时间序列学习笔记4

6. 重采样及频率转换

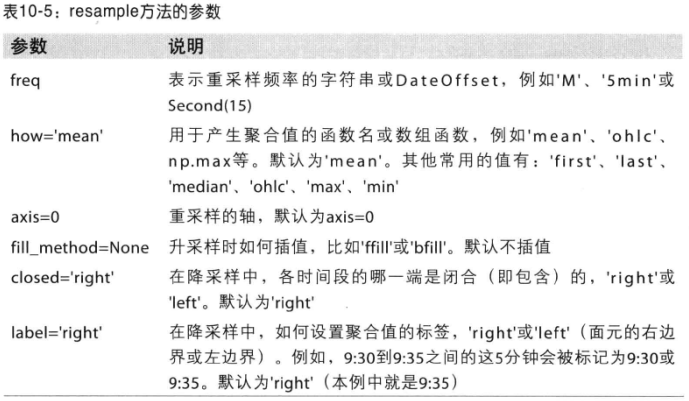

重采样(resample)表示将时间序列的频率进行转换的过程。可以分为降采样和升采样等。

pandas对象都有一个resample方法,可以进行频率转换。

In [5]: rng = pd.date_range('1/1/2000', periods=100, freq='D')

In [6]: ts = Series(np.random.randn(len(rng)), index=rng)

# 聚合后的值如何处理,使用mean(),默认即为mean,也可以使用sum,min等。

In [8]: ts.resample('M').mean()

Out[8]:

2000-01-31 -0.128802

2000-02-29 0.179255

2000-03-31 0.055778

2000-04-30 -0.736071

Freq: M, dtype: float64

In [9]: ts.resample('M', kind='period').mean()

Out[9]:

2000-01 -0.128802

2000-02 0.179255

2000-03 0.055778

2000-04 -0.736071

Freq: M, dtype: float64

6.1 降采样

# 12个每分钟 的采样

In [10]: rng = pd.date_range('1/1/2017', periods=12, freq='T')

In [11]: ts = Series(np.arange(12), index=rng)

In [12]: ts

Out[12]:

2017-01-01 00:00:00 0

2017-01-01 00:01:00 1

2017-01-01 00:02:00 2

...

2017-01-01 00:08:00 8

2017-01-01 00:09:00 9

2017-01-01 00:10:00 10

2017-01-01 00:11:00 11

Freq: T, dtype: int32

# 每隔五分钟采用,并将五分钟内的值求和,赋值到新的Series中。

# 默认 [0,4),前闭后开

In [14]: ts.resample('5min').sum()

Out[14]:

2017-01-01 00:00:00 10

2017-01-01 00:05:00 35

2017-01-01 00:10:00 21

Freq: 5T, dtype: int32

# 默认 closed就是left,

In [15]: ts.resample('5min', closed='left').sum()

Out[15]:

2017-01-01 00:00:00 10

2017-01-01 00:05:00 35

2017-01-01 00:10:00 21

Freq: 5T, dtype: int32

# 调整到右闭左开后,但是时间取值还是left

In [16]: ts.resample('5min', closed='right').sum()

Out[16]:

2016-12-31 23:55:00 0

2017-01-01 00:00:00 15

2017-01-01 00:05:00 40

2017-01-01 00:10:00 11

Freq: 5T, dtype: int32

# 时间取值也为left,默认

In [17]: ts.resample('5min', closed='left', label='left').sum()

Out[17]:

2017-01-01 00:00:00 10

2017-01-01 00:05:00 35

2017-01-01 00:10:00 21

Freq: 5T, dtype: int32

还可以调整offset

# 向前调整1秒

In [18]: ts.resample('5T', loffset='1s').sum()

Out[18]:

2017-01-01 00:00:01 10

2017-01-01 00:05:01 35

2017-01-01 00:10:01 21

Freq: 5T, dtype: int32

OHLC重采样

金融领域有一种ohlc重采样方式,即开盘、收盘、最大值和最小值。

In [19]: ts.resample('5min').ohlc()

Out[19]:

open high low close

2017-01-01 00:00:00 0 4 0 4

2017-01-01 00:05:00 5 9 5 9

2017-01-01 00:10:00 10 11 10 11

利用groupby进行重采样

In [20]: rng = pd.date_range('1/1/2017', periods=100, freq='D')

In [21]: ts = Series(np.arange(100), index=rng)

In [22]: ts.groupby(lambda x: x.month).mean()

Out[22]:

1 15.0

2 44.5

3 74.0

4 94.5

dtype: float64

In [23]: rng[0]

Out[23]: Timestamp('2017-01-01 00:00:00', offset='D')

In [24]: rng[0].month

Out[24]: 1

In [25]: ts.groupby(lambda x: x.weekday).mean()

Out[25]:

0 50.0

1 47.5

2 48.5

3 49.5

4 50.5

5 51.5

6 49.0

dtype: float64

6.2 升采样和插值

低频率到高频率的时候就会有缺失值,因此需要进行插值操作。

In [26]: frame = DataFrame(np.random.randn(2,4), index=pd.date_range('1/1/2017'

...: , periods=2, freq='W-WED'), columns=['Colorda','Texas','NewYork','Ohio

...: '])

In [27]: frame

Out[27]:

Colorda Texas NewYork Ohio

2017-01-04 1.666793 -0.478740 -0.544072 1.934226

2017-01-11 -0.407898 1.072648 1.079074 -2.922704

In [28]: df_daily = frame.resample('D')

In [30]: df_daily = frame.resample('D').mean()

In [31]: df_daily

Out[31]:

Colorda Texas NewYork Ohio

2017-01-04 1.666793 -0.478740 -0.544072 1.934226

2017-01-05 NaN NaN NaN NaN

2017-01-06 NaN NaN NaN NaN

2017-01-07 NaN NaN NaN NaN

2017-01-08 NaN NaN NaN NaN

2017-01-09 NaN NaN NaN NaN

2017-01-10 NaN NaN NaN NaN

2017-01-11 -0.407898 1.072648 1.079074 -2.922704

In [33]: frame.resample('D', fill_method='ffill')

C:\Users\yangfl\Anaconda3\Scripts\ipython-script.py:1: FutureWarning: fill_metho

d is deprecated to .resample()

the new syntax is .resample(...).ffill()

if __name__ == '__main__':

Out[33]:

Colorda Texas NewYork Ohio

2017-01-04 1.666793 -0.478740 -0.544072 1.934226

2017-01-05 1.666793 -0.478740 -0.544072 1.934226

2017-01-06 1.666793 -0.478740 -0.544072 1.934226

2017-01-07 1.666793 -0.478740 -0.544072 1.934226

2017-01-08 1.666793 -0.478740 -0.544072 1.934226

2017-01-09 1.666793 -0.478740 -0.544072 1.934226

2017-01-10 1.666793 -0.478740 -0.544072 1.934226

2017-01-11 -0.407898 1.072648 1.079074 -2.922704

In [34]: frame.resample('D', fill_method='ffill', limit=2)

C:\Users\yangfl\Anaconda3\Scripts\ipython-script.py:1: FutureWarning: fill_metho

d is deprecated to .resample()

the new syntax is .resample(...).ffill(limit=2)

if __name__ == '__main__':

Out[34]:

Colorda Texas NewYork Ohio

2017-01-04 1.666793 -0.478740 -0.544072 1.934226

2017-01-05 1.666793 -0.478740 -0.544072 1.934226

2017-01-06 1.666793 -0.478740 -0.544072 1.934226

2017-01-07 NaN NaN NaN NaN

2017-01-08 NaN NaN NaN NaN

2017-01-09 NaN NaN NaN NaN

2017-01-10 NaN NaN NaN NaN

2017-01-11 -0.407898 1.072648 1.079074 -2.922704

In [35]: frame.resample('W-THU', fill_method='ffill')

C:\Users\yangfl\Anaconda3\Scripts\ipython-script.py:1: FutureWarning: fill_metho

d is deprecated to .resample()

the new syntax is .resample(...).ffill()

if __name__ == '__main__':

Out[35]:

Colorda Texas NewYork Ohio

2017-01-05 1.666793 -0.478740 -0.544072 1.934226

2017-01-12 -0.407898 1.072648 1.079074 -2.922704

In [38]: frame.resample('W-THU').ffill()

Out[38]:

Colorda Texas NewYork Ohio

2017-01-05 1.666793 -0.478740 -0.544072 1.934226

2017-01-12 -0.407898 1.072648 1.079074 -2.922704

6.3 通过时期(period)进行重采样

# 创建一个每月随机数据,两年

In [41]: frame = DataFrame(np.random.randn(24,4), index=pd.date_range('1-2017',

...: '1-2019', freq='M'), columns=['Colorda','Texas','NewYork','Ohio'])

# 每年平均值进行重采样

In [42]: a_frame = frame.resample('A-DEC').mean()

In [43]: a_frame

Out[43]:

Colorda Texas NewYork Ohio

2017-12-31 -0.441948 -0.040711 0.036633 -0.328769

2018-12-31 -0.121778 0.181043 -0.004376 0.085500

# 按季度进行采用

In [45]: a_frame.resample('Q-DEC').ffill()

Out[45]:

Colorda Texas NewYork Ohio

2017-12-31 -0.441948 -0.040711 0.036633 -0.328769

2018-03-31 -0.441948 -0.040711 0.036633 -0.328769

2018-06-30 -0.441948 -0.040711 0.036633 -0.328769

2018-09-30 -0.441948 -0.040711 0.036633 -0.328769

2018-12-31 -0.121778 0.181043 -0.004376 0.085500

In [49]: frame.resample('Q-DEC').mean()

Out[49]:

Colorda Texas NewYork Ohio

2017-03-31 -0.445315 0.488191 -0.543567 -0.459284

2017-06-30 -0.157438 -0.680145 0.295301 -0.118013

2017-09-30 -0.151736 0.092512 0.684201 -0.035097

2017-12-31 -1.013302 -0.063404 -0.289404 -0.702681

2018-03-31 0.157538 -0.175134 -0.548305 0.609768

2018-06-30 -0.231697 -0.094108 0.224245 -0.151958

2018-09-30 -0.614219 0.308801 -0.205952 0.154302

2018-12-31 0.201266 0.684613 0.512506 -0.270111

7. 时间序列绘图

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

from pandas import Series,DataFrame

frame = DataFrame(np.random.randn(20,3),

index = pd.date_range('1/1/2017', periods=20, freq='M'),

columns=['randn1','randn2','randn3']

)

frame.plot()

8. 移动窗口函数

待续。。。

9. 性能和内存使用方面的注意事项

In [50]: rng = pd.date_range('1/1/2017', periods=10000000, freq='1s')

In [51]: ts = Series(np.random.randn(len(rng)), index=rng)

In [52]: %timeit ts.resample('15s').ohlc()

1 loop, best of 3: 222 ms per loop

In [53]: %timeit ts.resample('15min').ohlc()

10 loops, best of 3: 152 ms per loop

貌似现在还有所下降。

浙公网安备 33010602011771号

浙公网安备 33010602011771号