree import DecisionTreeClassifierfrom sklearn.cross_validation import train_test_splitfrom sklearn.metrics import classification_report#http://tsfresh.readthedocs.io/en/latest/text/quick_start.html#官方文档 |

1 2 3 | download_robot_execution_failures()df, y = load_robot_execution_failures()df.head() |

结果:

id time a b c d e f 0 1 0 -1 -1 63 -3 -1 0 1 1 1 0 0 62 -3 -1 0 2 1 2 -1 -1 61 -3 0 0 3 1 3 -1 -1 63 -2 -1 0 4 1 4 -1 -1 63 -3 -1 0

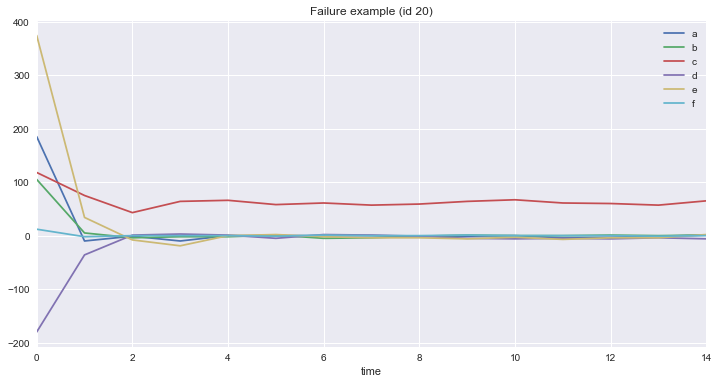

1 2 | df[df.id == 3][['time', 'a', 'b', 'c', 'd', 'e', 'f']].plot(x='time', title='Success example (id 3)', figsize=(12, 6));df[df.id == 20][['time', 'a', 'b', 'c', 'd', 'e', 'f']].plot(x='time', title='Failure example (id 20)', figsize=(12, 6)); |

结果:

1 | extraction_settings = ComprehensiveFCParameters()#提取特征 |

1 2 3 4 5 6 | #column_id (str) – The name of the id column to group by#column_sort (str) – The name of the sort column.X = extract_features(df, column_id='id', column_sort='time',#以id为聚合,以time排序 default_fc_parameters=extraction_settings, impute_function= impute) |

1 | X.head()#提取到的特征 |

结果:

a__mean_abs_change_quantiles__qh_1.0__ql_0.8 a__percentage_of_reoccurring_values_to_all_values a__mean_abs_change_quantiles__qh_1.0__ql_0.2 a__mean_abs_change_quantiles__qh_1.0__ql_0.0 a__large_standard_deviation__r_0.45 a__absolute_sum_of_changes a__mean_abs_change_quantiles__qh_1.0__ql_0.4 a__mean_second_derivate_central a__autocorrelation__lag_4 a__binned_entropy__max_bins_10 ... f__fft_coefficient__coeff_0 f__fft_coefficient__coeff_1 f__fft_coefficient__coeff_2 f__fft_coefficient__coeff_3 f__fft_coefficient__coeff_4 f__fft_coefficient__coeff_5 f__fft_coefficient__coeff_6 f__fft_coefficient__coeff_7 f__fft_coefficient__coeff_8 f__fft_coefficient__coeff_9 id 1 0.142857 0.933333 0.142857 0.142857 0.0 2.0 0.142857 -0.038462 0.17553 0.244930 ... 0.0 0.000000 0.000000 0.000000 0.000000 0.0 0.000000 0.000000 0.0 0.0 2 0.000000 1.000000 0.400000 1.000000 0.0 14.0 0.400000 -0.038462 0.17553 0.990835 ... -4.0 0.744415 1.273659 -0.809017 1.373619 0.5 0.309017 -1.391693 0.0 0.0 3 0.000000 0.933333 0.714286 0.714286 0.0 10.0 0.714286 -0.038462 0.17553 0.729871 ... -4.0 -0.424716 0.878188 1.000000 1.851767 0.5 1.000000 -2.805239 0.0 0.0 4 0.000000 1.000000 0.800000 1.214286 0.0 17.0 0.800000 -0.038462 0.17553 1.322950 ... -5.0 -1.078108 3.678858 -3.618034 -1.466977 -0.5 -1.381966 -0.633773 0.0 0.0 5 2.000000 0.866667 0.916667 0.928571 0.0 13.0 0.916667 0.038462 0.17553 1.020037 ... -2.0 -3.743460 3.049653 -0.618034 1.198375 -0.5 1.618034 -0.004568 0.0 0.0 5 rows × 1332 columns

1 2 3 4 5 6 7 | X.info()#结果:<class 'pandas.core.frame.DataFrame'>Int64Index: 88 entries, 1 to 88Columns: 1332 entries, a__mean_abs_change_quantiles__qh_1.0__ql_0.8 to f__fft_coefficient__coeff_9dtypes: float64(1332)memory usage: 916.4 KB |

1 2 3 | X_filtered = extract_relevant_features(df, y, column_id='id', column_sort='time', default_fc_parameters=extraction_settings)#特征过滤,选择最相关的特征。具体了解查看官方文档 |

1 | X_filtered.head()#新特征 |

结果:

a__abs_energy a__range_count__max_1__min_-1 b__abs_energy e__variance e__standard_deviation e__abs_energy c__standard_deviation c__variance a__standard_deviation a__variance ... b__has_duplicate_max b__cwt_coefficients__widths_(2, 5, 10, 20)__coeff_14__w_5 b__cwt_coefficients__widths_(2, 5, 10, 20)__coeff_13__w_2 e__quantile__q_0.1 a__ar_coefficient__k_10__coeff_1 a__quantile__q_0.2 b__quantile__q_0.7 f__large_standard_deviation__r_0.35 f__quantile__q_0.9 d__spkt_welch_density__coeff_5 id 1 14.0 15.0 13.0 0.222222 0.471405 10.0 1.203698 1.448889 0.249444 0.062222 ... 1.0 -0.751682 -0.310265 -1.0 0.125000 -1.0 -1.0 0.0 0.0 0.037795 2 25.0 13.0 76.0 4.222222 2.054805 90.0 4.333846 18.782222 0.956847 0.915556 ... 1.0 0.057818 -0.202951 -3.6 -0.078829 -1.0 -1.0 1.0 0.0 0.319311 3 12.0 14.0 40.0 3.128889 1.768867 103.0 4.616877 21.315556 0.596285 0.355556 ... 0.0 0.912474 0.539121 -4.0 0.084836 -1.0 0.0 1.0 0.0 9.102780 4 16.0 10.0 60.0 7.128889 2.669998 124.0 3.833188 14.693333 0.952190 0.906667 ... 0.0 -0.609735 -2.641390 -4.6 0.003108 -1.0 1.0 0.0 0.0 56.910262 5 17.0 13.0 46.0 4.160000 2.039608 180.0 4.841487 23.440000 0.879394 0.773333 ... 0.0 0.072771 0.591927 -5.0 0.087906 -1.0 0.8 0.0 0.6 22.841805 5 rows × 300 columns

1 | X_filtered.info() |

结果:

<class 'pandas.core.frame.DataFrame'> Int64Index: 88 entries, 1 to 88 Columns: 300 entries, a__abs_energy to d__spkt_welch_density__coeff_5 dtypes: float64(300) memory usage: 206.9 KB

1 | X_train, X_test, X_filtered_train, X_filtered_test, y_train, y_test = train_test_split(X, X_filtered, y, test_size=.4) |

1 2 3 | cl = DecisionTreeClassifier()cl.fit(X_train, y_train)print(classification_report(y_test, cl.predict(X_test)))#对模型进行评估,可以看出这个结果还不错 |

结果:

precision recall f1-score support

0 1.00 0.89 0.94 9

1 0.96 1.00 0.98 27

avg / total 0.97 0.97 0.97 36

1 | cl.n_features_#1332 |

1 2 3 | cl2 = DecisionTreeClassifier()cl2.fit(X_filtered_train, y_train)print(classification_report(y_test, cl2.predict(X_filtered_test))) |

结果:

cl2 = DecisionTreeClassifier() cl2.fit(X_filtered_train, y_train) print(classification_report(y_test, cl2.predict(X_filtered_test))) cl2 = DecisionTreeClassifier() cl2.fit(X_filtered_train, y_train) print(classification_report(y_test, cl2.predict(X_filtered_test))) precision recall f1-score support 0 1.00 0.78 0.88 9 1 0.93 1.00 0.96 27 avg / total 0.95 0.94 0.94 36

1 | cl2.n_features_#300 |

维基百科词条EDA

探索性数据分析(EDA)目的是最大化对数据的直觉,完成这个事情的方法只能是结合统计学的图形以各种形式展现出来。通过EDA可以实现:

1. 得到数据的直观表现

2. 发现潜在的结构

3. 提取重要的变量

4. 处理异常值

5. 检验统计假设

6. 建立初步模型

7. 决定最优因子的设置

1 2 3 4 5 | import pandas as pdimport numpy as npimport matplotlib.pyplot as pltimport re%matplotlib inline |

1 2 | train = pd.read_csv('train_1.csv').fillna(0)train.head() |

结果:

Page 2015-07-01 2015-07-02 2015-07-03 2015-07-04 2015-07-05 2015-07-06 2015-07-07 2015-07-08 2015-07-09 ... 2016-12-22 2016-12-23 2016-12-24 2016-12-25 2016-12-26 2016-12-27 2016-12-28 2016-12-29 2016-12-30 2016-12-31

0 2NE1_zh.wikipedia.org_all-access_spider 18.0 11.0 5.0 13.0 14.0 9.0 9.0 22.0 26.0 ... 32.0 63.0 15.0 26.0 14.0 20.0 22.0 19.0 18.0 20.0

1 2PM_zh.wikipedia.org_all-access_spider 11.0 14.0 15.0 18.0 11.0 13.0 22.0 11.0 10.0 ... 17.0 42.0 28.0 15.0 9.0 30.0 52.0 45.0 26.0 20.0

2 3C_zh.wikipedia.org_all-access_spider 1.0 0.0 1.0 1.0 0.0 4.0 0.0 3.0 4.0 ... 3.0 1.0 1.0 7.0 4.0 4.0 6.0 3.0 4.0 17.0

3 4minute_zh.wikipedia.org_all-access_spider 35.0 13.0 10.0 94.0 4.0 26.0 14.0 9.0 11.0 ... 32.0 10.0 26.0 27.0 16.0 11.0 17.0 19.0 10.0 11.0

4 52_Hz_I_Love_You_zh.wikipedia.org_all-access_s... 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 ... 48.0 9.0 25.0 13.0 3.0 11.0 27.0 13.0 36.0 10.0

5 rows × 551 columns

1 2 3 4 5 6 | train.info()结果:<class 'pandas.core.frame.DataFrame'>RangeIndex: 145063 entries, 0 to 145062Columns: 551 entries, Page to 2016-12-31dtypes: float64(550), object(1)memory usage: 609.8+ MB |

1 2 3 | for col in train.columns[1:]: train[col] = pd.to_numeric(train[col],downcast='integer')#float数据较为占内存,从上表可以看出,小数点后都是0,可将数据转换为int,减小内存。train.head() |

结果:

Page 2015-07-01 2015-07-02 2015-07-03 2015-07-04 2015-07-05 2015-07-06 2015-07-07 2015-07-08 2015-07-09 ... 2016-12-22 2016-12-23 2016-12-24 2016-12-25 2016-12-26 2016-12-27 2016-12-28 2016-12-29 2016-12-30 2016-12-31

0 2NE1_zh.wikipedia.org_all-access_spider 18 11 5 13 14 9 9 22 26 ... 32 63 15 26 14 20 22 19 18 20

1 2PM_zh.wikipedia.org_all-access_spider 11 14 15 18 11 13 22 11 10 ... 17 42 28 15 9 30 52 45 26 20

2 3C_zh.wikipedia.org_all-access_spider 1 0 1 1 0 4 0 3 4 ... 3 1 1 7 4 4 6 3 4 17

3 4minute_zh.wikipedia.org_all-access_spider 35 13 10 94 4 26 14 9 11 ... 32 10 26 27 16 11 17 19 10 11

4 52_Hz_I_Love_You_zh.wikipedia.org_all-access_s... 0 0 0 0 0 0 0 0 0 ... 48 9 25 13 3 11 27 13 36 10

5 rows × 551 columns

1 2 3 4 5 6 7 | train.info()结果:<class 'pandas.core.frame.DataFrame'>RangeIndex: 145063 entries, 0 to 145062Columns: 551 entries, Page to 2016-12-31dtypes: int32(550), object(1)memory usage: 305.5+ MB |

1 2 3 4 5 6 7 8 9 10 11 12 | def get_language(page):#将词条按国家分类 res = re.search('[a-z][a-z].wikipedia.org',page) #print (res.group()[0:2]) if res: return res.group()[0:2] return 'na'train['lang'] = train.Page.map(get_language)from collections import Counterprint(Counter(train.lang)) |

结果:Counter({'en': 24108, 'ja': 20431, 'de': 18547, 'na': 17855, 'fr': 17802, 'zh': 17229, 'ru': 15022, 'es': 14069})

1 2 3 4 5 6 7 8 9 10 11 12 13 | lang_sets = {}lang_sets['en'] = train[train.lang=='en'].iloc[:,0:-1]lang_sets['ja'] = train[train.lang=='ja'].iloc[:,0:-1]lang_sets['de'] = train[train.lang=='de'].iloc[:,0:-1]lang_sets['na'] = train[train.lang=='na'].iloc[:,0:-1]lang_sets['fr'] = train[train.lang=='fr'].iloc[:,0:-1]lang_sets['zh'] = train[train.lang=='zh'].iloc[:,0:-1]lang_sets['ru'] = train[train.lang=='ru'].iloc[:,0:-1]lang_sets['es'] = train[train.lang=='es'].iloc[:,0:-1]sums = {}for key in lang_sets: sums[key] = lang_sets[key].iloc[:,1:].sum(axis=0) / lang_sets[key].shape[0] |

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 | days = [r for r in range(sums['en'].shape[0])]fig = plt.figure(1,figsize=[10,10])plt.ylabel('Views per Page')plt.xlabel('Day')plt.title('Pages in Different Languages')labels={'en':'English','ja':'Japanese','de':'German', 'na':'Media','fr':'French','zh':'Chinese', 'ru':'Russian','es':'Spanish' }for key in sums: plt.plot(days,sums[key],label = labels[key] ) plt.legend()plt.show() |

结果:

1 2 3 4 5 6 7 8 9 | def plot_entry(key,idx): data = lang_sets[key].iloc[idx,1:] fig = plt.figure(1,figsize=(10,5)) plt.plot(days,data) plt.xlabel('day') plt.ylabel('views') plt.title(train.iloc[lang_sets[key].index[idx],0]) plt.show() |

1 2 3 | idx = [1, 5, 10, 50, 100, 250,500, 750,1000,1500,2000,3000,4000,5000]for i in idx:#按词条分类 plot_entry('en',i) |

结果:

1 2 3 4 5 6 7 8 9 | npages = 5top_pages = {}for key in lang_sets: print(key) sum_set = pd.DataFrame(lang_sets[key][['Page']]) sum_set['total'] = lang_sets[key].sum(axis=1) sum_set = sum_set.sort_values('total',ascending=False) print(sum_set.head(10)) top_pages[key] = sum |

结果:

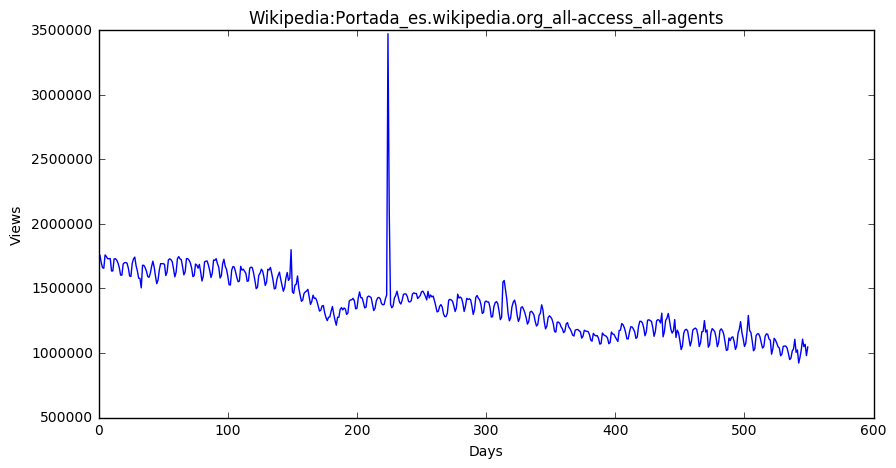

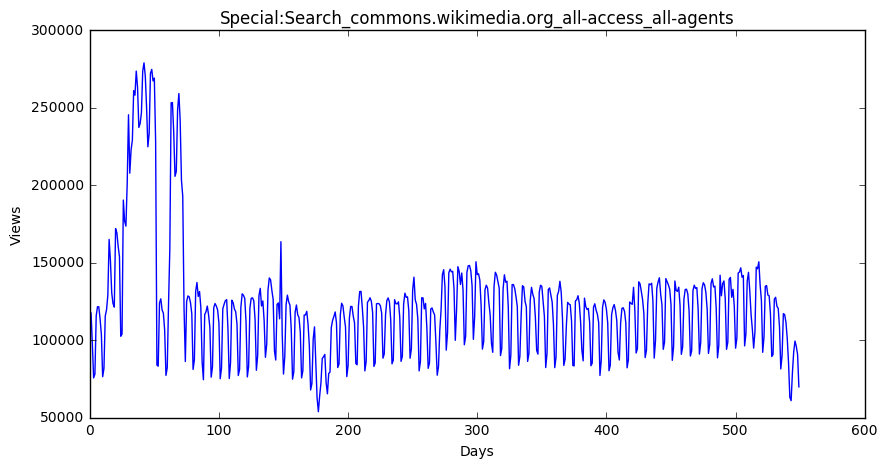

zh Page total 28727 Wikipedia:首页_zh.wikipedia.org_all-access_all-a... 123694312 61350 Wikipedia:首页_zh.wikipedia.org_desktop_all-agents 66435641 105844 Wikipedia:首页_zh.wikipedia.org_mobile-web_all-a... 50887429 28728 Special:搜索_zh.wikipedia.org_all-access_all-agents 48678124 61351 Special:搜索_zh.wikipedia.org_desktop_all-agents 48203843 28089 Running_Man_zh.wikipedia.org_all-access_all-ag... 11485845 30960 Special:链接搜索_zh.wikipedia.org_all-access_all-a... 10320403 63510 Special:链接搜索_zh.wikipedia.org_desktop_all-agents 10320336 60711 Running_Man_zh.wikipedia.org_desktop_all-agents 7968443 30446 瑯琊榜_(電視劇)_zh.wikipedia.org_all-access_all-agents 5891589 fr Page total 27330 Wikipédia:Accueil_principal_fr.wikipedia.org_a... 868480667 55104 Wikipédia:Accueil_principal_fr.wikipedia.org_m... 611302821 7344 Wikipédia:Accueil_principal_fr.wikipedia.org_d... 239589012 27825 Spécial:Recherche_fr.wikipedia.org_all-access_... 95666374 8221 Spécial:Recherche_fr.wikipedia.org_desktop_all... 88448938 26500 Sp?cial:Search_fr.wikipedia.org_all-access_all... 76194568 6978 Sp?cial:Search_fr.wikipedia.org_desktop_all-ag... 76185450 131296 Wikipédia:Accueil_principal_fr.wikipedia.org_a... 63860799 26993 Organisme_de_placement_collectif_en_valeurs_mo... 36647929 7213 Organisme_de_placement_collectif_en_valeurs_mo... 36624145 ru Page total 99322 Заглавная_страница_ru.wikipedia.org_all-access... 1086019452 103123 Заглавная_страница_ru.wikipedia.org_desktop_al... 742880016 17670 Заглавная_страница_ru.wikipedia.org_mobile-web... 327930433 99537 Служебная:Поиск_ru.wikipedia.org_all-access_al... 103764279 103349 Служебная:Поиск_ru.wikipedia.org_desktop_all-a... 98664171 100414 Служебная:Ссылки_сюда_ru.wikipedia.org_all-acc... 25102004 104195 Служебная:Ссылки_сюда_ru.wikipedia.org_desktop... 25058155 97670 Special:Search_ru.wikipedia.org_all-access_all... 24374572 101457 Special:Search_ru.wikipedia.org_desktop_all-ag... 21958472 98301 Служебная:Вход_ru.wikipedia.org_all-access_all... 12162587 ja Page total 120336 メインページ_ja.wikipedia.org_all-access_all-agents 210753795 86431 メインページ_ja.wikipedia.org_desktop_all-agents 134147415 123025 特別:検索_ja.wikipedia.org_all-access_all-agents 70316929 89202 特別:検索_ja.wikipedia.org_desktop_all-agents 69215206 57309 メインページ_ja.wikipedia.org_mobile-web_all-agents 66459122 119609 特別:最近の更新_ja.wikipedia.org_all-access_all-agents 17662791 88897 特別:最近の更新_ja.wikipedia.org_desktop_all-agents 17627621 119625 真田信繁_ja.wikipedia.org_all-access_all-agents 10793039 123292 特別:外部リンク検索_ja.wikipedia.org_all-access_all-agents 10331191 89463 特別:外部リンク検索_ja.wikipedia.org_desktop_all-agents 10327917 es Page total 92205 Wikipedia:Portada_es.wikipedia.org_all-access_... 751492304 95855 Wikipedia:Portada_es.wikipedia.org_mobile-web_... 565077372 90810 Especial:Buscar_es.wikipedia.org_all-access_al... 194491245 71199 Wikipedia:Portada_es.wikipedia.org_desktop_all... 165439354 69939 Especial:Buscar_es.wikipedia.org_desktop_all-a... 160431271 94389 Especial:Buscar_es.wikipedia.org_mobile-web_al... 34059966 90813 Especial:Entrar_es.wikipedia.org_all-access_al... 33983359 143440 Wikipedia:Portada_es.wikipedia.org_all-access_... 31615409 93094 Lali_Espósito_es.wikipedia.org_all-access_all-... 26602688 69942 Especial:Entrar_es.wikipedia.org_desktop_all-a... 25747141 en Page total 38573 Main_Page_en.wikipedia.org_all-access_all-agents 12066181102 9774 Main_Page_en.wikipedia.org_desktop_all-agents 8774497458 74114 Main_Page_en.wikipedia.org_mobile-web_all-agents 3153984882 39180 Special:Search_en.wikipedia.org_all-access_all... 1304079353 10403 Special:Search_en.wikipedia.org_desktop_all-ag... 1011847748 74690 Special:Search_en.wikipedia.org_mobile-web_all... 292162839 39172 Special:Book_en.wikipedia.org_all-access_all-a... 133993144 10399 Special:Book_en.wikipedia.org_desktop_all-agents 133285908 33644 Main_Page_en.wikipedia.org_all-access_spider 129020407 34257 Special:Search_en.wikipedia.org_all-access_spider 124310206 na Page total 45071 Special:Search_commons.wikimedia.org_all-acces... 67150638 81665 Special:Search_commons.wikimedia.org_desktop_a... 63349756 45056 Special:CreateAccount_commons.wikimedia.org_al... 53795386 45028 Main_Page_commons.wikimedia.org_all-access_all... 52732292 81644 Special:CreateAccount_commons.wikimedia.org_de... 48061029 81610 Main_Page_commons.wikimedia.org_desktop_all-ag... 39160923 46078 Special:RecentChangesLinked_commons.wikimedia.... 28306336 45078 Special:UploadWizard_commons.wikimedia.org_all... 23733805 81671 Special:UploadWizard_commons.wikimedia.org_des... 22008544 82680 Special:RecentChangesLinked_commons.wikimedia.... 21915202 de Page total 139119 Wikipedia:Hauptseite_de.wikipedia.org_all-acce... 1603934248 116196 Wikipedia:Hauptseite_de.wikipedia.org_mobile-w... 1112689084 67049 Wikipedia:Hauptseite_de.wikipedia.org_desktop_... 426992426 140151 Spezial:Suche_de.wikipedia.org_all-access_all-... 223425944 66736 Spezial:Suche_de.wikipedia.org_desktop_all-agents 219636761 140147 Spezial:Anmelden_de.wikipedia.org_all-access_a... 40291806 138800 Special:Search_de.wikipedia.org_all-access_all... 39881543 68104 Spezial:Anmelden_de.wikipedia.org_desktop_all-... 35355226 68511 Special:MyPage/toolserverhelferleinconfig.js_d... 32584955 137765 Hauptseite_de.wikipedia.org_all-access_all-agents 31732458

1 2 3 4 5 6 7 8 9 10 | for key in top_pages: fig = plt.figure(1,figsize=(10,5)) cols = train.columns cols = cols[1:-1] data = train.loc[top_pages[key],cols] plt.plot(days,data) plt.xlabel('Days') plt.ylabel('Views') plt.title(train.loc[top_pages[key],'Page']) plt.show() |

结果:

【推荐】国内首个AI IDE,深度理解中文开发场景,立即下载体验Trae

【推荐】编程新体验,更懂你的AI,立即体验豆包MarsCode编程助手

【推荐】抖音旗下AI助手豆包,你的智能百科全书,全免费不限次数

【推荐】轻量又高性能的 SSH 工具 IShell:AI 加持,快人一步

· 10年+ .NET Coder 心语,封装的思维:从隐藏、稳定开始理解其本质意义

· .NET Core 中如何实现缓存的预热?

· 从 HTTP 原因短语缺失研究 HTTP/2 和 HTTP/3 的设计差异

· AI与.NET技术实操系列:向量存储与相似性搜索在 .NET 中的实现

· 基于Microsoft.Extensions.AI核心库实现RAG应用

· 10年+ .NET Coder 心语 ── 封装的思维:从隐藏、稳定开始理解其本质意义

· 地球OL攻略 —— 某应届生求职总结

· 提示词工程——AI应用必不可少的技术

· Open-Sora 2.0 重磅开源!

· 周边上新:园子的第一款马克杯温暖上架