数据挖掘

0 上手前准备

首先看数据集意义,确定以哪个数据集为基层数据通过添加特征丰富数据,最后形成训练集。

然后看预测结果集的格式,对于二分类问题是形成最终的预测(如0,1)还是预测概率(如5e^-4)。

最重要的是要看手册,避免自身操作带来的失误。

1 数据挖掘基础操作

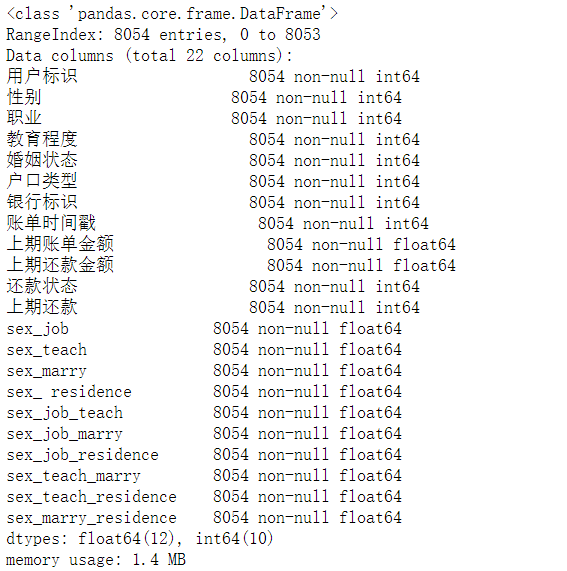

1.1 查看表

p = pd.read_csv('../data/A/test_prof_bill.csv')

p.head()

查看表的前五行,方便简单了解数据的大致内容和数值例子。

p.info()

具体查看表的组成,包括列名,列中元素的类型,空值情况

import os

import seaborn as sns

import matplotlib.pyplot as plt

color = sns.color_palette()

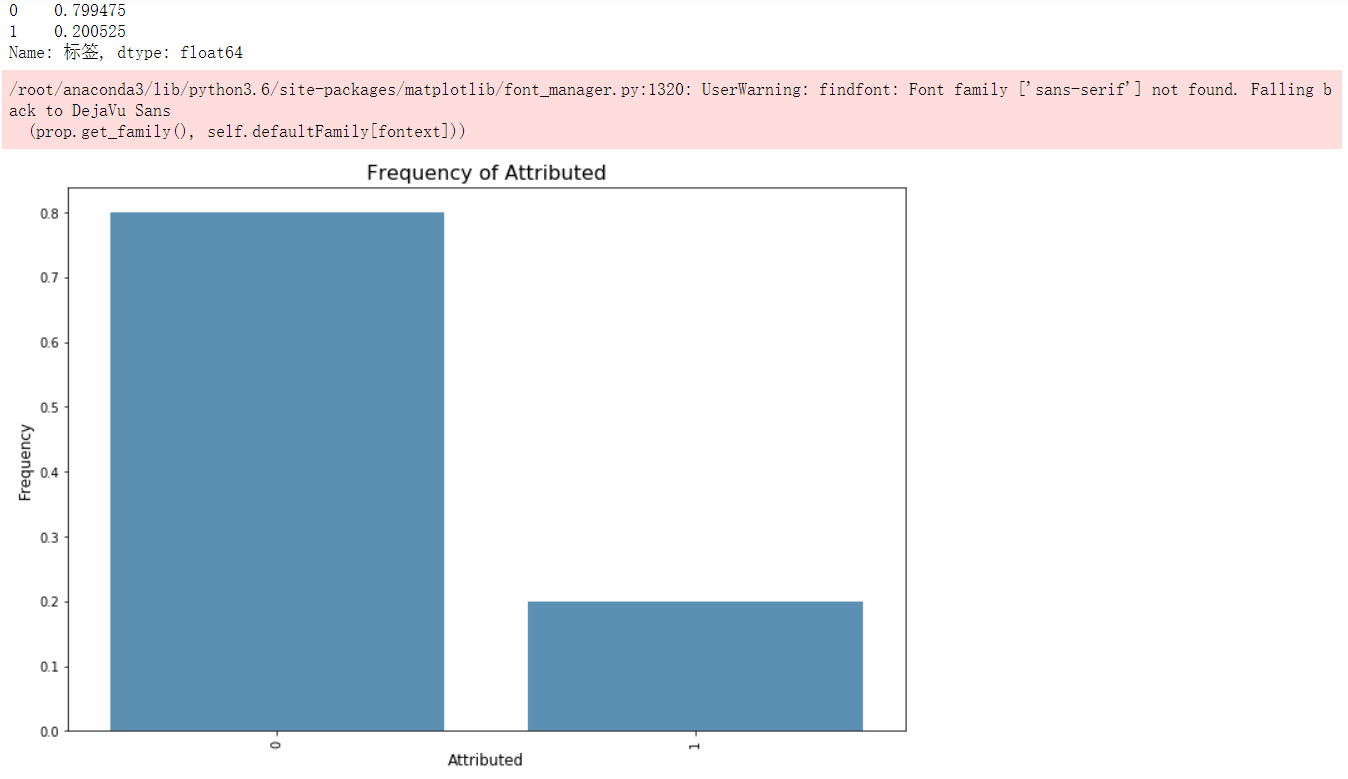

group_df = train_L.标签.value_counts().reset_index()

k = group_df['标签'].sum()

plt.figure(figsize = (12,8))

sns.barplot(group_df['index'], (group_df.标签/k), alpha=0.8, color=color[0])

print((group_df.标签/k))

plt.ylabel('Frequency', fontsize = 12)

plt.xlabel('Attributed', fontsize = 12)

plt.title('Frequency of Attributed', fontsize = 16)

plt.xticks(rotation='vertical')

plt.show()

表中某一列分布情况概览,这种方法主要用于数据中正负样本的统计,根据统计结果可一选择采样比例。

1.2 查看各个基础特征对结果的影响因子

colormap = plt.cm.viridis

plt.figure(figsize=(16,16))

plt.title(' The Absolute Correlation Coefficient of Features', y=1.05, size=15)

sns.heatmap(abs(bg.astype(float).corr()),linewidths=0.1,vmax=1.0, square=True, cmap=colormap, linecolor='white', annot=True, )

plt.show()

以协方差为衡量指标,绘制可视化界面

1.3 形成新特征

仅以一例说明,在本数据中有一行为的七个种类,分别为ABCDEFG,这七种行为的发生次数比例会对结果有不错的影响:

现将这七种行为的发生次数按照用户统计,分别统计了用户某一行为的发生次数和用户总行为次数:

count = p1.groupby(['用户标识','行为类型']).count()

maxi = p1.groupby(['用户标识','行为类型']).max()

然后将两个临时表合并一下:

merge = pd.merge(c,a,how='left',on='用户标识') #选择左连接方式

计算出来的每一行为几率作为一个特征:

with open('../data/A/behavier_ratio.csv','rt', encoding="utf-8") as csvfile:

reader = csv.reader(csvfile)

next(csvfile)

writefile = open('../data/A/behavier_analy.csv','w+',newline='')

writer = csv.writer(writefile)

flag = 1

user = '1'

tmp = []

l = []

for raw in reader:

if(raw[0] != user):

flag = 0

user = raw[0]

if(flag == 0):

if(len(l) != 0):

writer.writerow(l)

l = [0.0,0.0,0.0,0.0,0.0,0.0,0.0,0.0,0.0]

l[0] = raw[0]

l[int(raw[1])+1] = raw[4]

flag = 1

else:

l[int(raw[1])+1]=raw[4]

tmp = l

writer.writerow(tmp)

csvfile.close()

writefile.close()

由于数据本身原因,在转变的过程中会产生空值的现象,可以暴力填补:

a.fillna(0,inplace=True)

注意,若不添加inplace参数的话是不会在原有基础上进行填补

1.4 无用特征的删除

a = a.drop(['Unnamed: 0'],1)

1.5 结果的存取

正常来说,读取这样既可:

total.to_csv('../data/A/total_del.csv')

c = pd.read_csv('../data/A/count_del.csv')

但是会出现,表中没有标题行的情况:

b = pd.read_csv('../data/A/bankStatement_analy.csv',header=None, names = ['用户标识','type0_ratio','type1_ratio','type0_money','type1_money'])

a.to_csv('../data/A/test_3.csv',index=False)

2 模型的选取与优化

本次选用xgboost模型,使用贝叶斯优化器进行最优参数的选取:

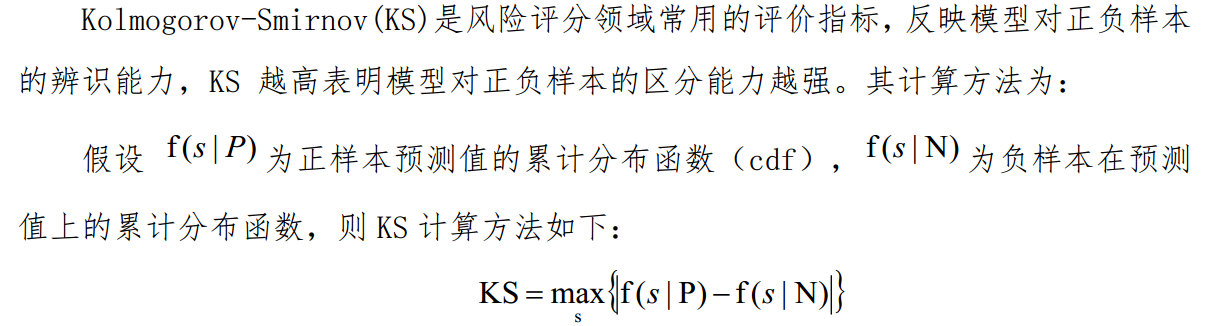

对于评价函数,本次比赛使用KS值,因为一直用的是auc评价函数,因此前期吃了不少亏。

对于贝叶斯优化器来说,默认的评价函数并没有ks,因此需要自己实现:

def eval_ks(estimator,x,y):

preds = estimator.predict_proba(x) #获取预测的概率

preds = preds[:,1]

fpr, tpr, thresholds = metrics.roc_curve(y, preds) #传入真实值,预测值,获取正样本、负样本以及判别正负样本的阈值

ks = 0

for i in range(len(thresholds)):

if abs(tpr[i] - fpr[i]) > ks:

ks = abs(tpr[i] - fpr[i])

print('KS score = ',ks)

return ks

通过查看官方手册可知,自定义评价函数需要传入三个参数

import pandas as pd

import numpy as np

import xgboost as xgb

import lightgbm as lgb

from skopt import BayesSearchCV

from sklearn.model_selection import StratifiedKFold

# SETTINGS - CHANGE THESE TO GET SOMETHING MEANINGFUL

ITERATIONS = 100 # 1000

TRAINING_SIZE = 100000 # 20000000

TEST_SIZE = 40000

# Load data

train = pd.read_csv(

'../data/step2/train2_1.csv'

)

X = train.drop(['label'],1)

Y = train['label']

bayes_cv_tuner = BayesSearchCV(

estimator = xgb.XGBClassifier(

n_jobs = 1,

objective = 'binary:logistic',

eval_metric = 'auc',

silent=1,

tree_method='approx'

),

search_spaces = {

'learning_rate': (0.01, 1.0, 'log-uniform'),

'min_child_weight': (0, 10),

'max_depth': (0, 50),

'max_delta_step': (0, 20),

'subsample': (0.01, 1.0, 'uniform'),

'colsample_bytree': (0.01, 1.0, 'uniform'),

'colsample_bylevel': (0.01, 1.0, 'uniform'),

'reg_lambda': (1e-9, 1000, 'log-uniform'),

'reg_alpha': (1e-9, 1.0, 'log-uniform'),

'gamma': (1e-9, 0.5, 'log-uniform'),

'min_child_weight': (0, 5),

'n_estimators': (50, 100),

'scale_pos_weight': (1e-6, 500, 'log-uniform')

},

scoring = eval_ks,

cv = StratifiedKFold(

n_splits=3,

shuffle=True,

random_state=42

),

n_jobs = 3,

n_iter = ITERATIONS,

verbose = 0,

refit = True,

random_state = 42

)

result = bayes_cv_tuner.fit(X.values, Y.values)

all_models = pd.DataFrame(bayes_cv_tuner.cv_results_)

best_params = pd.Series(bayes_cv_tuner.best_params_)

print('Model #{}\nBest ROC-AUC: {}\nBest params: {}\n'.format(

len(all_models),

np.round(bayes_cv_tuner.best_score_, 4),

bayes_cv_tuner.best_params_

))

# Save all model results

clf_name = bayes_cv_tuner.estimator.__class__.__name__

all_models.to_csv('../data/_cv_results.csv')

训练结果是定义的迭代次数中,分数最好的参数配置,使用该参数配置应用于测试集的预测:

import csv

test = pd.read_csv('../data/B/test2_1.csv')

clf = xgb.XGBClassifier(colsample_bylevel= 0.782142304086966, colsample_bytree= 0.9019863190224396, gamma= 0.0001491431487281734, learning_rate= 0.1675067687563292, max_delta_step= 3,max_depth= 10, min_child_weight= 4, n_estimators= 76, reg_alpha= 0.0026534914283041435, reg_lambda= 211.46421106591836, scale_pos_weight= 0.5414848749017023, subsample= 0.8406121867576984)

clf.fit(X,Y)

preds = clf.predict_proba(test) #该函数产生的是概率,predict函数产生的是0,1结果

upload = pd.DataFrame()

upload['客户号'] = test['用户标识']

upload['违约概率'] = preds[:,1] #注意,模型训练出来的结果是两列,第一列是预测为0的概率,第二列是预测为1的概率,根据题意,取为1的概率作为最终概率

upload.to_csv('../data/A/upload.csv',index=False)

with open('../data/A/upload.csv','rt', encoding="utf-8") as csvfile:

reader = csv.reader(csvfile)

next(csvfile)

writefile = open('../data/A/up.csv','w+',newline='')

writer = csv.writer(writefile)

for raw in reader:

writer.writerow(raw)

csvfile.close()

writefile.close()

浙公网安备 33010602011771号

浙公网安备 33010602011771号