金融数据指标(历史移动波动率,均值)

1.导入函数

import numpy as np import pandas as pd import matplotlib.pyplot as plt import tushare as ts import math

2. 数据获取

data = ts.get_hist_data('000012',start='2015-06-23',end='2017-11-16')

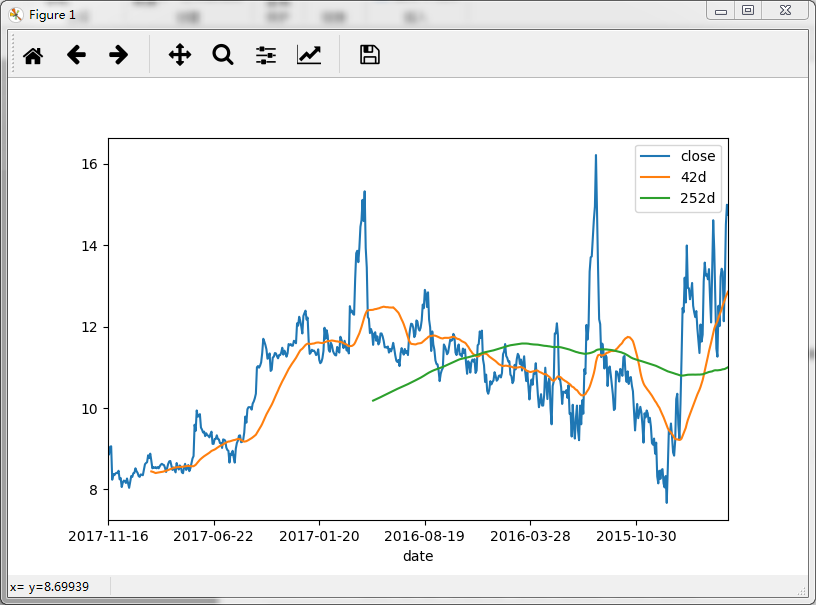

3.移动平均值

# 滚动窗口的使用

data['42d']= pd.rolling_mean(data['close'],window=42)

data['252d'] =pd.rolling_mean(data['close'],window=252)

print(data[['close','42d','252d']].tail())

data[['close','42d','252d']].plot(figsize=(8,5))

plt.show()

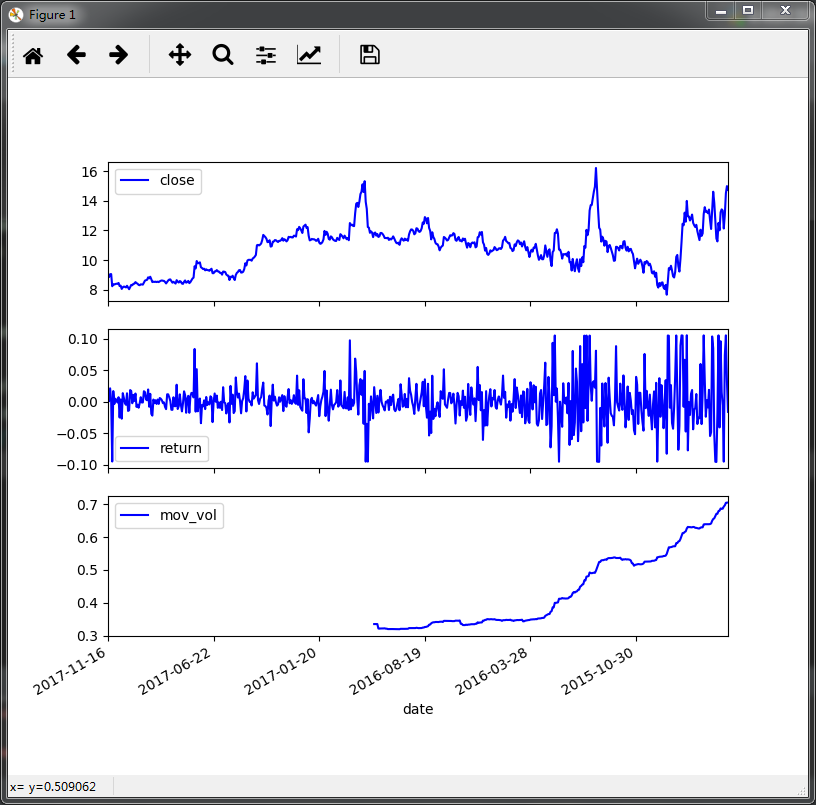

4.移动历史波动

data['return']=np.log(data['close']/data['close'].shift(1)) data['mov_vol'] = pd.rolling_std(data['return'],window=252)*math.sqrt(252) data[['close','return','mov_vol']].plot(subplots=True,style='b',figsize=(8,7)) plt.show()

浙公网安备 33010602011771号

浙公网安备 33010602011771号