拓端tecdat|R语言编程指导中的马尔科夫机制转换(Markov regime switching)模型

原文链接:http://tecdat.cn/?p=12187

金融分析师通常关心检测市场何时“发生变化”:几个月或至几年内市场的典型行为可以立即转变为非常不同的行为。投资者希望及时发现这些变化,以便可以相应地调整其策略,但是这样做可能很困难。

RHmm从CRAN不再可用,因此我想使用其他软件包复制功能实现马尔科夫机制转换(Markov regime switching)模型从而对典型的市场行为进行预测,并且增加模型中对参数的线性约束功能。

library(SIT)

load.packages('quantmod')

# find regimes

load.packages('RHmm', repos ='http://R-Forge.R-project.org')

y=returns

ResFit = HMMFit(y, nStates=2)

VitPath = viterbi(ResFit, y)DimObs = 1

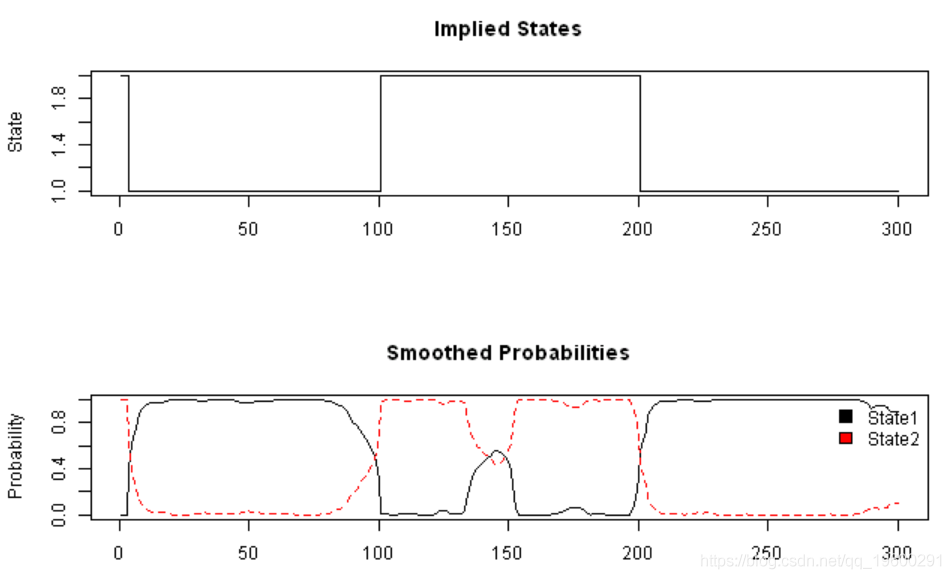

matplot(fb$Gamma, type='l', main='Smoothed Probabilities', ylab='Probability')

legend(x='topright', c('State1','State2'), fill=1:2, bty='n')

![]()

fm2 = fit(mod, verbose = FALSE)使用logLik在迭代69处收敛:125.6168

probs = posterior(fm2)

layout(1:2)

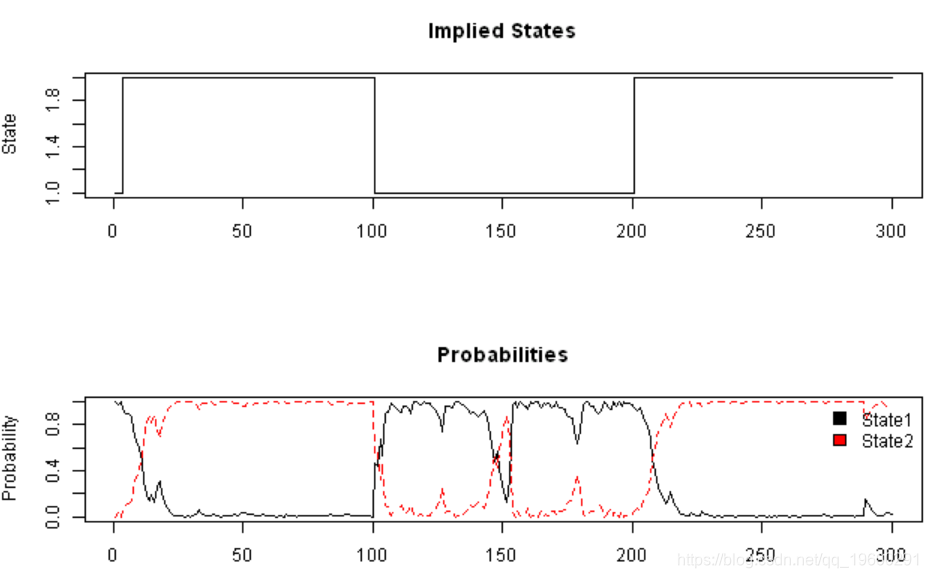

plot(probs$state, type='s', main='Implied States', xlab='', ylab='State')

matplot(probs[,-1], type='l', main='Probabilities', ylab='Probability')

legend(x='topright', c('State1','State2'), fill=1:2, bty='n')

![]()

#*****************************************************************

# Add some data and see if the model is able to identify the regimes

#******************************************************************

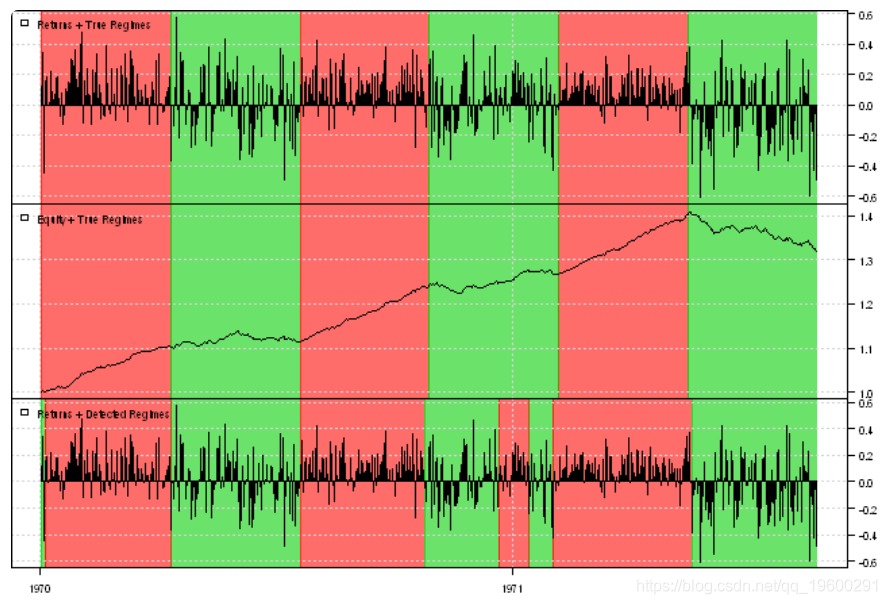

bear2 = rnorm( 100, -0.01, 0.20 )

bull3 = rnorm( 100, 0.10, 0.10 )

bear3 = rnorm( 100, -0.01, 0.25 )

true.states = c(true.states, rep(2,100),rep(1,100),rep(2,100))

y = c( bull1, bear, bull2, bear2, bull3, bear3 )

DimObs = 1

plota(data, type='h', x.highlight=T)

plota.legend('Returns + Detected Regimes')

![]()

#*****************************************************************

# Load historical prices

#******************************************************************

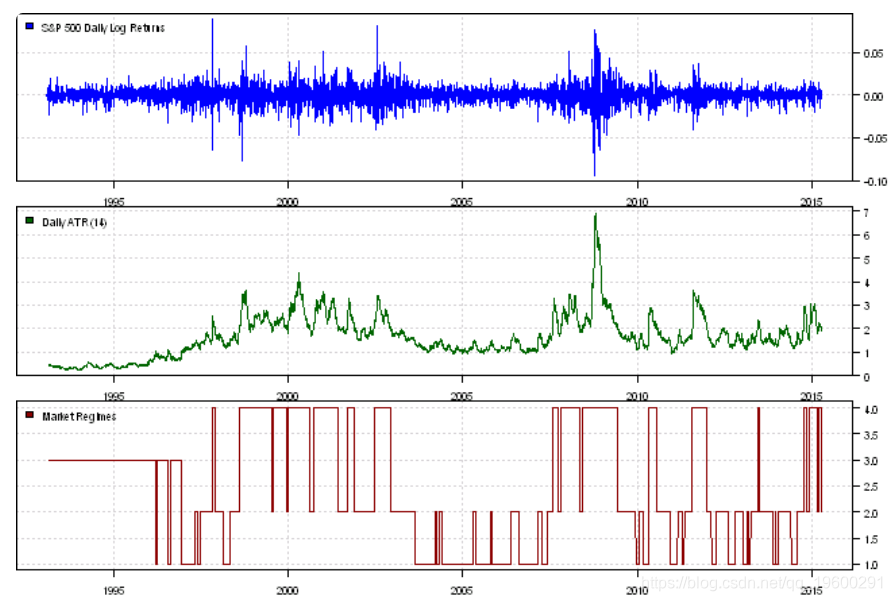

data = env()

getSymbols('SPY', src = 'yahoo', from = '1970-01-01', env = data, auto.assign = T)

price = Cl(data$SPY)

open = Op(data$SPY)

ret = diff(log(price))

ret = log(price) - log(open)

atr = ATR(HLC(data$SPY))[,'atr']

fm2 = fit(mod, verbose = FALSE)使用logLik在迭代30处收敛:18358.98

print(summary(fm2))

Initial state probabilties model pr1 pr2 pr3 pr4 0 0 1 0

Transition matrix toS1 toS2 toS3 toS4 fromS1 9.821940e-01 1.629595e-02 1.510069e-03 8.514403e-45 fromS2 1.167011e-02 9.790209e-01 8.775478e-68 9.308946e-03 fromS3 3.266616e-03 8.586650e-47 9.967334e-01 1.350529e-69 fromS4 3.608394e-65 1.047516e-02 1.922545e-130 9.895248e-01

Response parameters Resp 1 : gaussian Resp 2 : gaussian Re1.(Intercept) Re1.sd Re2.(Intercept) Re2.sd St1 2.897594e-04 0.006285514 1.1647547 0.1181514 St2 -6.980187e-05 0.008186433 1.6554049 0.1871963 St3 2.134584e-04 0.005694483 0.4537498 0.1564576 St4 -4.459161e-04 0.015419207 2.7558362 0.7297283

Re1.(Intercept) Re1.sd Re2.(Intercept) Re2.sd

St1 0.000289759401378951 0.00628551404616354 1.16475474419891 0.118151350440916

St2 -6.98018749098021e-05 0.00818643307634358 1.65540488736983 0.187196307284941

St3 0.000213458358141314 0.00569448330115608 0.453749781945066 0.156457606460757

St4 -0.00044591612667264 0.0154192070819596 2.75583620018895 0.72972830143278

probs = posterior(fm2)

print(head(probs))rownames(x) state S1 S2 S3 S4

1 3 0 0 1 0

2 3 0 0 1 0

3 3 0 0 1 0

4 3 0 0 1 0

5 3 0 0 1 0

6 3 0 0 1 0

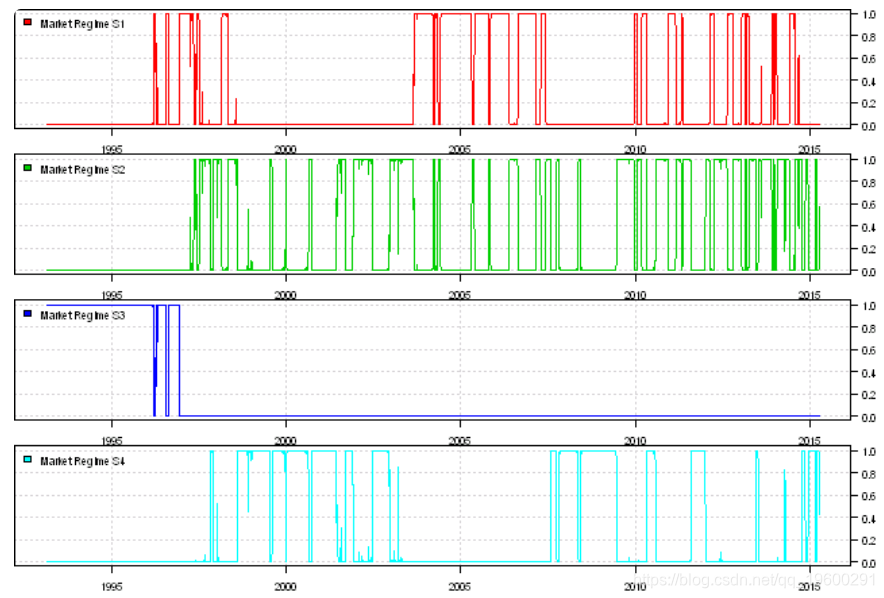

layout(1:3)

plota(temp, type='l', col='darkred')

plota.legend('Market Regimes', 'darkred')

![]()

layout(1:4)

![]()

▍关注我们

【大数据部落】第三方数据服务提供商,提供全面的统计分析与数据挖掘咨询服务,为客户定制个性化的数据解决方案与行业报告等。

▍咨询链接:http://y0.cn/teradat

▍联系邮箱:3025393450@qq.com