前言

原文来源:这里!

数据集:根据不同人的数据来判断他有没有可能再次偿还信用借款(Home credit default risk)

看完的感想是:

- 每个不同的数据集的数据都是不一样的,背后表现的现象也是有差异。

- 但是还是有处理数据的规律和套路可以值得学习的。

- 本文是特征工程处理的第一章,提供了一些简单的方法来新建特征数据,之后还有2章讲述新的方法

原文的工作流程:outline of a machine learning project

- 理解问题,数据背景(understand the problem and the data)

- 数据清理和格式清理(data cleaning and formatting)

- EDA研究数据

- 使用数据建立最简单的模型(baseline model) ----> 线性回归line regression比如说(得到最低的acc,然后之后都要在这个基础上改进,不能比这个还差)

- 改进模型(improved model)----> 使用特征工程改进的数据或者使用新的模型

- 对于模型进行基本解释(model interpretaion) ---> 为啥比baseline好等等的总结

特征工程feature engineering

- 下面列举本文新建特征数据的几个方法,本文新建的角度有两种:

-

- 从统计学的角度

-

- 从应用场景的背景知识来的角度(domain knowledge)

-

- 本文还强调了kaggle的关键也就是特征工程,好的特征可以比起HP Tuning和模型选择更能促进gradient boosting,从而获得高acc。

- 特征工程是:

- 新建特征

- 选择重要特征(删除其他不需要的特征):从而reduce dimentionality的集合

统计学的角度

- 多项式特征

我们本来有['EXT_SOURCE_1', 'EXT_SOURCE_2', 'EXT_SOURCE_3', 'DAYS_BIRTH']这些特征,然后我们可以将他们两两组合(degree=2)变成下面的特征组合。

['1',

'EXT_SOURCE_1',

'EXT_SOURCE_2',

'EXT_SOURCE_3',

'DAYS_BIRTH',

'EXT_SOURCE_1^2',

'EXT_SOURCE_1 EXT_SOURCE_2',

'EXT_SOURCE_1 EXT_SOURCE_3',

'EXT_SOURCE_1 DAYS_BIRTH',

'EXT_SOURCE_2^2',

'EXT_SOURCE_2 EXT_SOURCE_3',

'EXT_SOURCE_2 DAYS_BIRTH',

'EXT_SOURCE_3^2',

'EXT_SOURCE_3 DAYS_BIRTH',

'DAYS_BIRTH^2']

实现方法:

from sklearn.preprocessing import PolynomialFeatures

# Make a new dataframe for polynomial features

poly_features = app_train[['EXT_SOURCE_1', 'EXT_SOURCE_2', 'EXT_SOURCE_3', 'DAYS_BIRTH', 'TARGET']]

# Create the polynomial object with specified degree

poly_transformer = PolynomialFeatures(degree = 3)

# Train the polynomial features

poly_transformer.fit(poly_features)

# Transform the features

poly_features = poly_transformer.transform(poly_features)

注:对于poly的新特征有必要用scaler来调整一些参数取值范围(原文用了minmaxscaler)

从经济学的角度(domain knowledge)

CREDIT_INCOME_PERCENT: 借贷与收入比 the percentage of the credit amount relative to a client's income

ANNUITY_INCOME_PERCENT: 贷款年金和收入比the percentage of the loan annuity relative to a client's income

CREDIT_TERM: 连续还款月长度 the length of the payment in months (since the annuity is the monthly amount due

DAYS_EMPLOYED_PERCENT: 受雇佣天数与年龄比the percentage of the days employed relative to the client's age

实现方式

app_train_domain['CREDIT_INCOME_PERCENT'] = app_train_domain['AMT_CREDIT'] / app_train_domain['AMT_INCOME_TOTAL']

app_train_domain['ANNUITY_INCOME_PERCENT'] = app_train_domain['AMT_ANNUITY'] / app_train_domain['AMT_INCOME_TOTAL']

app_train_domain['CREDIT_TERM'] = app_train_domain['AMT_ANNUITY'] / app_train_domain['AMT_CREDIT']

app_train_domain['DAYS_EMPLOYED_PERCENT'] = app_train_domain['DAYS_EMPLOYED'] / app_train_domain['DAYS_BIRTH']

其他

除了重点是特征工程以外,本文还提供了一些新的画图/处理数据的方法,这里简单总结一下

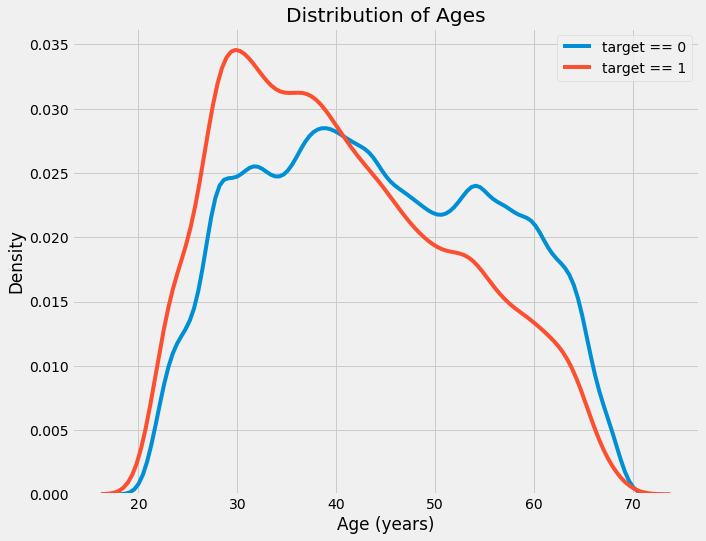

1.画图

- sns.kdeplot: 内核密度函数kernel density estimation

也就是之前sns.distplot之后hist的拟合曲线?

plt.figure(figsize = (10, 8))

# KDE plot of loans that were repaid on time

sns.kdeplot(app_train.loc[app_train['TARGET'] == 0, 'DAYS_BIRTH'] / 365, label = 'target == 0')

# KDE plot of loans which were not repaid on time

sns.kdeplot(app_train.loc[app_train['TARGET'] == 1, 'DAYS_BIRTH'] / 365, label = 'target == 1')

# Labeling of plot

plt.xlabel('Age (years)'); plt.ylabel('Density'); plt.title('Distribution of Ages');

- 如何通过kde看出相关性:比如下图EXT_SOURCE_3比起其他2个更能分辨出target=0/1的区别,那就说明EXT_SOURCE_3比起其他2个更好,更有相关性。

2.发现样本目标值不均衡怎么办?

- 在训练器里面加权目标值:weight classes(XGBOOST)

- 其他解决方法看这里:这里

- 下面有class_weight = 'balanced'参数

# Create the model

model = lgb.LGBMClassifier(n_estimators=10000, objective = 'binary',

class_weight = 'balanced', learning_rate = 0.05,

reg_alpha = 0.1, reg_lambda = 0.1,

subsample = 0.8, n_jobs = -1, random_state = 50)

3.查看数据集里面所有categorical里面的Unique数量

# Number of unique classes in each object column

app_train.select_dtypes('object').apply(pd.Series.nunique, axis = 0)

4.对于categorical的encoding

原文给出的是

小于2个的categorical ---> label encoding

from sklearn.preprocessing import LabelEncoder

le = LabelEncoder()

le.fit(app_train[col])

app_train[col] = le.transform(app_train[col])

大于2个的 ---> one-hot encoding

pd.get_dummies(app_train[col])

5.如何对齐align训练集和测试集

最后训练集要比测试集多一列:target

align的理由是在one-hot encoding之后:训练集可能比测试集多出几列(训练集里面存在的categorical值,在测试集里面不存在)

下面是对齐的实现,注意要事先把target拿出来,防止被align的时候删除。

train_labels = app_train['TARGET']

# Align the training and testing data, keep only columns present in both dataframes

app_train, app_test = app_train.align(app_test, join = 'inner', axis = 1)

# Add the target back in

app_train['TARGET'] = train_labels

print('Training Features shape: ', app_train.shape)

print('Testing Features shape: ', app_test.shape)

得到

Training Features shape: (307511, 240)

Testing Features shape: (48744, 239)

6.对于相关性的评估

.00-.19 “very weak”

.20-.39 “weak”

.40-.59 “moderate”

.60-.79 “strong”

.80-1.0 “very strong”

7.简单replace一个值

可以用切片或者df.replace

# Replace the anomalous values with nan

app_train['DAYS_EMPLOYED'].replace({365243: np.nan}, inplace = True)

8.处理outlier/anomalies

将其变成nan,然后之后会在处理nan(插补imputation)的时候一同处理。

9.神奇的anomalies

原文发现有些人的年龄超过了1000岁(异常值)而且这些人欠款违约(default loan)的概率比一般人还小。

anom = app_train[app_train['DAYS_EMPLOYED'] == 365243]

non_anom = app_train[app_train['DAYS_EMPLOYED'] != 365243]

print('The non-anomalies default on %0.2f%% of loans' % (100 * non_anom['TARGET'].mean()))

print('The anomalies default on %0.2f%% of loans' % (100 * anom['TARGET'].mean()))

print('There are %d anomalous days of employment' % len(anom))

得到只有5.4%的人违约欠款了。

The non-anomalies default on 8.66% of loans

The anomalies default on 5.40% of loans

There are 55374 anomalous days of employment

10.插补Imputer填充nan

之前都是直接df.fillna(df.mean()),这里用了Imputer

from sklearn.preprocessing import MinMaxScaler, Imputer

# Median imputation of missing values

imputer = Imputer(strategy = 'median')

# Fit on the training data

imputer.fit(train)

# Transform both training and testing data

train = imputer.transform(train)

11.训练完后展示重要的特征feature_importance

sklearn的基本每个classifer都有feature_importances_这个参数,下面的例子是随机树

# Extract feature importances

feature_importance_values_domain = random_forest_domain.feature_importances_

feature_importances_domain = pd.DataFrame({'feature': domain_features_names, 'importance': feature_importance_values_domain})

获取到之后就可以用barplot来显示

def plot_feature_importances(df):

"""

Plot importances returned by a model. This can work with any measure of

feature importance provided that higher importance is better.

Args:

df (dataframe): feature importances. Must have the features in a column

called `features` and the importances in a column called `importance

Returns:

shows a plot of the 15 most importance features

df (dataframe): feature importances sorted by importance (highest to lowest)

with a column for normalized importance

"""

# Sort features according to importance

df = df.sort_values('importance', ascending = False).reset_index()

# Normalize the feature importances to add up to one

df['importance_normalized'] = df['importance'] / df['importance'].sum()

# Make a horizontal bar chart of feature importances

plt.figure(figsize = (10, 6))

ax = plt.subplot()

# Need to reverse the index to plot most important on top

ax.barh(list(reversed(list(df.index[:15]))),

df['importance_normalized'].head(15),

align = 'center', edgecolor = 'k')

# Set the yticks and labels

ax.set_yticks(list(reversed(list(df.index[:15]))))

ax.set_yticklabels(df['feature'].head(15))

# Plot labeling

plt.xlabel('Normalized Importance'); plt.title('Feature Importances')

plt.show()

return df

# Show the feature importances for the default features

feature_importances_sorted = plot_feature_importances(feature_importances)