python信用卡欺诈检测

信用卡欺诈检测

任务流程:

1、加载数据,观察问题

2、针对问题给出解决方案

3、数据集切分

4、评估方法对比

5、逻辑回归模型

6、建模结果分析

7、方案效果对比

读取数据

import pandas as pd

import matplotlib.pyplot as plt

import numpy as np

%matplotlib inline

data = pd.read_csv("E:\python学习\回归\信用卡欺诈检测\creditcard.csv")

data.head()

| Time | V1 | V2 | V3 | V4 | V5 | V6 | V7 | V8 | V9 | ... | V21 | V22 | V23 | V24 | V25 | V26 | V27 | V28 | Amount | Class | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.0 | -1.359807 | -0.072781 | 2.536347 | 1.378155 | -0.338321 | 0.462388 | 0.239599 | 0.098698 | 0.363787 | ... | -0.018307 | 0.277838 | -0.110474 | 0.066928 | 0.128539 | -0.189115 | 0.133558 | -0.021053 | 149.62 | 0 |

| 1 | 0.0 | 1.191857 | 0.266151 | 0.166480 | 0.448154 | 0.060018 | -0.082361 | -0.078803 | 0.085102 | -0.255425 | ... | -0.225775 | -0.638672 | 0.101288 | -0.339846 | 0.167170 | 0.125895 | -0.008983 | 0.014724 | 2.69 | 0 |

| 2 | 1.0 | -1.358354 | -1.340163 | 1.773209 | 0.379780 | -0.503198 | 1.800499 | 0.791461 | 0.247676 | -1.514654 | ... | 0.247998 | 0.771679 | 0.909412 | -0.689281 | -0.327642 | -0.139097 | -0.055353 | -0.059752 | 378.66 | 0 |

| 3 | 1.0 | -0.966272 | -0.185226 | 1.792993 | -0.863291 | -0.010309 | 1.247203 | 0.237609 | 0.377436 | -1.387024 | ... | -0.108300 | 0.005274 | -0.190321 | -1.175575 | 0.647376 | -0.221929 | 0.062723 | 0.061458 | 123.50 | 0 |

| 4 | 2.0 | -1.158233 | 0.877737 | 1.548718 | 0.403034 | -0.407193 | 0.095921 | 0.592941 | -0.270533 | 0.817739 | ... | -0.009431 | 0.798278 | -0.137458 | 0.141267 | -0.206010 | 0.502292 | 0.219422 | 0.215153 | 69.99 | 0 |

5 rows × 31 columns

通过观察数据,发现第一列 time没有真实意义,其他V列的值比较匀称,但是Amount列值的波动比较大,我们希望的数据特征是数据波动比较稳定的。

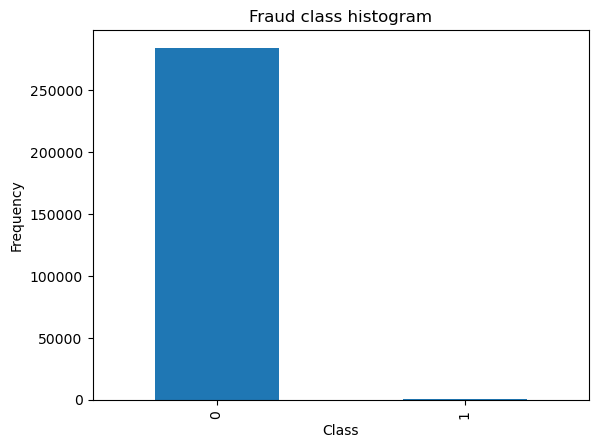

##数据标签分布

count_classes = pd.value_counts(data['Class'],sort=True).sort_index()

print(count_classes)

# pandas画条形图

count_classes.plot(kind = 'bar')

plt.title("Fraud class histogram")

plt.xlabel("Class")

plt.ylabel("Frequency")

0 284315

1 492

Name: Class, dtype: int64

Text(0, 0.5, 'Frequency')

由于我们发现提供的数据集本身就很不规则,我们考虑对数据做进一步处理,主要2种思路:下采样和过采样。

# 引入sklearn 标准化处理模块

from sklearn.preprocessing import StandardScaler

data['normAmount'] = StandardScaler().fit_transform(data['Amount'].values.reshape(-1,1))

data = data.drop(['Time','Amount'],axis = 1)

data.head()

| V1 | V2 | V3 | V4 | V5 | V6 | V7 | V8 | V9 | V10 | ... | V21 | V22 | V23 | V24 | V25 | V26 | V27 | V28 | Class | normAmount | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | -1.359807 | -0.072781 | 2.536347 | 1.378155 | -0.338321 | 0.462388 | 0.239599 | 0.098698 | 0.363787 | 0.090794 | ... | -0.018307 | 0.277838 | -0.110474 | 0.066928 | 0.128539 | -0.189115 | 0.133558 | -0.021053 | 0 | 0.244964 |

| 1 | 1.191857 | 0.266151 | 0.166480 | 0.448154 | 0.060018 | -0.082361 | -0.078803 | 0.085102 | -0.255425 | -0.166974 | ... | -0.225775 | -0.638672 | 0.101288 | -0.339846 | 0.167170 | 0.125895 | -0.008983 | 0.014724 | 0 | -0.342475 |

| 2 | -1.358354 | -1.340163 | 1.773209 | 0.379780 | -0.503198 | 1.800499 | 0.791461 | 0.247676 | -1.514654 | 0.207643 | ... | 0.247998 | 0.771679 | 0.909412 | -0.689281 | -0.327642 | -0.139097 | -0.055353 | -0.059752 | 0 | 1.160686 |

| 3 | -0.966272 | -0.185226 | 1.792993 | -0.863291 | -0.010309 | 1.247203 | 0.237609 | 0.377436 | -1.387024 | -0.054952 | ... | -0.108300 | 0.005274 | -0.190321 | -1.175575 | 0.647376 | -0.221929 | 0.062723 | 0.061458 | 0 | 0.140534 |

| 4 | -1.158233 | 0.877737 | 1.548718 | 0.403034 | -0.407193 | 0.095921 | 0.592941 | -0.270533 | 0.817739 | 0.753074 | ... | -0.009431 | 0.798278 | -0.137458 | 0.141267 | -0.206010 | 0.502292 | 0.219422 | 0.215153 | 0 | -0.073403 |

5 rows × 30 columns

第一种方式:采用下采样

X = data.iloc[:,data.columns != 'Class']

y = data.iloc[:,data.columns == 'Class']

number_records_fraud = len(data[data.Class==1]) ## class 为1 是异常值

fraud_indices = np.array(data[data.Class==1].index) ## 异常值数据的索引

normal_indices = data[data.Class==0].index ## 正常值数据的索引个数

# 对正常样本随即采用指定长度

random_normal_indices = np.random.choice(normal_indices,number_records_fraud,replace=False)

random_normal_indices = np.array(random_normal_indices)

# 合并新的索引项

under_sample_indices = np.concatenate([fraud_indices,random_normal_indices])

# 根据索引得到下采样的所有的样本点

under_sample_data = data.iloc[under_sample_indices,:]

X_undersample = under_sample_data.iloc[:,under_sample_data.columns!='Class']

y_undersample = under_sample_data.iloc[:,under_sample_data.columns=='Class']

#打印比例

print("正常样本比例:",len(under_sample_data[under_sample_data.Class==0])/len(under_sample_data))

print("异常样本比例:",len(under_sample_data[under_sample_data.Class==1])/len(under_sample_data))

print("下采样的总样本:",len(under_sample_data))

正常样本比例: 0.5

异常样本比例: 0.5

下采样的总样本: 984

数据集划分 这里我们需要注意的是,数据集划分成 训练集 和 测试集

from sklearn.model_selection import train_test_split

X_train,X_test,y_train,y_test = train_test_split(X,y,test_size=0.3,random_state=0)

print("原始训练集包含样本:",len(X_train))

print("原始测试集包含样本数量:",len(X_test))

print("原始样本总数:",len(X_train)+len(X_test))

# 对下采样的数据集进行划分

X_train_undersample,X_test_undersample,y_train_undersample,y_test_undersample = train_test_split(X_undersample,y_undersample,test_size=0.3,random_state=0)

print("下采样训练集包含样本:",len(X_train_undersample))

print("下采样测试集包含样本数量:",len(X_test_undersample))

print("下采样总数:",len(X_train_undersample)+len(X_test_undersample))

原始训练集包含样本: 199364

原始测试集包含样本数量: 85443

原始样本总数: 284807

下采样训练集包含样本: 688

下采样测试集包含样本数量: 296

下采样总数: 984

### 选择模型评估方法

准确率:分类问题中做对的占总体的百分比

召回率:正例中有多少能够预测,覆盖面的大小,比如我们看异常次数,那么假设总共异常值 10次,我们预测到是异常的是 6次, 那么召回率就是 0.6

精确度,被分为正例中实际为正例的比例

## Recall = TP / (TP + FN)

from sklearn.model_selection import KFold,cross_val_score,cross_val_predict

from sklearn.linear_model import LogisticRegression

from sklearn.metrics import recall_score,confusion_matrix

def printing_Kfold_scores(x_train_data,y_train_data):

fold = KFold(n_splits=5,shuffle=False)

c_param_range = [0.01,0.1,1,10,100] # 定义不同力度的正则化惩罚力度

## 展示结果用的表格

result_table = pd.DataFrame(index = range(len(c_param_range),2),columns=['C_parameter','Mean recall score'])

result_table['C_parameter'] = c_param_range

# k - fold 表示 K折交叉验证,这会得到2个索引集, 训练集 indices[0] 验证集 indices[1]

j = 0

## 循环遍历不同的惩罚力度

for c_param in c_param_range:

print('----------------------')

print('正则化惩罚力度' , c_param)

print('----------------------')

print('')

recall_accs = []

## 一步步分解来做交叉验证 把训练集数据 重新分成 新的训练集和验证集

for iteration,indices in enumerate(fold.split(x_train_data),start=1):

## 指定算法模型,并给定参数

Ir = LogisticRegression(C = c_param, penalty='l2')

## 训练模型,注意训练的时候,一定传入的训练集,所以 x 和 y 的索引都是 0

Ir.fit(x_train_data.iloc[indices[0],:],y_train_data.iloc[indices[0],:].values.ravel())

## 进行模型预测,这时候用的是 验证集 索引 为 1

y_pred_undersample = Ir.predict(x_train_data.iloc[indices[1],:].values)

## 有了预测结果之后,就可以进行模型评估,这里 recall_score 需要传入 预测值和真实值

recall_acc = recall_score(y_train_data.iloc[indices[1],:].values,y_pred_undersample)

recall_accs.append(recall_acc)

print('Iteration',iteration,':召回率 = ',recall_accs[-1])

## 当执行完所有的交叉验证后,计算平均结果

result_table.loc[j,'Mean recall score'] = np.mean(recall_accs)

j += 1

print()

print("平均召回率:",np.mean(recall_accs))

print()

best_c = result_table.iloc[result_table['Mean recall score'].astype('float32').idxmax()]['C_parameter']

print(">>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>")

print('效果最好的模型选择的参数=',best_c)

print(">>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>")

return best_c

## 交叉验证与不同参数的结果

best_c = printing_Kfold_scores(X_train_undersample,y_train_undersample)

----------------------

正则化惩罚力度 0.01

----------------------

Iteration 1 :召回率 = 0.821917808219178

Iteration 2 :召回率 = 0.8493150684931506

Iteration 3 :召回率 = 0.8983050847457628

Iteration 4 :召回率 = 0.9324324324324325

Iteration 5 :召回率 = 0.8787878787878788

平均召回率: 0.8761516545356806

----------------------

正则化惩罚力度 0.1

----------------------

Iteration 1 :召回率 = 0.863013698630137

Iteration 2 :召回率 = 0.863013698630137

Iteration 3 :召回率 = 0.9661016949152542

Iteration 4 :召回率 = 0.9459459459459459

Iteration 5 :召回率 = 0.8939393939393939

平均召回率: 0.9064028864121736

----------------------

正则化惩罚力度 1

----------------------

Iteration 1 :召回率 = 0.863013698630137

Iteration 2 :召回率 = 0.8767123287671232

Iteration 3 :召回率 = 0.9830508474576272

Iteration 4 :召回率 = 0.9324324324324325

Iteration 5 :召回率 = 0.9242424242424242

平均召回率: 0.9158903463059488

----------------------

正则化惩罚力度 10

----------------------

Iteration 1 :召回率 = 0.863013698630137

Iteration 2 :召回率 = 0.8767123287671232

Iteration 3 :召回率 = 0.9830508474576272

Iteration 4 :召回率 = 0.9459459459459459

Iteration 5 :召回率 = 0.9393939393939394

平均召回率: 0.9216233520389545

----------------------

正则化惩罚力度 100

----------------------

Iteration 1 :召回率 = 0.863013698630137

Iteration 2 :召回率 = 0.8767123287671232

Iteration 3 :召回率 = 0.9830508474576272

Iteration 4 :召回率 = 0.9459459459459459

Iteration 5 :召回率 = 0.9393939393939394

平均召回率: 0.9216233520389545

>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>

效果最好的模型选择的参数= 10.0

>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>

混淆矩阵

from sklearn.metrics import confusion_matrix

from itertools import product as product

def plot_confusion_matrix(cm,classes,title='Confusion matrix',cmap=plt.cm.Blues):

plt.imshow(cm,interpolation='nearest',cmap=cmap)

plt.title(title)

plt.colorbar()

tick_marks = np.arange(len(classes))

plt.xticks(tick_marks,classes,rotation=0)

plt.yticks(tick_marks,classes)

thresh = cm.max() / 2.

for i, j in product(range(cm.shape[0]),range(cm.shape[1])):

plt.text(j,i,cm[i,j],

horizontalalignment="center",

color="white" if cm[i,j] > thresh else "black")

plt.tight_layout()

plt.ylabel("True label")

plt.xlabel("Predicted label")

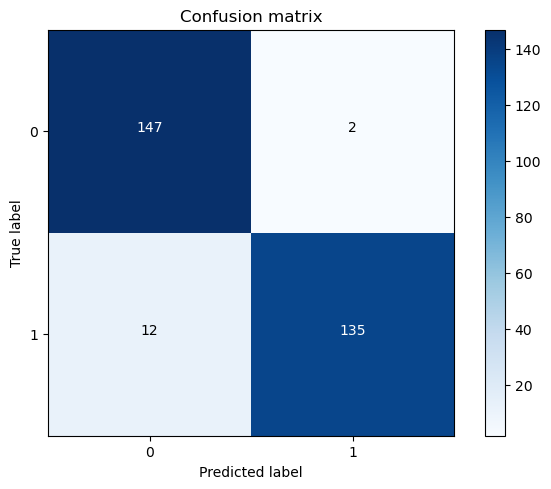

下采样模型 应用于下采样数据

Ir = LogisticRegression(C=best_c,penalty='l2')

Ir.fit(X_train_undersample,y_train_undersample.values.ravel())

y_pred_undersample = Ir.predict(X_test_undersample.values)

cnf_matrix = confusion_matrix(y_test_undersample,y_pred_undersample)

np.set_printoptions(precision=2)

print("模型应用于下采样的召回率:",cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

class_names = [0,1]

plt.figure()

plot_confusion_matrix(cnf_matrix,

classes=class_names,

title='Confusion matrix')

plt.show()

模型应用于下采样的召回率: 0.9183673469387755

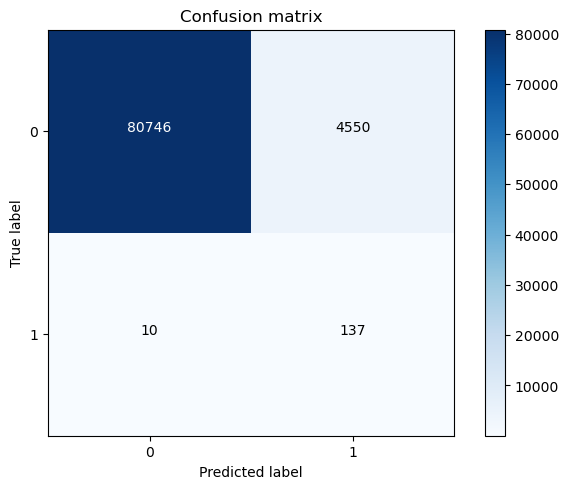

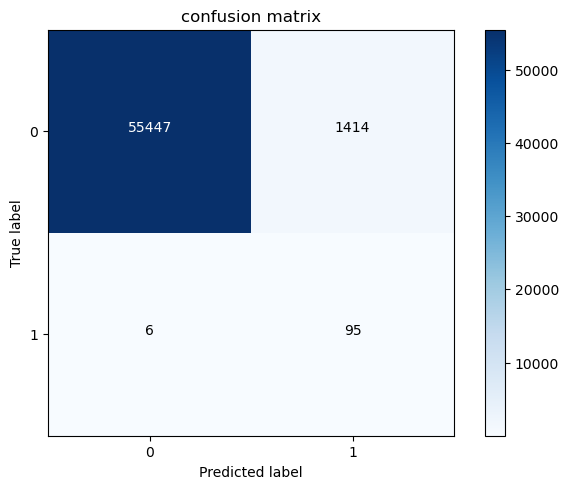

下采样模型应用于原始数据

Ir = LogisticRegression(C=best_c,penalty='l2')

Ir.fit(X_train_undersample,y_train_undersample.values.ravel())

y_pred = Ir.predict(X_test.values)

cnf_matrix = confusion_matrix(y_test,y_pred)

np.set_printoptions(precision=2)

print("下采样模型应用于原始数据的召回率:",cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

class_names = [0,1]

plt.figure()

plot_confusion_matrix(cnf_matrix,

classes=class_names,

title='Confusion matrix')

plt.show()

下采样模型应用于原始数据的召回率: 0.9319727891156463

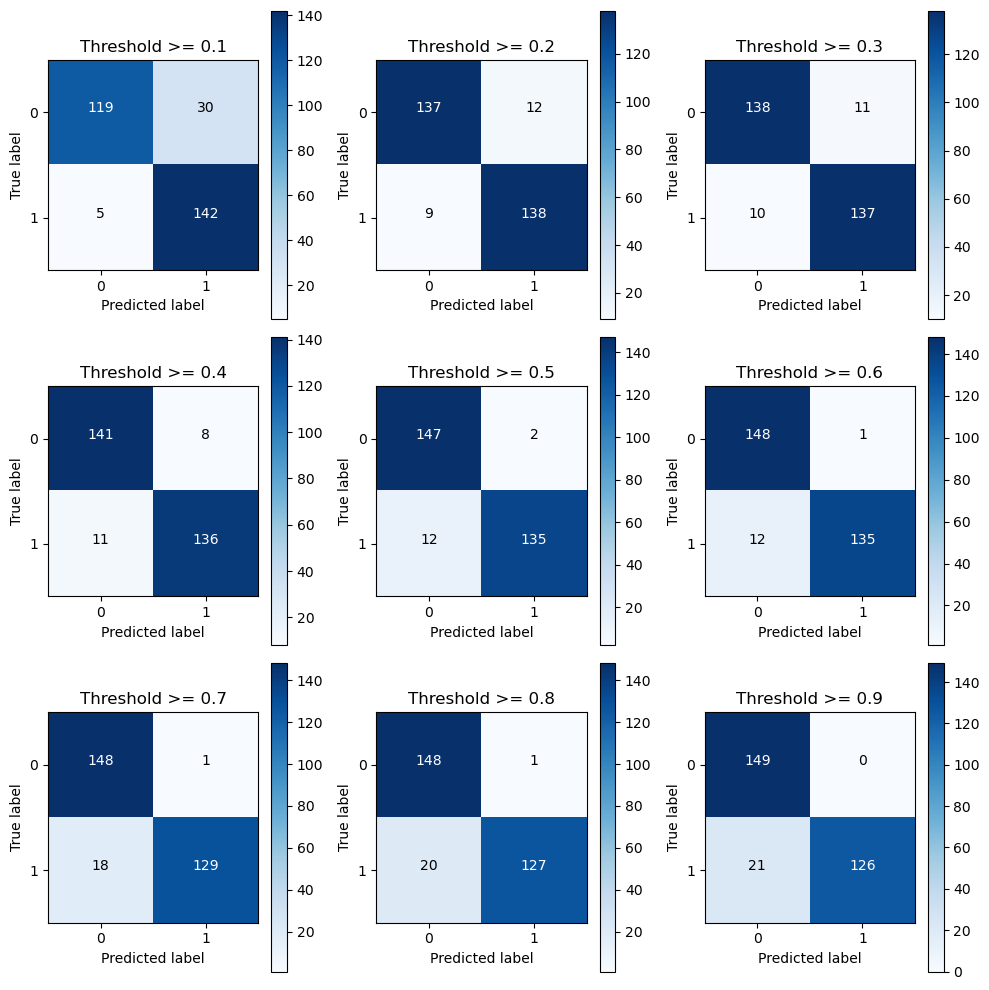

不同阈值影响

Ir = LogisticRegression(C=best_c,penalty='l2')

Ir.fit(X_train_undersample,y_train_undersample.values.ravel())

y_pred_undersample_proba = Ir.predict_proba(X_test_undersample.values)

thresholds = [0.1,0.2,0.3,0.4,0.5,0.6,0.7,0.8,0.9]

plt.figure(figsize=(10,10))

j = 1

for i in thresholds:

y_test_predictions_high_recall = y_pred_undersample_proba[:,1] > i

plt.subplot(3,3,j)

j+=1

cnf_matrix = confusion_matrix(y_test_undersample,y_test_predictions_high_recall)

np.set_printoptions(precision=2)

print("Recall metric in the testing dataset: ", cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

class_names = [0,1]

plot_confusion_matrix(cnf_matrix,

classes=class_names,

title="Threshold >= %s"%i)

Recall metric in the testing dataset: 0.9659863945578231

Recall metric in the testing dataset: 0.9387755102040817

Recall metric in the testing dataset: 0.9319727891156463

Recall metric in the testing dataset: 0.9251700680272109

Recall metric in the testing dataset: 0.9183673469387755

Recall metric in the testing dataset: 0.9183673469387755

Recall metric in the testing dataset: 0.8775510204081632

Recall metric in the testing dataset: 0.8639455782312925

Recall metric in the testing dataset: 0.8571428571428571

第二种方式 过采样方案

# 过采样, 使用 smote算法生成样本

# 引入逻辑回归模型

# 加载数据

data = pd.read_csv("E:\python学习\回归\信用卡欺诈检测\creditcard.csv")

# Amount特征值太大,进行正规化

data['normAmount'] = StandardScaler().fit_transform(data['Amount'].values.reshape(-1, 1))

# 删除无用的Time列和原 Amount列

data = data.drop(['Time', 'Amount'], axis=1)

# 获取特征列,所有行,列名不是Class的列

features = data.loc[:, data.columns != 'Class']

# 获取标签列,所有行,列名是Class的列

labels = data.loc[:, data.columns == 'Class']

# 分离训练集和测试集

features_train, features_test, labels_train, labels_test = train_test_split(features, labels, test_size=0.2, random_state=0)

from imblearn.over_sampling import SMOTE

oversampler = SMOTE(random_state=0)

os_features,os_labels=oversampler.fit_resample(features_train,labels_train)

os_features = pd.DataFrame(os_features)

os_labels = pd.DataFrame(os_labels)

best_c = printing_Kfold_scores(os_features,os_labels)

----------------------

正则化惩罚力度 0.01

----------------------

Iteration 1 :召回率 = 0.9161290322580645

Iteration 2 :召回率 = 0.9144736842105263

Iteration 3 :召回率 = 0.9105676662609273

Iteration 4 :召回率 = 0.8931754981809389

Iteration 5 :召回率 = 0.893626141721898

平均召回率: 0.905594404526471

----------------------

正则化惩罚力度 0.1

----------------------

Iteration 1 :召回率 = 0.9161290322580645

Iteration 2 :召回率 = 0.9144736842105263

Iteration 3 :召回率 = 0.9115857032200951

Iteration 4 :召回率 = 0.8943295852980293

Iteration 5 :召回率 = 0.895120959321177

平均召回率: 0.9063277928615785

----------------------

正则化惩罚力度 1

----------------------

Iteration 1 :召回率 = 0.9161290322580645

Iteration 2 :召回率 = 0.9144736842105263

Iteration 3 :召回率 = 0.911807015602523

Iteration 4 :召回率 = 0.8945384201096932

Iteration 5 :召回率 = 0.8952528549917016

平均召回率: 0.9064402014345017

----------------------

正则化惩罚力度 10

----------------------

Iteration 1 :召回率 = 0.9161290322580645

Iteration 2 :召回率 = 0.9144736842105263

Iteration 3 :召回率 = 0.9118734093172512

Iteration 4 :召回率 = 0.8945713940273244

Iteration 5 :召回率 = 0.8952528549917016

平均召回率: 0.9064600749609737

----------------------

正则化惩罚力度 100

----------------------

Iteration 1 :召回率 = 0.9161290322580645

Iteration 2 :召回率 = 0.9144736842105263

Iteration 3 :召回率 = 0.9118734093172512

Iteration 4 :召回率 = 0.8945713940273244

Iteration 5 :召回率 = 0.8952638462975786

平均召回率: 0.906462273222149

>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>

效果最好的模型选择的参数= 100.0

>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>

#### 过采样模型 应用于 过采样数据

Ir = LogisticRegression(C=best_c,penalty='l2')

Ir.fit(os_features,os_labels.values.ravel())

y_pred = Ir.predict(features_test.values)

cnf_matrix = confusion_matrix(labels_test,y_pred)

np.set_printoptions(precision=2)

print("过采样混淆矩阵:",cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

class_names = [0,1]

plt.figure()

plot_confusion_matrix(cnf_matrix,

classes=class_names,

title="confusion matrix")

plt.show()

过采样混淆矩阵: 0.9405940594059405

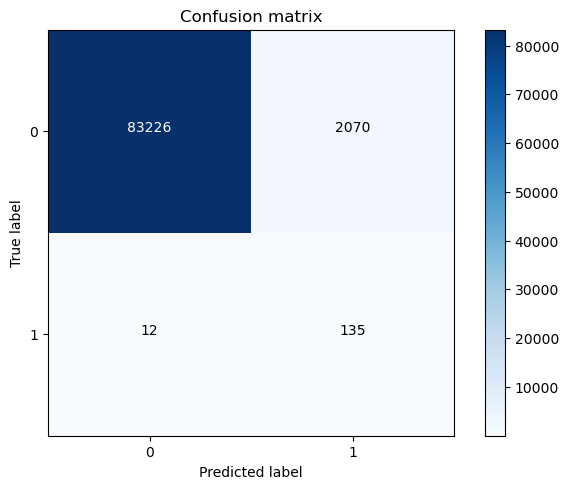

#### 过采样模型 应用于 真实数据

Ir = LogisticRegression(C=best_c,penalty='l2')

Ir.fit(os_features,os_labels.values.ravel())

y_pred = Ir.predict(X_test.values)

cnf_matrix = confusion_matrix(y_test,y_pred)

np.set_printoptions(precision=2)

print("过采样模型应用于原始数据的召回率:",cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

class_names = [0,1]

plt.figure()

plot_confusion_matrix(cnf_matrix,

classes=class_names,

title='Confusion matrix')

plt.show()

过采样模型应用于原始数据的召回率: 0.9183673469387755

【推荐】国内首个AI IDE,深度理解中文开发场景,立即下载体验Trae

【推荐】编程新体验,更懂你的AI,立即体验豆包MarsCode编程助手

【推荐】抖音旗下AI助手豆包,你的智能百科全书,全免费不限次数

【推荐】轻量又高性能的 SSH 工具 IShell:AI 加持,快人一步

· 全程不用写代码,我用AI程序员写了一个飞机大战

· DeepSeek 开源周回顾「GitHub 热点速览」

· 记一次.NET内存居高不下排查解决与启示

· MongoDB 8.0这个新功能碉堡了,比商业数据库还牛

· .NET10 - 预览版1新功能体验(一)