import pandas as pd

import numpy as np

0. 案例引入

# 由np直接生成的ndarray

stock_change = np.random.normal(0, 1, (10, 8))

stock_change

array([[ 0.74057955, 0.78604657, -0.15264135, 0.05680483, 0.09388135,

0.7313751 , -1.52338443, 1.71156505],

[ 0.42204925, 0.62541715, -1.41583042, -0.27434654, 0.98587136,

-0.55797884, 0.31026482, -0.47964535],

[ 0.99741102, -0.94397298, -0.40782973, -1.33631227, -0.0124836 ,

1.1873408 , -0.25430393, -0.74264106],

[ 0.34156662, -0.40621262, 0.82861416, 0.1272128 , 1.04101412,

0.79061324, -0.60325544, 1.29954581],

[-1.23289547, 0.83789748, 1.19276989, 0.45092868, -1.7418129 ,

-0.65362211, -0.17752493, 1.87679286],

[-0.4268705 , 1.14017572, 0.18261009, -0.28947877, 0.82489897,

0.11566058, -0.53191371, -0.96065812],

[ 0.92792797, 0.26086313, 0.08316582, -0.94533007, -0.77956139,

0.23006703, -0.81971461, -1.36742474],

[ 0.82241768, 0.54201367, -0.19331564, 0.50576697, -0.42545839,

-0.24247517, -0.03526651, -0.02268451],

[ 1.67480093, -1.23265948, -2.88199942, -1.07761987, -1.37844497,

-0.13581683, 2.06013919, 1.18986057],

[ 0.60744357, 0.52348326, 0.76418263, -0.73385554, 0.54857341,

0.27310645, -0.26464179, 0.77370496]])

# 通过pd.DataFrame生成 (pd.DataFrame(ndarray))

stock_df = pd.DataFrame(stock_change)

stock_df

|

0 |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

| 0 |

0.740580 |

0.786047 |

-0.152641 |

0.056805 |

0.093881 |

0.731375 |

-1.523384 |

1.711565 |

| 1 |

0.422049 |

0.625417 |

-1.415830 |

-0.274347 |

0.985871 |

-0.557979 |

0.310265 |

-0.479645 |

| 2 |

0.997411 |

-0.943973 |

-0.407830 |

-1.336312 |

-0.012484 |

1.187341 |

-0.254304 |

-0.742641 |

| 3 |

0.341567 |

-0.406213 |

0.828614 |

0.127213 |

1.041014 |

0.790613 |

-0.603255 |

1.299546 |

| 4 |

-1.232895 |

0.837897 |

1.192770 |

0.450929 |

-1.741813 |

-0.653622 |

-0.177525 |

1.876793 |

| 5 |

-0.426871 |

1.140176 |

0.182610 |

-0.289479 |

0.824899 |

0.115661 |

-0.531914 |

-0.960658 |

| 6 |

0.927928 |

0.260863 |

0.083166 |

-0.945330 |

-0.779561 |

0.230067 |

-0.819715 |

-1.367425 |

| 7 |

0.822418 |

0.542014 |

-0.193316 |

0.505767 |

-0.425458 |

-0.242475 |

-0.035267 |

-0.022685 |

| 8 |

1.674801 |

-1.232659 |

-2.881999 |

-1.077620 |

-1.378445 |

-0.135817 |

2.060139 |

1.189861 |

| 9 |

0.607444 |

0.523483 |

0.764183 |

-0.733856 |

0.548573 |

0.273106 |

-0.264642 |

0.773705 |

stock_df.shape

(10, 8)

# 添加行索引

stock_name = ['股票{}'.format(i+1) for i in range(stock_df.shape[0])]

stock_df = pd.DataFrame(data=stock_change, index=stock_name)

stock_df

|

0 |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

| 股票1 |

0.740580 |

0.786047 |

-0.152641 |

0.056805 |

0.093881 |

0.731375 |

-1.523384 |

1.711565 |

| 股票2 |

0.422049 |

0.625417 |

-1.415830 |

-0.274347 |

0.985871 |

-0.557979 |

0.310265 |

-0.479645 |

| 股票3 |

0.997411 |

-0.943973 |

-0.407830 |

-1.336312 |

-0.012484 |

1.187341 |

-0.254304 |

-0.742641 |

| 股票4 |

0.341567 |

-0.406213 |

0.828614 |

0.127213 |

1.041014 |

0.790613 |

-0.603255 |

1.299546 |

| 股票5 |

-1.232895 |

0.837897 |

1.192770 |

0.450929 |

-1.741813 |

-0.653622 |

-0.177525 |

1.876793 |

| 股票6 |

-0.426871 |

1.140176 |

0.182610 |

-0.289479 |

0.824899 |

0.115661 |

-0.531914 |

-0.960658 |

| 股票7 |

0.927928 |

0.260863 |

0.083166 |

-0.945330 |

-0.779561 |

0.230067 |

-0.819715 |

-1.367425 |

| 股票8 |

0.822418 |

0.542014 |

-0.193316 |

0.505767 |

-0.425458 |

-0.242475 |

-0.035267 |

-0.022685 |

| 股票9 |

1.674801 |

-1.232659 |

-2.881999 |

-1.077620 |

-1.378445 |

-0.135817 |

2.060139 |

1.189861 |

| 股票10 |

0.607444 |

0.523483 |

0.764183 |

-0.733856 |

0.548573 |

0.273106 |

-0.264642 |

0.773705 |

# 添加列索引

# 引入df.date_range(),start-开始日期, end: 结束日期, periods - 持续时间, frep- B:工作日, M:月, D:天

date = pd.date_range(start='2020-3-30', periods=stock_df.shape[1], freq='d')

date

DatetimeIndex(['2020-03-30', '2020-03-31', '2020-04-01', '2020-04-02',

'2020-04-03', '2020-04-04', '2020-04-05', '2020-04-06'],

dtype='datetime64[ns]', freq='D')

stock_df = pd.DataFrame(stock_change, index=stock_name, columns=date)

stock_df

|

2020-03-30 |

2020-03-31 |

2020-04-01 |

2020-04-02 |

2020-04-03 |

2020-04-04 |

2020-04-05 |

2020-04-06 |

| 股票1 |

0.740580 |

0.786047 |

-0.152641 |

0.056805 |

0.093881 |

0.731375 |

-1.523384 |

1.711565 |

| 股票2 |

0.422049 |

0.625417 |

-1.415830 |

-0.274347 |

0.985871 |

-0.557979 |

0.310265 |

-0.479645 |

| 股票3 |

0.997411 |

-0.943973 |

-0.407830 |

-1.336312 |

-0.012484 |

1.187341 |

-0.254304 |

-0.742641 |

| 股票4 |

0.341567 |

-0.406213 |

0.828614 |

0.127213 |

1.041014 |

0.790613 |

-0.603255 |

1.299546 |

| 股票5 |

-1.232895 |

0.837897 |

1.192770 |

0.450929 |

-1.741813 |

-0.653622 |

-0.177525 |

1.876793 |

| 股票6 |

-0.426871 |

1.140176 |

0.182610 |

-0.289479 |

0.824899 |

0.115661 |

-0.531914 |

-0.960658 |

| 股票7 |

0.927928 |

0.260863 |

0.083166 |

-0.945330 |

-0.779561 |

0.230067 |

-0.819715 |

-1.367425 |

| 股票8 |

0.822418 |

0.542014 |

-0.193316 |

0.505767 |

-0.425458 |

-0.242475 |

-0.035267 |

-0.022685 |

| 股票9 |

1.674801 |

-1.232659 |

-2.881999 |

-1.077620 |

-1.378445 |

-0.135817 |

2.060139 |

1.189861 |

| 股票10 |

0.607444 |

0.523483 |

0.764183 |

-0.733856 |

0.548573 |

0.273106 |

-0.264642 |

0.773705 |

1. Pandas 主要数据结构

1.1 DataFrame

stock_df

|

2020-03-30 |

2020-03-31 |

2020-04-01 |

2020-04-02 |

2020-04-03 |

2020-04-04 |

2020-04-05 |

2020-04-06 |

| 股票1 |

0.740580 |

0.786047 |

-0.152641 |

0.056805 |

0.093881 |

0.731375 |

-1.523384 |

1.711565 |

| 股票2 |

0.422049 |

0.625417 |

-1.415830 |

-0.274347 |

0.985871 |

-0.557979 |

0.310265 |

-0.479645 |

| 股票3 |

0.997411 |

-0.943973 |

-0.407830 |

-1.336312 |

-0.012484 |

1.187341 |

-0.254304 |

-0.742641 |

| 股票4 |

0.341567 |

-0.406213 |

0.828614 |

0.127213 |

1.041014 |

0.790613 |

-0.603255 |

1.299546 |

| 股票5 |

-1.232895 |

0.837897 |

1.192770 |

0.450929 |

-1.741813 |

-0.653622 |

-0.177525 |

1.876793 |

| 股票6 |

-0.426871 |

1.140176 |

0.182610 |

-0.289479 |

0.824899 |

0.115661 |

-0.531914 |

-0.960658 |

| 股票7 |

0.927928 |

0.260863 |

0.083166 |

-0.945330 |

-0.779561 |

0.230067 |

-0.819715 |

-1.367425 |

| 股票8 |

0.822418 |

0.542014 |

-0.193316 |

0.505767 |

-0.425458 |

-0.242475 |

-0.035267 |

-0.022685 |

| 股票9 |

1.674801 |

-1.232659 |

-2.881999 |

-1.077620 |

-1.378445 |

-0.135817 |

2.060139 |

1.189861 |

| 股票10 |

0.607444 |

0.523483 |

0.764183 |

-0.733856 |

0.548573 |

0.273106 |

-0.264642 |

0.773705 |

# 查看DataFrame形状,类似于2d array

stock_df.shape

(10, 8)

# 取行索引

stock_df.index

Index(['股票1', '股票2', '股票3', '股票4', '股票5', '股票6', '股票7', '股票8', '股票9', '股票10'], dtype='object')

# 取列索引

stock_df.columns

DatetimeIndex(['2020-03-30', '2020-03-31', '2020-04-01', '2020-04-02',

'2020-04-03', '2020-04-04', '2020-04-05', '2020-04-06'],

dtype='datetime64[ns]', freq='D')

# 取ndarray的值

stock_df.values

array([[ 0.74057955, 0.78604657, -0.15264135, 0.05680483, 0.09388135,

0.7313751 , -1.52338443, 1.71156505],

[ 0.42204925, 0.62541715, -1.41583042, -0.27434654, 0.98587136,

-0.55797884, 0.31026482, -0.47964535],

[ 0.99741102, -0.94397298, -0.40782973, -1.33631227, -0.0124836 ,

1.1873408 , -0.25430393, -0.74264106],

[ 0.34156662, -0.40621262, 0.82861416, 0.1272128 , 1.04101412,

0.79061324, -0.60325544, 1.29954581],

[-1.23289547, 0.83789748, 1.19276989, 0.45092868, -1.7418129 ,

-0.65362211, -0.17752493, 1.87679286],

[-0.4268705 , 1.14017572, 0.18261009, -0.28947877, 0.82489897,

0.11566058, -0.53191371, -0.96065812],

[ 0.92792797, 0.26086313, 0.08316582, -0.94533007, -0.77956139,

0.23006703, -0.81971461, -1.36742474],

[ 0.82241768, 0.54201367, -0.19331564, 0.50576697, -0.42545839,

-0.24247517, -0.03526651, -0.02268451],

[ 1.67480093, -1.23265948, -2.88199942, -1.07761987, -1.37844497,

-0.13581683, 2.06013919, 1.18986057],

[ 0.60744357, 0.52348326, 0.76418263, -0.73385554, 0.54857341,

0.27310645, -0.26464179, 0.77370496]])

# 取转置

stock_df.T

|

股票1 |

股票2 |

股票3 |

股票4 |

股票5 |

股票6 |

股票7 |

股票8 |

股票9 |

股票10 |

| 2020-03-30 |

0.740580 |

0.422049 |

0.997411 |

0.341567 |

-1.232895 |

-0.426871 |

0.927928 |

0.822418 |

1.674801 |

0.607444 |

| 2020-03-31 |

0.786047 |

0.625417 |

-0.943973 |

-0.406213 |

0.837897 |

1.140176 |

0.260863 |

0.542014 |

-1.232659 |

0.523483 |

| 2020-04-01 |

-0.152641 |

-1.415830 |

-0.407830 |

0.828614 |

1.192770 |

0.182610 |

0.083166 |

-0.193316 |

-2.881999 |

0.764183 |

| 2020-04-02 |

0.056805 |

-0.274347 |

-1.336312 |

0.127213 |

0.450929 |

-0.289479 |

-0.945330 |

0.505767 |

-1.077620 |

-0.733856 |

| 2020-04-03 |

0.093881 |

0.985871 |

-0.012484 |

1.041014 |

-1.741813 |

0.824899 |

-0.779561 |

-0.425458 |

-1.378445 |

0.548573 |

| 2020-04-04 |

0.731375 |

-0.557979 |

1.187341 |

0.790613 |

-0.653622 |

0.115661 |

0.230067 |

-0.242475 |

-0.135817 |

0.273106 |

| 2020-04-05 |

-1.523384 |

0.310265 |

-0.254304 |

-0.603255 |

-0.177525 |

-0.531914 |

-0.819715 |

-0.035267 |

2.060139 |

-0.264642 |

| 2020-04-06 |

1.711565 |

-0.479645 |

-0.742641 |

1.299546 |

1.876793 |

-0.960658 |

-1.367425 |

-0.022685 |

1.189861 |

0.773705 |

# 查看头部几行数据, 默认5行

stock_df.head(5)

# 查看倒数几行数据

stock_df.tail()

|

2020-03-30 |

2020-03-31 |

2020-04-01 |

2020-04-02 |

2020-04-03 |

2020-04-04 |

2020-04-05 |

2020-04-06 |

| 股票6 |

-0.426871 |

1.140176 |

0.182610 |

-0.289479 |

0.824899 |

0.115661 |

-0.531914 |

-0.960658 |

| 股票7 |

0.927928 |

0.260863 |

0.083166 |

-0.945330 |

-0.779561 |

0.230067 |

-0.819715 |

-1.367425 |

| 股票8 |

0.822418 |

0.542014 |

-0.193316 |

0.505767 |

-0.425458 |

-0.242475 |

-0.035267 |

-0.022685 |

| 股票9 |

1.674801 |

-1.232659 |

-2.881999 |

-1.077620 |

-1.378445 |

-0.135817 |

2.060139 |

1.189861 |

| 股票10 |

0.607444 |

0.523483 |

0.764183 |

-0.733856 |

0.548573 |

0.273106 |

-0.264642 |

0.773705 |

1.1.1 设置索引

# 只能通过对整个index 重新赋值, 整行或者整列

data_index = [['股票__{}'.format(i+1) for i in range(stock_df.shape[0])]]

stock_df.index = data_index

stock_df

|

2020-03-30 |

2020-03-31 |

2020-04-01 |

2020-04-02 |

2020-04-03 |

2020-04-04 |

2020-04-05 |

2020-04-06 |

| 股票__1 |

0.740580 |

0.786047 |

-0.152641 |

0.056805 |

0.093881 |

0.731375 |

-1.523384 |

1.711565 |

| 股票__2 |

0.422049 |

0.625417 |

-1.415830 |

-0.274347 |

0.985871 |

-0.557979 |

0.310265 |

-0.479645 |

| 股票__3 |

0.997411 |

-0.943973 |

-0.407830 |

-1.336312 |

-0.012484 |

1.187341 |

-0.254304 |

-0.742641 |

| 股票__4 |

0.341567 |

-0.406213 |

0.828614 |

0.127213 |

1.041014 |

0.790613 |

-0.603255 |

1.299546 |

| 股票__5 |

-1.232895 |

0.837897 |

1.192770 |

0.450929 |

-1.741813 |

-0.653622 |

-0.177525 |

1.876793 |

| 股票__6 |

-0.426871 |

1.140176 |

0.182610 |

-0.289479 |

0.824899 |

0.115661 |

-0.531914 |

-0.960658 |

| 股票__7 |

0.927928 |

0.260863 |

0.083166 |

-0.945330 |

-0.779561 |

0.230067 |

-0.819715 |

-1.367425 |

| 股票__8 |

0.822418 |

0.542014 |

-0.193316 |

0.505767 |

-0.425458 |

-0.242475 |

-0.035267 |

-0.022685 |

| 股票__9 |

1.674801 |

-1.232659 |

-2.881999 |

-1.077620 |

-1.378445 |

-0.135817 |

2.060139 |

1.189861 |

| 股票__10 |

0.607444 |

0.523483 |

0.764183 |

-0.733856 |

0.548573 |

0.273106 |

-0.264642 |

0.773705 |

# stock_df.index[3] ='hahha'

# stock_df

1.1.2 重设索引

# reset_index在原来基础上新增一列索引

# drop=False(默认) - 不丢弃原来索引

# drop=True - 丢掉原来索引 index

stock_df.reset_index()

|

level_0 |

2020-03-30 00:00:00 |

2020-03-31 00:00:00 |

2020-04-01 00:00:00 |

2020-04-02 00:00:00 |

2020-04-03 00:00:00 |

2020-04-04 00:00:00 |

2020-04-05 00:00:00 |

2020-04-06 00:00:00 |

| 0 |

股票__1 |

0.740580 |

0.786047 |

-0.152641 |

0.056805 |

0.093881 |

0.731375 |

-1.523384 |

1.711565 |

| 1 |

股票__2 |

0.422049 |

0.625417 |

-1.415830 |

-0.274347 |

0.985871 |

-0.557979 |

0.310265 |

-0.479645 |

| 2 |

股票__3 |

0.997411 |

-0.943973 |

-0.407830 |

-1.336312 |

-0.012484 |

1.187341 |

-0.254304 |

-0.742641 |

| 3 |

股票__4 |

0.341567 |

-0.406213 |

0.828614 |

0.127213 |

1.041014 |

0.790613 |

-0.603255 |

1.299546 |

| 4 |

股票__5 |

-1.232895 |

0.837897 |

1.192770 |

0.450929 |

-1.741813 |

-0.653622 |

-0.177525 |

1.876793 |

| 5 |

股票__6 |

-0.426871 |

1.140176 |

0.182610 |

-0.289479 |

0.824899 |

0.115661 |

-0.531914 |

-0.960658 |

| 6 |

股票__7 |

0.927928 |

0.260863 |

0.083166 |

-0.945330 |

-0.779561 |

0.230067 |

-0.819715 |

-1.367425 |

| 7 |

股票__8 |

0.822418 |

0.542014 |

-0.193316 |

0.505767 |

-0.425458 |

-0.242475 |

-0.035267 |

-0.022685 |

| 8 |

股票__9 |

1.674801 |

-1.232659 |

-2.881999 |

-1.077620 |

-1.378445 |

-0.135817 |

2.060139 |

1.189861 |

| 9 |

股票__10 |

0.607444 |

0.523483 |

0.764183 |

-0.733856 |

0.548573 |

0.273106 |

-0.264642 |

0.773705 |

stock_df.reset_index(drop=True)

|

2020-03-30 |

2020-03-31 |

2020-04-01 |

2020-04-02 |

2020-04-03 |

2020-04-04 |

2020-04-05 |

2020-04-06 |

| 0 |

0.740580 |

0.786047 |

-0.152641 |

0.056805 |

0.093881 |

0.731375 |

-1.523384 |

1.711565 |

| 1 |

0.422049 |

0.625417 |

-1.415830 |

-0.274347 |

0.985871 |

-0.557979 |

0.310265 |

-0.479645 |

| 2 |

0.997411 |

-0.943973 |

-0.407830 |

-1.336312 |

-0.012484 |

1.187341 |

-0.254304 |

-0.742641 |

| 3 |

0.341567 |

-0.406213 |

0.828614 |

0.127213 |

1.041014 |

0.790613 |

-0.603255 |

1.299546 |

| 4 |

-1.232895 |

0.837897 |

1.192770 |

0.450929 |

-1.741813 |

-0.653622 |

-0.177525 |

1.876793 |

| 5 |

-0.426871 |

1.140176 |

0.182610 |

-0.289479 |

0.824899 |

0.115661 |

-0.531914 |

-0.960658 |

| 6 |

0.927928 |

0.260863 |

0.083166 |

-0.945330 |

-0.779561 |

0.230067 |

-0.819715 |

-1.367425 |

| 7 |

0.822418 |

0.542014 |

-0.193316 |

0.505767 |

-0.425458 |

-0.242475 |

-0.035267 |

-0.022685 |

| 8 |

1.674801 |

-1.232659 |

-2.881999 |

-1.077620 |

-1.378445 |

-0.135817 |

2.060139 |

1.189861 |

| 9 |

0.607444 |

0.523483 |

0.764183 |

-0.733856 |

0.548573 |

0.273106 |

-0.264642 |

0.773705 |

1.1.3 以某列为索引

stock_df.set_index(keys='2020-03-30', drop=False) #此处因为类型问题,都是drop 原来的index

|

2020-03-30 |

2020-03-31 |

2020-04-01 |

2020-04-02 |

2020-04-03 |

2020-04-04 |

2020-04-05 |

2020-04-06 |

| 2020-03-30 |

|

|

|

|

|

|

|

|

| 0.740580 |

0.740580 |

0.786047 |

-0.152641 |

0.056805 |

0.093881 |

0.731375 |

-1.523384 |

1.711565 |

| 0.422049 |

0.422049 |

0.625417 |

-1.415830 |

-0.274347 |

0.985871 |

-0.557979 |

0.310265 |

-0.479645 |

| 0.997411 |

0.997411 |

-0.943973 |

-0.407830 |

-1.336312 |

-0.012484 |

1.187341 |

-0.254304 |

-0.742641 |

| 0.341567 |

0.341567 |

-0.406213 |

0.828614 |

0.127213 |

1.041014 |

0.790613 |

-0.603255 |

1.299546 |

| -1.232895 |

-1.232895 |

0.837897 |

1.192770 |

0.450929 |

-1.741813 |

-0.653622 |

-0.177525 |

1.876793 |

| -0.426871 |

-0.426871 |

1.140176 |

0.182610 |

-0.289479 |

0.824899 |

0.115661 |

-0.531914 |

-0.960658 |

| 0.927928 |

0.927928 |

0.260863 |

0.083166 |

-0.945330 |

-0.779561 |

0.230067 |

-0.819715 |

-1.367425 |

| 0.822418 |

0.822418 |

0.542014 |

-0.193316 |

0.505767 |

-0.425458 |

-0.242475 |

-0.035267 |

-0.022685 |

| 1.674801 |

1.674801 |

-1.232659 |

-2.881999 |

-1.077620 |

-1.378445 |

-0.135817 |

2.060139 |

1.189861 |

| 0.607444 |

0.607444 |

0.523483 |

0.764183 |

-0.733856 |

0.548573 |

0.273106 |

-0.264642 |

0.773705 |

# 字典方式创建DataFrame

df = pd.DataFrame({'month': [1, 4, 7, 10],

'year': [2012, 2014, 2013, 2014],

'sale':[55, 40, 84, 31]})

df

|

month |

year |

sale |

| 0 |

1 |

2012 |

55 |

| 1 |

4 |

2014 |

40 |

| 2 |

7 |

2013 |

84 |

| 3 |

10 |

2014 |

31 |

df.set_index(keys='month')

|

year |

sale |

| month |

|

|

| 1 |

2012 |

55 |

| 4 |

2014 |

40 |

| 7 |

2013 |

84 |

| 10 |

2014 |

31 |

# 设置2个index, 就是MultiIndex (三维数据结构)

# df.set_index(keys=['month', 'year'])

df.set_index(['month', 'year'])

|

|

sale |

| month |

year |

|

| 1 |

2012 |

55 |

| 4 |

2014 |

40 |

| 7 |

2013 |

84 |

| 10 |

2014 |

31 |

1.2 MultiIndex

df_m = df.set_index(['year', 'month'])

df_m

|

|

sale |

| year |

month |

|

| 2012 |

1 |

55 |

| 2014 |

4 |

40 |

| 2013 |

7 |

84 |

| 2014 |

10 |

31 |

# index属性

# - names: levers的名称

# - levels: 每个level的列表值

df_m.index

MultiIndex([(2012, 1),

(2014, 4),

(2013, 7),

(2014, 10)],

names=['year', 'month'])

df_m.index.names

FrozenList(['year', 'month'])

df_m.index.levels

FrozenList([[2012, 2013, 2014], [1, 4, 7, 10]])

1.3 Series

# 自动生成从0开始的行索引 index

# Data must be 1-dimensional

pd.Series(np.arange(10))

0 0

1 1

2 2

3 3

4 4

5 5

6 6

7 7

8 8

9 9

dtype: int32

# 手动指定index值

pd.Series([6.7,5.6,3,10,2], index=['a', 'b', 'c', 'd', 'e'])

a 6.7

b 5.6

c 3.0

d 10.0

e 2.0

dtype: float64

# 通过字典创建

se = pd.Series({'red':100, 'blue':200, 'green': 500, 'yellow':1000})

se

red 100

blue 200

green 500

yellow 1000

dtype: int64

# 取索引

se.index

Index(['red', 'blue', 'green', 'yellow'], dtype='object')

# 取array值

se.values

array([ 100, 200, 500, 1000], dtype=int64)

pd.Series(np.random.normal(0, 1, (10)))

0 -0.975747

1 0.021589

2 -0.384579

3 -0.412900

4 0.218133

5 -0.866525

6 -0.777209

7 -1.032130

8 0.202134

9 0.295274

dtype: float64

2.基本数据操作

2.1 索引操作

# 使用pd.read_csv()读取本地数据

data = pd.read_csv('./data/stock_day.csv')

data

|

open |

high |

close |

low |

volume |

price_change |

p_change |

ma5 |

ma10 |

ma20 |

v_ma5 |

v_ma10 |

v_ma20 |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

95578.03 |

0.63 |

2.68 |

22.942 |

22.142 |

22.875 |

53782.64 |

46738.65 |

55576.11 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

60985.11 |

0.69 |

3.02 |

22.406 |

21.955 |

22.942 |

40827.52 |

42736.34 |

56007.50 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

52914.01 |

0.54 |

2.42 |

21.938 |

21.929 |

23.022 |

35119.58 |

41871.97 |

56372.85 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

36105.01 |

0.36 |

1.64 |

21.446 |

21.909 |

23.137 |

35397.58 |

39904.78 |

60149.60 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

23331.04 |

0.44 |

2.05 |

21.366 |

21.923 |

23.253 |

33590.21 |

42935.74 |

61716.11 |

0.58 |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

| 2015-03-06 |

13.17 |

14.48 |

14.28 |

13.13 |

179831.72 |

1.12 |

8.51 |

13.112 |

13.112 |

13.112 |

115090.18 |

115090.18 |

115090.18 |

6.16 |

| 2015-03-05 |

12.88 |

13.45 |

13.16 |

12.87 |

93180.39 |

0.26 |

2.02 |

12.820 |

12.820 |

12.820 |

98904.79 |

98904.79 |

98904.79 |

3.19 |

| 2015-03-04 |

12.80 |

12.92 |

12.90 |

12.61 |

67075.44 |

0.20 |

1.57 |

12.707 |

12.707 |

12.707 |

100812.93 |

100812.93 |

100812.93 |

2.30 |

| 2015-03-03 |

12.52 |

13.06 |

12.70 |

12.52 |

139071.61 |

0.18 |

1.44 |

12.610 |

12.610 |

12.610 |

117681.67 |

117681.67 |

117681.67 |

4.76 |

| 2015-03-02 |

12.25 |

12.67 |

12.52 |

12.20 |

96291.73 |

0.32 |

2.62 |

12.520 |

12.520 |

12.520 |

96291.73 |

96291.73 |

96291.73 |

3.30 |

643 rows × 14 columns

# 去除一些列,简化数据

data = data.drop(["ma5","ma10","ma20","v_ma5","v_ma10","v_ma20"], axis=1) # axis=1 去除对应的列,与numpy相反

data

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

95578.03 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

60985.11 |

0.69 |

3.02 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

52914.01 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

36105.01 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

23331.04 |

0.44 |

2.05 |

0.58 |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

| 2015-03-06 |

13.17 |

14.48 |

14.28 |

13.13 |

179831.72 |

1.12 |

8.51 |

6.16 |

| 2015-03-05 |

12.88 |

13.45 |

13.16 |

12.87 |

93180.39 |

0.26 |

2.02 |

3.19 |

| 2015-03-04 |

12.80 |

12.92 |

12.90 |

12.61 |

67075.44 |

0.20 |

1.57 |

2.30 |

| 2015-03-03 |

12.52 |

13.06 |

12.70 |

12.52 |

139071.61 |

0.18 |

1.44 |

4.76 |

| 2015-03-02 |

12.25 |

12.67 |

12.52 |

12.20 |

96291.73 |

0.32 |

2.62 |

3.30 |

643 rows × 8 columns

2.1.1 直接使用行列索引

# 必须先列后行

data['high']['2018-02-27']

25.88

# data['2018-02-27']['high']

2.1.2 使用loc和iloc取索引

# loc取字符串, 先行后列

data.loc['2018-02-27']['high']

25.88

# 两种取值方式都可以

data.loc['2018-02-27','high']

25.88

data.loc['2018-02-27':'2018-02-22', 'open']

2018-02-27 23.53

2018-02-26 22.80

2018-02-23 22.88

2018-02-22 22.25

Name: open, dtype: float64

# data.loc['high']['2018-02-27']

# iloc取索引数字,先行后列

data.iloc[:3, 3:5]

|

low |

volume |

| 2018-02-27 |

23.53 |

95578.03 |

| 2018-02-26 |

22.80 |

60985.11 |

| 2018-02-23 |

22.71 |

52914.01 |

2.1.3 使用ix取混合索引

# ix可以去数字和字符串, 先行后列

# 现版本中已被取消

# data.ix[0:4, ['open', 'close', 'high', 'low']]

# 先通过data.index去除索引并切片

data.loc[data.index[0:4], ['open', 'close', 'high', 'low']]

|

open |

close |

high |

low |

| 2018-02-27 |

23.53 |

24.16 |

25.88 |

23.53 |

| 2018-02-26 |

22.80 |

23.53 |

23.78 |

22.80 |

| 2018-02-23 |

22.88 |

22.82 |

23.37 |

22.71 |

| 2018-02-22 |

22.25 |

22.28 |

22.76 |

22.02 |

data.index

Index(['2018-02-27', '2018-02-26', '2018-02-23', '2018-02-22', '2018-02-14',

'2018-02-13', '2018-02-12', '2018-02-09', '2018-02-08', '2018-02-07',

...

'2015-03-13', '2015-03-12', '2015-03-11', '2015-03-10', '2015-03-09',

'2015-03-06', '2015-03-05', '2015-03-04', '2015-03-03', '2015-03-02'],

dtype='object', length=643)

data.iloc[0:4, data.columns.get_indexer(['open', 'close', 'high', 'low'])]

|

open |

close |

high |

low |

| 2018-02-27 |

23.53 |

24.16 |

25.88 |

23.53 |

| 2018-02-26 |

22.80 |

23.53 |

23.78 |

22.80 |

| 2018-02-23 |

22.88 |

22.82 |

23.37 |

22.71 |

| 2018-02-22 |

22.25 |

22.28 |

22.76 |

22.02 |

data.columns.get_indexer(['close'])

array([2], dtype=int64)

data

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

95578.03 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

60985.11 |

0.69 |

3.02 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

52914.01 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

36105.01 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

23331.04 |

0.44 |

2.05 |

0.58 |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

| 2015-03-06 |

13.17 |

14.48 |

14.28 |

13.13 |

179831.72 |

1.12 |

8.51 |

6.16 |

| 2015-03-05 |

12.88 |

13.45 |

13.16 |

12.87 |

93180.39 |

0.26 |

2.02 |

3.19 |

| 2015-03-04 |

12.80 |

12.92 |

12.90 |

12.61 |

67075.44 |

0.20 |

1.57 |

2.30 |

| 2015-03-03 |

12.52 |

13.06 |

12.70 |

12.52 |

139071.61 |

0.18 |

1.44 |

4.76 |

| 2015-03-02 |

12.25 |

12.67 |

12.52 |

12.20 |

96291.73 |

0.32 |

2.62 |

3.30 |

643 rows × 8 columns

2.2 赋值操作

data

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

95578.03 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

60985.11 |

0.69 |

3.02 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

52914.01 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

36105.01 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

23331.04 |

0.44 |

2.05 |

0.58 |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

| 2015-03-06 |

13.17 |

14.48 |

14.28 |

13.13 |

179831.72 |

1.12 |

8.51 |

6.16 |

| 2015-03-05 |

12.88 |

13.45 |

13.16 |

12.87 |

93180.39 |

0.26 |

2.02 |

3.19 |

| 2015-03-04 |

12.80 |

12.92 |

12.90 |

12.61 |

67075.44 |

0.20 |

1.57 |

2.30 |

| 2015-03-03 |

12.52 |

13.06 |

12.70 |

12.52 |

139071.61 |

0.18 |

1.44 |

4.76 |

| 2015-03-02 |

12.25 |

12.67 |

12.52 |

12.20 |

96291.73 |

0.32 |

2.62 |

3.30 |

643 rows × 8 columns

# 赋值方式1, 直接取对应的属性值

data.volume = 100

data.head()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

100 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

100 |

0.69 |

3.02 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

100 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

100 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

100 |

0.44 |

2.05 |

0.58 |

# 赋值方式2, 类似于取切片

data['low'] = 100

data.head()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

100 |

100 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

100 |

100 |

0.69 |

3.02 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

100 |

100 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

100 |

100 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

100 |

100 |

0.44 |

2.05 |

0.58 |

# 直接取出Series

data.open.head()

2018-02-27 23.53

2018-02-26 22.80

2018-02-23 22.88

2018-02-22 22.25

2018-02-14 21.49

Name: open, dtype: float64

# 直接取出Series

data['open'].head()

2018-02-27 23.53

2018-02-26 22.80

2018-02-23 22.88

2018-02-22 22.25

2018-02-14 21.49

Name: open, dtype: float64

2.3 排序

data.head()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

100 |

100 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

100 |

100 |

0.69 |

3.02 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

100 |

100 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

100 |

100 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

100 |

100 |

0.44 |

2.05 |

0.58 |

2.3.1 以特征值排序

# by --> 传入特征值, 可以传一个或者多个,以列表形式,排前面的作为高优先级,默认升序

data.sort_values(by='open', ascending=False)

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2015-06-15 |

34.99 |

34.99 |

31.69 |

100 |

100 |

-3.52 |

-10.00 |

6.82 |

| 2015-06-12 |

34.69 |

35.98 |

35.21 |

100 |

100 |

0.82 |

2.38 |

5.47 |

| 2015-06-10 |

34.10 |

36.35 |

33.85 |

100 |

100 |

0.51 |

1.53 |

9.21 |

| 2017-11-01 |

33.85 |

34.34 |

33.83 |

100 |

100 |

-0.61 |

-1.77 |

5.81 |

| 2015-06-11 |

33.17 |

34.98 |

34.39 |

100 |

100 |

0.54 |

1.59 |

5.92 |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

| 2015-03-05 |

12.88 |

13.45 |

13.16 |

100 |

100 |

0.26 |

2.02 |

3.19 |

| 2015-03-04 |

12.80 |

12.92 |

12.90 |

100 |

100 |

0.20 |

1.57 |

2.30 |

| 2015-03-03 |

12.52 |

13.06 |

12.70 |

100 |

100 |

0.18 |

1.44 |

4.76 |

| 2015-09-02 |

12.30 |

14.11 |

12.36 |

100 |

100 |

-1.10 |

-8.17 |

2.40 |

| 2015-03-02 |

12.25 |

12.67 |

12.52 |

100 |

100 |

0.32 |

2.62 |

3.30 |

643 rows × 8 columns

data.sort_values(by=['open', 'high'], ascending=True)

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2015-03-02 |

12.25 |

12.67 |

12.52 |

100 |

100 |

0.32 |

2.62 |

3.30 |

| 2015-09-02 |

12.30 |

14.11 |

12.36 |

100 |

100 |

-1.10 |

-8.17 |

2.40 |

| 2015-03-03 |

12.52 |

13.06 |

12.70 |

100 |

100 |

0.18 |

1.44 |

4.76 |

| 2015-03-04 |

12.80 |

12.92 |

12.90 |

100 |

100 |

0.20 |

1.57 |

2.30 |

| 2015-03-05 |

12.88 |

13.45 |

13.16 |

100 |

100 |

0.26 |

2.02 |

3.19 |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

| 2015-06-11 |

33.17 |

34.98 |

34.39 |

100 |

100 |

0.54 |

1.59 |

5.92 |

| 2017-11-01 |

33.85 |

34.34 |

33.83 |

100 |

100 |

-0.61 |

-1.77 |

5.81 |

| 2015-06-10 |

34.10 |

36.35 |

33.85 |

100 |

100 |

0.51 |

1.53 |

9.21 |

| 2015-06-12 |

34.69 |

35.98 |

35.21 |

100 |

100 |

0.82 |

2.38 |

5.47 |

| 2015-06-15 |

34.99 |

34.99 |

31.69 |

100 |

100 |

-3.52 |

-10.00 |

6.82 |

643 rows × 8 columns

# Series 排序因为只有一个特征值,所以不需要传参

data.close.sort_values()

2015-09-02 12.36

2015-03-02 12.52

2015-03-03 12.70

2015-09-07 12.77

2015-03-04 12.90

...

2017-11-01 33.83

2015-06-10 33.85

2015-06-11 34.39

2017-10-31 34.44

2015-06-12 35.21

Name: close, Length: 643, dtype: float64

2.3.2 以索引排序

# DataFrame 使用sort_index 以索引排序

data.sort_index()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2015-03-02 |

12.25 |

12.67 |

12.52 |

100 |

100 |

0.32 |

2.62 |

3.30 |

| 2015-03-03 |

12.52 |

13.06 |

12.70 |

100 |

100 |

0.18 |

1.44 |

4.76 |

| 2015-03-04 |

12.80 |

12.92 |

12.90 |

100 |

100 |

0.20 |

1.57 |

2.30 |

| 2015-03-05 |

12.88 |

13.45 |

13.16 |

100 |

100 |

0.26 |

2.02 |

3.19 |

| 2015-03-06 |

13.17 |

14.48 |

14.28 |

100 |

100 |

1.12 |

8.51 |

6.16 |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

100 |

100 |

0.44 |

2.05 |

0.58 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

100 |

100 |

0.36 |

1.64 |

0.90 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

100 |

100 |

0.54 |

2.42 |

1.32 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

100 |

100 |

0.69 |

3.02 |

1.53 |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

100 |

100 |

0.63 |

2.68 |

2.39 |

643 rows × 8 columns

# Series 排序

data.high.sort_index()

2015-03-02 12.67

2015-03-03 13.06

2015-03-04 12.92

2015-03-05 13.45

2015-03-06 14.48

...

2018-02-14 21.99

2018-02-22 22.76

2018-02-23 23.37

2018-02-26 23.78

2018-02-27 25.88

Name: high, Length: 643, dtype: float64

3. DataFrame运算

3.1 算数运算

data.head()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

100 |

100 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

100 |

100 |

0.69 |

3.02 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

100 |

100 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

100 |

100 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

100 |

100 |

0.44 |

2.05 |

0.58 |

# 推荐使用pd.方法

data['close'].add(100).head()

2018-02-27 124.16

2018-02-26 123.53

2018-02-23 122.82

2018-02-22 122.28

2018-02-14 121.92

Name: close, dtype: float64

# 使用符号运算

(data.close + 100).head()

2018-02-27 124.16

2018-02-26 123.53

2018-02-23 122.82

2018-02-22 122.28

2018-02-14 121.92

Name: close, dtype: float64

data.close.sub(10).head()

2018-02-27 14.16

2018-02-26 13.53

2018-02-23 12.82

2018-02-22 12.28

2018-02-14 11.92

Name: close, dtype: float64

3.2 逻辑运算

3.2.1 逻辑运算符 ( <, > , |, &)

data.head()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

100 |

100 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

100 |

100 |

0.69 |

3.02 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

100 |

100 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

100 |

100 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

100 |

100 |

0.44 |

2.05 |

0.58 |

# data.open 返回数据 True, False

# data[data.open] 逻辑判断的结果作为筛选依据

data['open'] > 23

2018-02-27 True

2018-02-26 False

2018-02-23 False

2018-02-22 False

2018-02-14 False

...

2015-03-06 False

2015-03-05 False

2015-03-04 False

2015-03-03 False

2015-03-02 False

Name: open, Length: 643, dtype: bool

data[data.open>23].head()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

100 |

100 |

0.63 |

2.68 |

2.39 |

| 2018-02-01 |

23.71 |

23.86 |

22.42 |

100 |

100 |

-1.30 |

-5.48 |

1.66 |

| 2018-01-31 |

23.85 |

23.98 |

23.72 |

100 |

100 |

-0.11 |

-0.46 |

1.23 |

| 2018-01-30 |

23.71 |

24.08 |

23.83 |

100 |

100 |

0.05 |

0.21 |

0.81 |

| 2018-01-29 |

24.40 |

24.63 |

23.77 |

100 |

100 |

-0.73 |

-2.98 |

1.64 |

# 利用与或 (& |)完成逻辑判断

# 优先级问题,多加括号

data[(data.close>23) & (data.close<24)].head()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

100 |

100 |

0.69 |

3.02 |

1.53 |

| 2018-02-05 |

22.45 |

23.39 |

23.27 |

100 |

100 |

0.65 |

2.87 |

1.31 |

| 2018-01-31 |

23.85 |

23.98 |

23.72 |

100 |

100 |

-0.11 |

-0.46 |

1.23 |

| 2018-01-30 |

23.71 |

24.08 |

23.83 |

100 |

100 |

0.05 |

0.21 |

0.81 |

| 2018-01-29 |

24.40 |

24.63 |

23.77 |

100 |

100 |

-0.73 |

-2.98 |

1.64 |

3.2.2 逻辑运算函数

# query(str) 传入字符串

data.query('close>23 & close<24').head()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

100 |

100 |

0.69 |

3.02 |

1.53 |

| 2018-02-05 |

22.45 |

23.39 |

23.27 |

100 |

100 |

0.65 |

2.87 |

1.31 |

| 2018-01-31 |

23.85 |

23.98 |

23.72 |

100 |

100 |

-0.11 |

-0.46 |

1.23 |

| 2018-01-30 |

23.71 |

24.08 |

23.83 |

100 |

100 |

0.05 |

0.21 |

0.81 |

| 2018-01-29 |

24.40 |

24.63 |

23.77 |

100 |

100 |

-0.73 |

-2.98 |

1.64 |

# isin() 可以传一个值, 也可以传一个列表范围, 判断是否在某个范围内

data['open'].isin([22.80, 23.00])

2018-02-27 False

2018-02-26 True

2018-02-23 False

2018-02-22 False

2018-02-14 False

...

2015-03-06 False

2015-03-05 False

2015-03-04 False

2015-03-03 False

2015-03-02 False

Name: open, Length: 643, dtype: bool

data[data['open'].isin([22.80, 23.00])]

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-26 |

22.8 |

23.78 |

23.53 |

100 |

100 |

0.69 |

3.02 |

1.53 |

| 2018-02-06 |

22.8 |

23.55 |

22.29 |

100 |

100 |

-0.97 |

-4.17 |

1.39 |

| 2017-12-18 |

23.0 |

23.49 |

23.13 |

100 |

100 |

0.12 |

0.52 |

0.74 |

| 2017-07-24 |

22.8 |

23.79 |

23.03 |

100 |

100 |

-0.17 |

-0.73 |

2.59 |

| 2017-06-21 |

23.0 |

23.84 |

23.57 |

100 |

100 |

-0.51 |

-2.12 |

5.13 |

| 2016-01-04 |

22.8 |

22.84 |

20.69 |

100 |

100 |

-2.28 |

-9.93 |

1.60 |

3.3 统计运算

3.3.1 describe()

# describe()方法可以快速的查看DataFrame的整体属性

# 25% - 第一四分位数(Q1),样本中从小到大排列后第25%的数据

# 50% - 中位数

data.describe()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| count |

643.000000 |

643.000000 |

643.000000 |

643.0 |

643.0 |

643.000000 |

643.000000 |

643.000000 |

| mean |

21.272706 |

21.900513 |

21.336267 |

100.0 |

100.0 |

0.018802 |

0.190280 |

2.936190 |

| std |

3.930973 |

4.077578 |

3.942806 |

0.0 |

0.0 |

0.898476 |

4.079698 |

2.079375 |

| min |

12.250000 |

12.670000 |

12.360000 |

100.0 |

100.0 |

-3.520000 |

-10.030000 |

0.040000 |

| 25% |

19.000000 |

19.500000 |

19.045000 |

100.0 |

100.0 |

-0.390000 |

-1.850000 |

1.360000 |

| 50% |

21.440000 |

21.970000 |

21.450000 |

100.0 |

100.0 |

0.050000 |

0.260000 |

2.500000 |

| 75% |

23.400000 |

24.065000 |

23.415000 |

100.0 |

100.0 |

0.455000 |

2.305000 |

3.915000 |

| max |

34.990000 |

36.350000 |

35.210000 |

100.0 |

100.0 |

3.030000 |

10.030000 |

12.560000 |

3.3.2 统计函数

# max(), min()

data.max()

open 34.99

high 36.35

close 35.21

low 100.00

volume 100.00

price_change 3.03

p_change 10.03

turnover 12.56

dtype: float64

data.std()

# data.var()

open 3.930973

high 4.077578

close 3.942806

low 0.000000

volume 0.000000

price_change 0.898476

p_change 4.079698

turnover 2.079375

dtype: float64

data.median()

open 21.44

high 21.97

close 21.45

low 100.00

volume 100.00

price_change 0.05

p_change 0.26

turnover 2.50

dtype: float64

# idxmax ( index-max) 最大值的索引值

data.idxmax()

# data,idxmin()

open 2015-06-15

high 2015-06-10

close 2015-06-12

low 2018-02-27

volume 2018-02-27

price_change 2015-06-09

p_change 2015-08-28

turnover 2017-10-26

dtype: object

3.4 累计统计函数

# 常见累计统计函数为:

# cumsum - 累加

# cummax - 累计取最大值, 新的最大值替换原来的最大值

# cummin - 累计取最小值

# cumprod - 累积

data = data.sort_index()

data.p_change

2015-03-02 2.62

2015-03-03 1.44

2015-03-04 1.57

2015-03-05 2.02

2015-03-06 8.51

...

2018-02-14 2.05

2018-02-22 1.64

2018-02-23 2.42

2018-02-26 3.02

2018-02-27 2.68

Name: p_change, Length: 643, dtype: float64

data.p_change.cumsum()

2015-03-02 2.62

2015-03-03 4.06

2015-03-04 5.63

2015-03-05 7.65

2015-03-06 16.16

...

2018-02-14 112.59

2018-02-22 114.23

2018-02-23 116.65

2018-02-26 119.67

2018-02-27 122.35

Name: p_change, Length: 643, dtype: float64

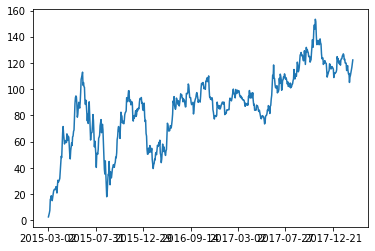

# 利用Pandas自带的绘图功能, 需要运行2次才能出结果

data.p_change.cumsum().plot()

<matplotlib.axes._subplots.AxesSubplot at 0x1d54ecb2848>

data.p_change.cummax().plot()

<matplotlib.axes._subplots.AxesSubplot at 0x1d54ff73a88>

3.5 自定义函数

# apply(func), fun - lambda函数

data[['open']] # [[]]取出DataFrame

|

open |

| 2015-03-02 |

12.25 |

| 2015-03-03 |

12.52 |

| 2015-03-04 |

12.80 |

| 2015-03-05 |

12.88 |

| 2015-03-06 |

13.17 |

| ... |

... |

| 2018-02-14 |

21.49 |

| 2018-02-22 |

22.25 |

| 2018-02-23 |

22.88 |

| 2018-02-26 |

22.80 |

| 2018-02-27 |

23.53 |

643 rows × 1 columns

data[['open']].apply(lambda x: x.max()-x.min()) # 默认axis=0

open 22.74

dtype: float64

4. Pandas内置画图

# DataFrame(x, y, kind='line')

# kind: 绘图的类型, line, bar, barh, hist, pie, scatter

# DataFrame

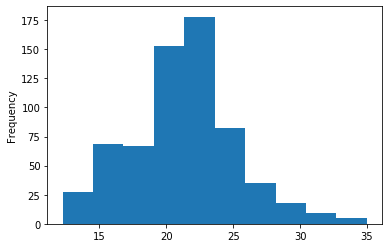

data['open'].plot(kind='hist')

<matplotlib.axes._subplots.AxesSubplot at 0x1d54ffe6c88>

5. 文件读取与存储

5.1 csv文件

# usecols -abs 读取特定列,列表形式传入

# sep=',' 分隔

# 读取文件

data = pd.read_csv('./data/stock_day.csv', usecols=['open', 'high', 'low'], sep=',')

data

|

open |

high |

low |

| 2018-02-27 |

23.53 |

25.88 |

23.53 |

| 2018-02-26 |

22.80 |

23.78 |

22.80 |

| 2018-02-23 |

22.88 |

23.37 |

22.71 |

| 2018-02-22 |

22.25 |

22.76 |

22.02 |

| 2018-02-14 |

21.49 |

21.99 |

21.48 |

| ... |

... |

... |

... |

| 2015-03-06 |

13.17 |

14.48 |

13.13 |

| 2015-03-05 |

12.88 |

13.45 |

12.87 |

| 2015-03-04 |

12.80 |

12.92 |

12.61 |

| 2015-03-03 |

12.52 |

13.06 |

12.52 |

| 2015-03-02 |

12.25 |

12.67 |

12.20 |

643 rows × 3 columns

# 存储文件

# columns :存储指定列,

# index:是否存储index

data[:10].to_csv('./data/test_write_in.csv',columns=['high', 'low'], index=False)

5.2 hdf文件

# hdf文件格式是官方推荐的格式,存储读取速度快

# 压缩方式读取速度快,节省空间

# 支持跨平台

day_eps = pd.read_hdf('./data/stock_data/day/day_close.h5')

# 需要安装tables模块才能显示

# hdf文件不能直接打开,需要导入后才能打开

day_eps

|

000001.SZ |

000002.SZ |

000004.SZ |

000005.SZ |

000006.SZ |

000007.SZ |

000008.SZ |

000009.SZ |

000010.SZ |

000011.SZ |

... |

001965.SZ |

603283.SH |

002920.SZ |

002921.SZ |

300684.SZ |

002922.SZ |

300735.SZ |

603329.SH |

603655.SH |

603080.SH |

| 0 |

16.30 |

17.71 |

4.58 |

2.88 |

14.60 |

2.62 |

4.96 |

4.66 |

5.37 |

6.02 |

... |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

| 1 |

17.02 |

19.20 |

4.65 |

3.02 |

15.97 |

2.65 |

4.95 |

4.70 |

5.37 |

6.27 |

... |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

| 2 |

17.02 |

17.28 |

4.56 |

3.06 |

14.37 |

2.63 |

4.82 |

4.47 |

5.37 |

5.96 |

... |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

| 3 |

16.18 |

16.97 |

4.49 |

2.95 |

13.10 |

2.73 |

4.89 |

4.33 |

5.37 |

5.77 |

... |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

| 4 |

16.95 |

17.19 |

4.55 |

2.99 |

13.18 |

2.77 |

4.97 |

4.42 |

5.37 |

5.92 |

... |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

| 2673 |

12.96 |

35.99 |

22.84 |

4.37 |

9.85 |

16.66 |

8.47 |

7.52 |

6.20 |

17.88 |

... |

12.99 |

23.42 |

47.99 |

32.40 |

22.45 |

28.79 |

23.18 |

24.45 |

14.98 |

26.06 |

| 2674 |

13.08 |

35.84 |

23.02 |

4.41 |

9.85 |

16.66 |

8.49 |

7.48 |

6.01 |

17.75 |

... |

12.83 |

25.76 |

45.14 |

35.64 |

24.70 |

31.67 |

25.50 |

26.90 |

16.48 |

28.67 |

| 2675 |

13.47 |

35.67 |

22.40 |

4.32 |

9.85 |

16.66 |

8.49 |

7.38 |

5.97 |

17.45 |

... |

12.20 |

28.34 |

43.21 |

39.20 |

27.17 |

34.84 |

28.05 |

29.59 |

18.13 |

31.54 |

| 2676 |

13.40 |

35.15 |

22.29 |

4.29 |

9.85 |

16.66 |

8.56 |

7.04 |

5.84 |

17.49 |

... |

12.11 |

31.17 |

43.76 |

40.88 |

29.89 |

34.84 |

29.64 |

32.55 |

19.94 |

34.69 |

| 2677 |

13.55 |

35.55 |

22.20 |

4.37 |

9.85 |

16.66 |

8.67 |

7.06 |

5.99 |

17.76 |

... |

11.91 |

34.29 |

41.71 |

39.10 |

32.88 |

34.84 |

27.92 |

31.82 |

21.93 |

38.16 |

2678 rows × 3562 columns

# 存储格式为 .h5

day_eps_test = day_eps.to_hdf('./data/day_eps_test.h5', key='day_eps')

pd.read_hdf('./data/day_eps_test.h5')

|

000001.SZ |

000002.SZ |

000004.SZ |

000005.SZ |

000006.SZ |

000007.SZ |

000008.SZ |

000009.SZ |

000010.SZ |

000011.SZ |

... |

001965.SZ |

603283.SH |

002920.SZ |

002921.SZ |

300684.SZ |

002922.SZ |

300735.SZ |

603329.SH |

603655.SH |

603080.SH |

| 0 |

16.30 |

17.71 |

4.58 |

2.88 |

14.60 |

2.62 |

4.96 |

4.66 |

5.37 |

6.02 |

... |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

| 1 |

17.02 |

19.20 |

4.65 |

3.02 |

15.97 |

2.65 |

4.95 |

4.70 |

5.37 |

6.27 |

... |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

| 2 |

17.02 |

17.28 |

4.56 |

3.06 |

14.37 |

2.63 |

4.82 |

4.47 |

5.37 |

5.96 |

... |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

| 3 |

16.18 |

16.97 |

4.49 |

2.95 |

13.10 |

2.73 |

4.89 |

4.33 |

5.37 |

5.77 |

... |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

| 4 |

16.95 |

17.19 |

4.55 |

2.99 |

13.18 |

2.77 |

4.97 |

4.42 |

5.37 |

5.92 |

... |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

| 2673 |

12.96 |

35.99 |

22.84 |

4.37 |

9.85 |

16.66 |

8.47 |

7.52 |

6.20 |

17.88 |

... |

12.99 |

23.42 |

47.99 |

32.40 |

22.45 |

28.79 |

23.18 |

24.45 |

14.98 |

26.06 |

| 2674 |

13.08 |

35.84 |

23.02 |

4.41 |

9.85 |

16.66 |

8.49 |

7.48 |

6.01 |

17.75 |

... |

12.83 |

25.76 |

45.14 |

35.64 |

24.70 |

31.67 |

25.50 |

26.90 |

16.48 |

28.67 |

| 2675 |

13.47 |

35.67 |

22.40 |

4.32 |

9.85 |

16.66 |

8.49 |

7.38 |

5.97 |

17.45 |

... |

12.20 |

28.34 |

43.21 |

39.20 |

27.17 |

34.84 |

28.05 |

29.59 |

18.13 |

31.54 |

| 2676 |

13.40 |

35.15 |

22.29 |

4.29 |

9.85 |

16.66 |

8.56 |

7.04 |

5.84 |

17.49 |

... |

12.11 |

31.17 |

43.76 |

40.88 |

29.89 |

34.84 |

29.64 |

32.55 |

19.94 |

34.69 |

| 2677 |

13.55 |

35.55 |

22.20 |

4.37 |

9.85 |

16.66 |

8.67 |

7.06 |

5.99 |

17.76 |

... |

11.91 |

34.29 |

41.71 |

39.10 |

32.88 |

34.84 |

27.92 |

31.82 |

21.93 |

38.16 |

2678 rows × 3562 columns

5.3 json文件

# oritent: 读取方式

# lines: 是否按行读取

json_read = pd.read_json("./data/Sarcasm_Headlines_Dataset.json", orient="records", lines=True)

json_read

|

article_link |

headline |

is_sarcastic |

| 0 |

https://www.huffingtonpost.com/entry/versace-b... |

former versace store clerk sues over secret 'b... |

0 |

| 1 |

https://www.huffingtonpost.com/entry/roseanne-... |

the 'roseanne' revival catches up to our thorn... |

0 |

| 2 |

https://local.theonion.com/mom-starting-to-fea... |

mom starting to fear son's web series closest ... |

1 |

| 3 |

https://politics.theonion.com/boehner-just-wan... |

boehner just wants wife to listen, not come up... |

1 |

| 4 |

https://www.huffingtonpost.com/entry/jk-rowlin... |

j.k. rowling wishes snape happy birthday in th... |

0 |

| ... |

... |

... |

... |

| 26704 |

https://www.huffingtonpost.com/entry/american-... |

american politics in moral free-fall |

0 |

| 26705 |

https://www.huffingtonpost.com/entry/americas-... |

america's best 20 hikes |

0 |

| 26706 |

https://www.huffingtonpost.com/entry/reparatio... |

reparations and obama |

0 |

| 26707 |

https://www.huffingtonpost.com/entry/israeli-b... |

israeli ban targeting boycott supporters raise... |

0 |

| 26708 |

https://www.huffingtonpost.com/entry/gourmet-g... |

gourmet gifts for the foodie 2014 |

0 |

26709 rows × 3 columns

# lines 表示存储数据分行, 否则全部为一整行

json_read.to_json('./data/test.json', orient='records', lines=True)

6.高级处理

6.1 处理缺失值

# 缺失值一般使用nan(not a number)来表示

type(np.nan)

float

# 导入数据

movie = pd.read_csv('./data/IMDB-Movie-Data.csv')

movie.head()

|

Rank |

Title |

Genre |

Description |

Director |

Actors |

Year |

Runtime (Minutes) |

Rating |

Votes |

Revenue (Millions) |

Metascore |

| 0 |

1 |

Guardians of the Galaxy |

Action,Adventure,Sci-Fi |

A group of intergalactic criminals are forced ... |

James Gunn |

Chris Pratt, Vin Diesel, Bradley Cooper, Zoe S... |

2014 |

121 |

8.1 |

757074 |

333.13 |

76.0 |

| 1 |

2 |

Prometheus |

Adventure,Mystery,Sci-Fi |

Following clues to the origin of mankind, a te... |

Ridley Scott |

Noomi Rapace, Logan Marshall-Green, Michael Fa... |

2012 |

124 |

7.0 |

485820 |

126.46 |

65.0 |

| 2 |

3 |

Split |

Horror,Thriller |

Three girls are kidnapped by a man with a diag... |

M. Night Shyamalan |

James McAvoy, Anya Taylor-Joy, Haley Lu Richar... |

2016 |

117 |

7.3 |

157606 |

138.12 |

62.0 |

| 3 |

4 |

Sing |

Animation,Comedy,Family |

In a city of humanoid animals, a hustling thea... |

Christophe Lourdelet |

Matthew McConaughey,Reese Witherspoon, Seth Ma... |

2016 |

108 |

7.2 |

60545 |

270.32 |

59.0 |

| 4 |

5 |

Suicide Squad |

Action,Adventure,Fantasy |

A secret government agency recruits some of th... |

David Ayer |

Will Smith, Jared Leto, Margot Robbie, Viola D... |

2016 |

123 |

6.2 |

393727 |

325.02 |

40.0 |

# 判断缺失值是否存在

# isnull() :nan - True

# notnull():nan - False

pd.isnull(movie)

|

Rank |

Title |

Genre |

Description |

Director |

Actors |

Year |

Runtime (Minutes) |

Rating |

Votes |

Revenue (Millions) |

Metascore |

| 0 |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

| 1 |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

| 2 |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

| 3 |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

| 4 |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

| 995 |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

True |

False |

| 996 |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

| 997 |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

| 998 |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

True |

False |

| 999 |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

False |

1000 rows × 12 columns

np.any(pd.isnull(movie)) # 其中有任何一个为True(nan值存在), 则返回True

True

np.all(pd.notnull(movie)) # 所有的元素都非nan

False

6.1.1 丢弃缺失值

# 直接丢弃含有nan的一行数据

data = movie.dropna()

np.any(pd.isnull(data))

False

6.1.2 替换缺失值 (常见:平均值或者0)

# 使用平均值替换

# inplace=True , 表示直接对原来movie值进行修改

data = movie['Revenue (Millions)'].fillna(movie['Revenue (Millions)'].mean())

# inplace默认为False, 返回了新的替换后的一个data数据, 原来的movie中仍含有nan

np.any(pd.isnull(movie['Revenue (Millions)']))

True

movie['Revenue (Millions)'].fillna(movie['Revenue (Millions)'].mean(), inplace=True)

# movie['Revenue (Millions)'] 中的nan 已经被替换

np.any(pd.isnull(movie['Revenue (Millions)']))

False

6.1.3 缺失值不是nan

# 全局取消证书验证

# 读取数据

import ssl

ssl._create_default_https_context = ssl._create_unverified_context

wis = pd.read_csv("https://archive.ics.uci.edu/ml/machine-learning-databases/breast-cancer-wisconsin/breast-cancer-wisconsin.data")

# 先将? 数据替换成nan

# 再对nan进行处理

wis

|

1000025 |

5 |

1 |

1.1 |

1.2 |

2 |

1.3 |

3 |

1.4 |

1.5 |

2.1 |

| 0 |

1002945 |

5 |

4 |

4 |

5 |

7 |

10 |

3 |

2 |

1 |

2 |

| 1 |

1015425 |

3 |

1 |

1 |

1 |

2 |

2 |

3 |

1 |

1 |

2 |

| 2 |

1016277 |

6 |

8 |

8 |

1 |

3 |

4 |

3 |

7 |

1 |

2 |

| 3 |

1017023 |

4 |

1 |

1 |

3 |

2 |

1 |

3 |

1 |

1 |

2 |

| 4 |

1017122 |

8 |

10 |

10 |

8 |

7 |

10 |

9 |

7 |

1 |

4 |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

| 693 |

776715 |

3 |

1 |

1 |

1 |

3 |

2 |

1 |

1 |

1 |

2 |

| 694 |

841769 |

2 |

1 |

1 |

1 |

2 |

1 |

1 |

1 |

1 |

2 |

| 695 |

888820 |

5 |

10 |

10 |

3 |

7 |

3 |

8 |

10 |

2 |

4 |

| 696 |

897471 |

4 |

8 |

6 |

4 |

3 |

4 |

10 |

6 |

1 |

4 |

| 697 |

897471 |

4 |

8 |

8 |

5 |

4 |

5 |

10 |

4 |

1 |

4 |

698 rows × 11 columns

# to_replace: 被替换的值, value:去替换的值

wis = wis.replace(to_replace='?', value=np.nan)

wis = wis.dropna()

wis

|

1000025 |

5 |

1 |

1.1 |

1.2 |

2 |

1.3 |

3 |

1.4 |

1.5 |

2.1 |

| 0 |

1002945 |

5 |

4 |

4 |

5 |

7 |

10 |

3 |

2 |

1 |

2 |

| 1 |

1015425 |

3 |

1 |

1 |

1 |

2 |

2 |

3 |

1 |

1 |

2 |

| 2 |

1016277 |

6 |

8 |

8 |

1 |

3 |

4 |

3 |

7 |

1 |

2 |

| 3 |

1017023 |

4 |

1 |

1 |

3 |

2 |

1 |

3 |

1 |

1 |

2 |

| 4 |

1017122 |

8 |

10 |

10 |

8 |

7 |

10 |

9 |

7 |

1 |

4 |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

| 693 |

776715 |

3 |

1 |

1 |

1 |

3 |

2 |

1 |

1 |

1 |

2 |

| 694 |

841769 |

2 |

1 |

1 |

1 |

2 |

1 |

1 |

1 |

1 |

2 |

| 695 |

888820 |

5 |

10 |

10 |

3 |

7 |

3 |

8 |

10 |

2 |

4 |

| 696 |

897471 |

4 |

8 |

6 |

4 |

3 |

4 |

10 |

6 |

1 |

4 |

| 697 |

897471 |

4 |

8 |

8 |

5 |

4 |

5 |

10 |

4 |

1 |

4 |

682 rows × 11 columns

6.2 数据离散化

# 数据离散化可以简化数据结构,将数据划分到若干离散的区间,可以简化数据结构, 常用于搭配one-hot编码

# 获取数据

data = pd.read_csv("./data/stock_day.csv")

data_p= data['p_change']

data_p

2018-02-27 2.68

2018-02-26 3.02

2018-02-23 2.42

2018-02-22 1.64

2018-02-14 2.05

...

2015-03-06 8.51

2015-03-05 2.02

2015-03-04 1.57

2015-03-03 1.44

2015-03-02 2.62

Name: p_change, Length: 643, dtype: float64

# pd.qcut() 智能分组

# q: 分组数量

q_cut = pd.qcut(data_p, q=10)

q_cut

2018-02-27 (1.738, 2.938]

2018-02-26 (2.938, 5.27]

2018-02-23 (1.738, 2.938]

2018-02-22 (0.94, 1.738]

2018-02-14 (1.738, 2.938]

...

2015-03-06 (5.27, 10.03]

2015-03-05 (1.738, 2.938]

2015-03-04 (0.94, 1.738]

2015-03-03 (0.94, 1.738]

2015-03-02 (1.738, 2.938]

Name: p_change, Length: 643, dtype: category

Categories (10, interval[float64]): [(-10.030999999999999, -4.836] < (-4.836, -2.444] < (-2.444, -1.352] < (-1.352, -0.462] ... (0.94, 1.738] < (1.738, 2.938] < (2.938, 5.27] < (5.27, 10.03]]

# value_counts(): 每个分组区间内的数据数量

q_cut.value_counts()

(5.27, 10.03] 65

(0.26, 0.94] 65

(-0.462, 0.26] 65

(-10.030999999999999, -4.836] 65

(2.938, 5.27] 64

(1.738, 2.938] 64

(-1.352, -0.462] 64

(-2.444, -1.352] 64

(-4.836, -2.444] 64

(0.94, 1.738] 63

Name: p_change, dtype: int64

# pd.cut(data, bins): 自己指定分组区间

bins = [-100, -7, -5, -3, 0, 3, 5, 7, 100]

cut = pd.cut(data_p, bins=bins)

cut

2018-02-27 (0, 3]

2018-02-26 (3, 5]

2018-02-23 (0, 3]

2018-02-22 (0, 3]

2018-02-14 (0, 3]

...

2015-03-06 (7, 100]

2015-03-05 (0, 3]

2015-03-04 (0, 3]

2015-03-03 (0, 3]

2015-03-02 (0, 3]

Name: p_change, Length: 643, dtype: category

Categories (8, interval[int64]): [(-100, -7] < (-7, -5] < (-5, -3] < (-3, 0] < (0, 3] < (3, 5] < (5, 7] < (7, 100]]

cut.value_counts()

(0, 3] 215

(-3, 0] 188

(3, 5] 57

(-5, -3] 51

(7, 100] 35

(5, 7] 35

(-100, -7] 34

(-7, -5] 28

Name: p_change, dtype: int64

# get_dummies() 取独热矩阵

pd.get_dummies(q_cut)

|

(-10.030999999999999, -4.836] |

(-4.836, -2.444] |

(-2.444, -1.352] |

(-1.352, -0.462] |

(-0.462, 0.26] |

(0.26, 0.94] |

(0.94, 1.738] |

(1.738, 2.938] |

(2.938, 5.27] |

(5.27, 10.03] |

| 2018-02-27 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

1 |

0 |

0 |

| 2018-02-26 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

1 |

0 |

| 2018-02-23 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

1 |

0 |

0 |

| 2018-02-22 |

0 |

0 |

0 |

0 |

0 |

0 |

1 |

0 |

0 |

0 |

| 2018-02-14 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

1 |

0 |

0 |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

| 2015-03-06 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

1 |

| 2015-03-05 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

1 |

0 |

0 |

| 2015-03-04 |

0 |

0 |

0 |

0 |

0 |

0 |

1 |

0 |

0 |

0 |

| 2015-03-03 |

0 |

0 |

0 |

0 |

0 |

0 |

1 |

0 |

0 |

0 |

| 2015-03-02 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

1 |

0 |

0 |

643 rows × 10 columns

data_dummy = pd.get_dummies(q_cut)

6.3 数据拼接

6.3.1 pd.concat()

# 不指定axis 可能会造成拼接错位,产生很多nan

pd.concat([data, data_dummy], axis=1)

|

open |

high |

close |

low |

volume |

price_change |

p_change |

ma5 |

ma10 |

ma20 |

... |

(-10.030999999999999, -4.836] |

(-4.836, -2.444] |

(-2.444, -1.352] |

(-1.352, -0.462] |

(-0.462, 0.26] |

(0.26, 0.94] |

(0.94, 1.738] |

(1.738, 2.938] |

(2.938, 5.27] |

(5.27, 10.03] |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

95578.03 |

0.63 |

2.68 |

22.942 |

22.142 |

22.875 |

... |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

1 |

0 |

0 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

60985.11 |

0.69 |

3.02 |

22.406 |

21.955 |

22.942 |

... |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

1 |

0 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

52914.01 |

0.54 |

2.42 |