How and when: ridge regression with glmnet

@drsimonj here to show you how to conduct ridge regression (linear regression with L2 regularization) in R using the glmnet package, and use simulations to demonstrate its relative advantages over ordinary least squares regression.

Ridge regression

Ridge regression uses L2 regularisation to weight/penalise residuals when the parameters of a regression model are being learned. In the context of linear regression, it can be compared to Ordinary Least Square (OLS). OLS defines the function by which parameter estimates (intercepts and slopes) are calculated. It involves minimising the sum of squared residuals. L2 regularisation is a small addition to the OLS function that weights residuals in a particular way to make the parameters more stable. The outcome is typically a model that fits the training data less well than OLS but generalises better because it is less sensitive to extreme variance in the data such as outliers.

Packages

We’ll make use of the following packages in this post:

library(tidyverse)

library(broom)

library(glmnet)

Ridge regression with glmnet

The glmnet package provides the functionality for ridge regression viaglmnet(). Important things to know:

- Rather than accepting a formula and data frame, it requires a vector input and matrix of predictors.

- You must specify

alpha = 0for ridge regression. - Ridge regression involves tuning a hyperparameter, lambda.

glmnet()will generate default values for you. Alternatively, it is common practice to define your own with thelambdaargument (which we’ll do).

Here’s an example using the mtcars data set:

y <- mtcars$hp

x <- mtcars %>% select(mpg, wt, drat) %>% data.matrix()

lambdas <- 10^seq(3, -2, by = -.1)

fit <- glmnet(x, y, alpha = 0, lambda = lambdas)

summary(fit)

#> Length Class Mode

#> a0 51 -none- numeric

#> beta 153 dgCMatrix S4

#> df 51 -none- numeric

#> dim 2 -none- numeric

#> lambda 51 -none- numeric

#> dev.ratio 51 -none- numeric

#> nulldev 1 -none- numeric

#> npasses 1 -none- numeric

#> jerr 1 -none- numeric

#> offset 1 -none- logical

#> call 5 -none- call

#> nobs 1 -none- numeric

Because, unlike OLS regression done with lm(), ridge regression involves tuning a hyperparameter, lambda, glmnet() runs the model many times for different values of lambda. We can automatically find a value for lambda that is optimal by using cv.glmnet() as follows:

cv_fit <- cv.glmnet(x, y, alpha = 0, lambda = lambdas)

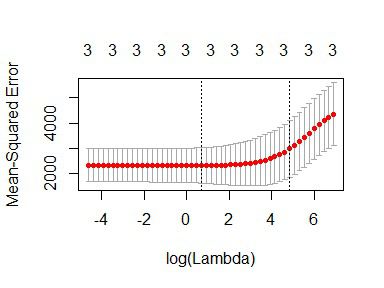

cv.glmnet() uses cross-validation to work out how well each model generalises, which we can visualise as:

plot(cv_fit)

The lowest point in the curve indicates the optimal lambda: the log value of lambda that best minimised the error in cross-validation. We can extract this values as:

opt_lambda <- cv_fit$lambda.min

opt_lambda

#> [1] 3.162278

And we can extract all of the fitted models (like the object returned byglmnet()) via:

fit <- cv_fit$glmnet.fit

summary(fit)

#> Length Class Mode

#> a0 51 -none- numeric

#> beta 153 dgCMatrix S4

#> df 51 -none- numeric

#> dim 2 -none- numeric

#> lambda 51 -none- numeric

#> dev.ratio 51 -none- numeric

#> nulldev 1 -none- numeric

#> npasses 1 -none- numeric

#> jerr 1 -none- numeric

#> offset 1 -none- logical

#> call 5 -none- call

#> nobs 1 -none- numeric

These are the two things we need to predict new data. For example, predicting values and computing an R2 value for the data we trained on:

y_predicted <- predict(fit, s = opt_lambda, newx = x)

# Sum of Squares Total and Error

sst <- sum(y^2)

sse <- sum((y_predicted - y)^2)

# R squared

rsq <- 1 - sse / sst

rsq

#> [1] 0.9318896

The optimal model has accounted for 93% of the variance in the training data.

Ridge v OLS simulations

By producing more stable parameters than OLS, ridge regression should be less prone to overfitting training data. Ridge regression might, therefore, predict training data less well than OLS, but better generalise to new data. This will particularly be the case when extreme variance in the training data is high, which tends to happen when the sample size is low and/or the number of features is high relative to the number of observations.

Below is a simulation experiment I created to compare the prediction accuracy of ridge regression and OLS on training and test data.

I first set up the functions to run the simulation:

# Compute R^2 from true and predicted values

rsquare <- function(true, predicted) {

sse <- sum((predicted - true)^2)

sst <- sum(true^2)

rsq <- 1 - sse / sst

# For this post, impose floor...

if (rsq < 0) rsq <- 0

return (rsq)

}

# Train ridge and OLS regression models on simulated data set with `n_train`

# observations and a number of features as a proportion to `n_train`,

# `p_features`. Return R squared for both models on:

# - y values of the training set

# - y values of a simualted test data set of `n_test` observations

# - The beta coefficients used to simulate the data

ols_vs_ridge <- function(n_train, p_features, n_test = 200) {

## Simulate datasets

n_features <- floor(n_train * p_features)

betas <- rnorm(n_features)

x <- matrix(rnorm(n_train * n_features), nrow = n_train)

y <- x %*% betas + rnorm(n_train)

train <- data.frame(y = y, x)

x <- matrix(rnorm(n_test * n_features), nrow = n_test)

y <- x %*% betas + rnorm(n_test)

test <- data.frame(y = y, x)

## OLS

lm_fit <- lm(y ~ ., train)

# Match to beta coefficients

lm_betas <- tidy(lm_fit) %>%

filter(term != "(Intercept)") %>%

{.$estimate}

lm_betas_rsq <- rsquare(betas, lm_betas)

# Fit to training data

lm_train_rsq <- glance(lm_fit)$r.squared

# Fit to test data

lm_test_yhat <- predict(lm_fit, newdata = test)

lm_test_rsq <- rsquare(test$y, lm_test_yhat)

## Ridge regression

lambda_vals <- 10^seq(3, -2, by = -.1) # Lambda values to search

cv_glm_fit <- cv.glmnet(as.matrix(train[,-1]), train$y, alpha = 0, lambda = lambda_vals, nfolds = 5)

opt_lambda <- cv_glm_fit$lambda.min # Optimal Lambda

glm_fit <- cv_glm_fit$glmnet.fit

# Match to beta coefficients

glm_betas <- tidy(glm_fit) %>%

filter(term != "(Intercept)", lambda == opt_lambda) %>%

{.$estimate}

glm_betas_rsq <- rsquare(betas, glm_betas)

# Fit to training data

glm_train_yhat <- predict(glm_fit, s = opt_lambda, newx = as.matrix(train[,-1]))

glm_train_rsq <- rsquare(train$y, glm_train_yhat)

# Fit to test data

glm_test_yhat <- predict(glm_fit, s = opt_lambda, newx = as.matrix(test[,-1]))

glm_test_rsq <- rsquare(test$y, glm_test_yhat)

data.frame(

model = c("OLS", "Ridge"),

betas_rsq = c(lm_betas_rsq, glm_betas_rsq),

train_rsq = c(lm_train_rsq, glm_train_rsq),

test_rsq = c(lm_test_rsq, glm_test_rsq)

)

}

# Function to run `ols_vs_ridge()` `n_replications` times

repeated_comparisons <- function(..., n_replications = 5) {

map(seq(n_replications), ~ ols_vs_ridge(...)) %>%

map2(seq(.), ~ mutate(.x, replicate = .y)) %>%

reduce(rbind)

}

Now run the simulations for varying numbers of training data and relative proportions of features (takes some time):

d <- purrr::cross_d(list(

n_train = seq(20, 200, 20),

p_features = seq(.55, .95, .05)

))

d <- d %>%

mutate(results = map2(n_train, p_features, repeated_comparisons))

Visualise the results…

For varying numbers of training data (averaging over number of features), how well do both models predict the training and test data?

d %>%

unnest() %>%

group_by(model, n_train) %>%

summarise(

train_rsq = mean(train_rsq),

test_rsq = mean(test_rsq)) %>%

gather(data, rsq, contains("rsq")) %>%

mutate(data = gsub("_rsq", "", data)) %>%

ggplot(aes(n_train, rsq, color = model)) +

geom_line() +

geom_point(size = 4, alpha = .3) +

facet_wrap(~ data) +

theme_minimal() +

labs(x = "Number of training observations",

y = "R squared")

As hypothesised, OLS fits the training data better but Ridge regression better generalises to new test data. Further, these effects are more pronounced when the number of training observations is low.

For varying relative proportions of features (averaging over numbers of training data) how well do both models predict the training and test data?

d %>%

unnest() %>%

group_by(model, p_features) %>%

summarise(

train_rsq = mean(train_rsq),

test_rsq = mean(test_rsq)) %>%

gather(data, rsq, contains("rsq")) %>%

mutate(data = gsub("_rsq", "", data)) %>%

ggplot(aes(p_features, rsq, color = model)) +

geom_line() +

geom_point(size = 4, alpha = .3) +

facet_wrap(~ data) +

theme_minimal() +

labs(x = "Number of features as proportion\nof number of observation",

y = "R squared")

Again, OLS has performed slightly better on training data, but Ridge better on test data. The effects are more pronounced when the number of features is relatively high compared to the number of training observations.

The following plot helps to visualise the relative advantage (or disadvantage) of Ridge to OLS over the number of observations and features:

d %>%

unnest() %>%

group_by(model, n_train, p_features) %>%

summarise(train_rsq = mean(train_rsq),

test_rsq = mean(test_rsq)) %>%

group_by(n_train, p_features) %>%

summarise(RidgeAdvTrain = train_rsq[model == "Ridge"] - train_rsq[model == "OLS"],

RidgeAdvTest = test_rsq[model == "Ridge"] - test_rsq[model == "OLS"]) %>%

gather(data, RidgeAdvantage, contains("RidgeAdv")) %>%

mutate(data = gsub("RidgeAdv", "", data)) %>%

ggplot(aes(n_train, p_features, fill = RidgeAdvantage)) +

scale_fill_gradient2(low = "red", high = "green") +

geom_tile() +

theme_minimal() +

facet_wrap(~ data) +

labs(x = "Number of training observations",

y = "Number of features as proportion\nof number of observation") +

ggtitle("Relative R squared advantage of Ridge compared to OLS")

This shows the combined effect: that Ridge regression better transfers to test data when the number of training observations is low and/or the number of features is high relative to the number of training observations. OLS performs slightly better on the training data under similar conditions, indicating that it is more prone to overfitting training data than when ridge regularisation is employed.

Sign off

Thanks for reading and I hope this was useful for you.

For updates of recent blog posts, follow @drsimonj on Twitter, or email me atdrsimonjackson@gmail.com to get in touch.

If you’d like the code that produced this blog, check out the blogR GitHub repository.

转自:https://drsimonj.svbtle.com/ridge-regression-with-glmnet

浙公网安备 33010602011771号

浙公网安备 33010602011771号