Financial Reporting and Analysis 5

R19:Understanding Cash Flow Statement

1、Components and Format of the Cash Flow Statement:现金流量表的组成部分和格式

1.1 Classification of Cash Flows:现金流的分类

The cash flow statement provides information about a company's cash receipts and cash payments during an accounting period. These cash flows are classified as follows:

现金流量表提供了公司在一个会计期间的现金收支情况。这些现金流分类如下:

- Operating cash flows(CFO):

Include the company's day-to-day activities that create revenues, such as selling inventory and providing services.

- 经营性现金流(CFO):

包括公司创造收入的日常活动,如销售存货和提供服务。

- Investing cash flows(CFI):

Include purchasing and selling long-term assets and other investments, such as property and equipment.

-投资性现金流(CFI):

包括购买和出售长期资产和其他投资,如房产和设备。

- Financing cash flows(CFF):

Include obtaining or repaying capital, such as equity and long-term debt.

-融资性现金流(CFF):

包括获取或偿还资本,如股权和长期债务。

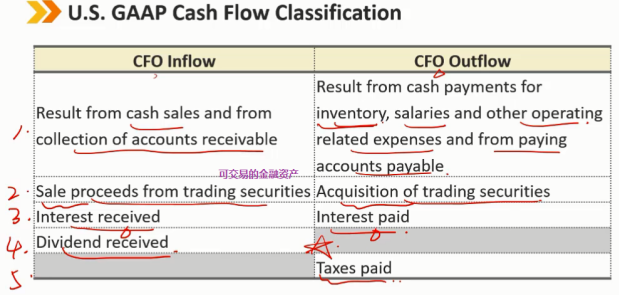

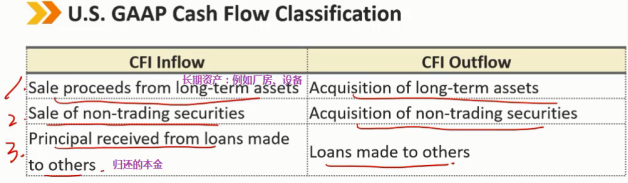

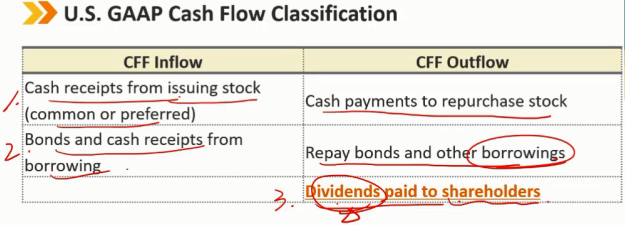

1.2 U.S.GAAP Cash Flow Classification:美国会计准则现金流量分类

2、可交易金融资产,在美国认为能利用闲钱今天投资获得一些短期收益,是一种经营能力强的表现,所以归在经营性现金流当中 4、支付的股利不算在经营性现金流当中,是因为计算 net income 时也不包括支付的股利 4、分红的股利算经营性现金流的流入,但是支出的股利不算在经营性现金流当中 注:CFO 相当于利润表中的 net income,只不过两个的视角不同,一个是收付实现制下的,一个是权责发生制下的

2、非交易的长期金融资产,例如长期债券、股权投资 3、给其他企业提供贷款,主要是看中他人支付的利息,所以也算投资性现金流,他人归还的本金算投资性现金流的流入,但是利息不算,利息算经营性现金流的流入

3、支付给股东的股利归在融资性现金流的流出中,是因为 net income 的计算过程中也是不包括支付的股利的

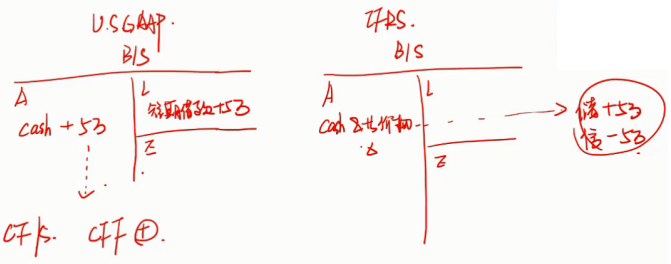

1.3 Summary of Differences Between IFRS and U.S.GAAP:国际会计准则与美国会计准则之间的差异

银行的透支:相当于银行给企业的一张信用卡,算作一笔贷款

1.4 Non-Cash Transaction:非现金交易的处理

A non-cash transaction is any transaction that does not involve an inflow or outflow of cash.

非现金交易是指不涉及现金流入或流出的任何交易。

For example:

- A company exchanges one non-monetary asset for another non-monetary asset, no cash is involved.

- A company issues common stock either for dividends or in connection with conversion of a convertible bond or convertible preferred stock.

例如:

- 一家公司用一种非货币性资产交换另一种非货币性资产,不涉及现金。

- 公司发行普通股用于股息或与可转换债券或可转换优先股的转换有关。

These transactions are not incorporated in the cash flow statement. However, any significant non-cash transaction is required to be disclosed, either in a separate note or a supplementary schedule to the cash flow statement.

这些交易不包含在现金流量表中。但是,任何重大非现金交易都需要在单独的附注或现金流量表的补充附表中披露。

2、Cash Flow Calculation:现金流的计算

Direct & Indirect Method:直接法和间接法

There are two acceptable formats for reporting cash flow from operating activities: direct and indirect methods.

报告经营活动现金流量有两种可接受的格式:直接法和间接法。

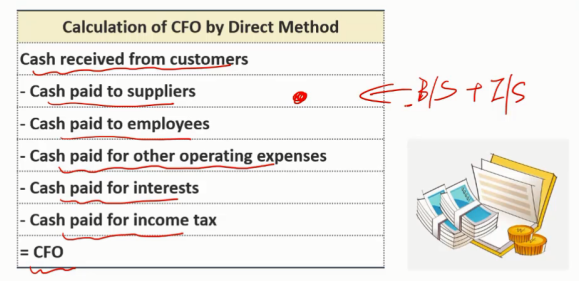

Direct method(for CFO/CFI/CFF):直接法(针对CFO/CFI/CFF)

- Shows the specific cash inflows and outflows that result in reported cash flow from operating activities. In other words, it shows only cash receipts and cash payments.

- 显示导致报告的经营活动现金流的具体现金流入和流出。换句话说,它只显示现金收入和现金支付。

Indirect method(for CFO only):间接法(仅适用于CFO)

- Begins with net income, shows how cash flow from operations can be obtained from reported net income as the result of a series of adjustments.

- 从净收入开始,说明如何通过一系列调整从报告的净收入中获得经营活动产生的现金流。

2.1 CFO Calculation:

(1)CFO Calculation:Direct Method

☆ 重点是知道如何从利润表和资产负债表中得出计算CFO的这些相关项

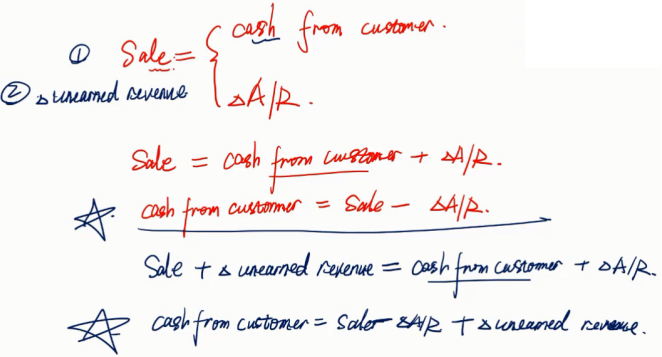

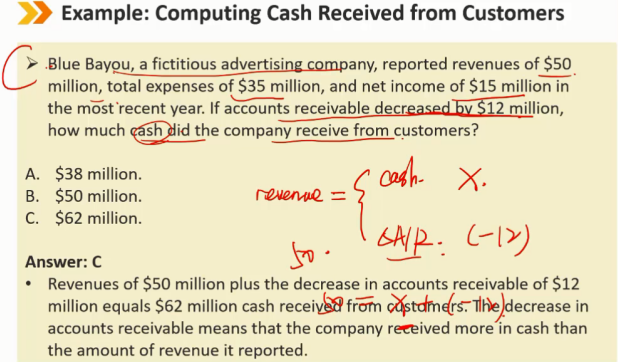

<1> Cash received from customers = Net sales - △A/R + △Unearned revenue

收到客户的现金 = 净销售额 - 应收账款的变动值 + 预收收入的变动值

出售货物或服务的销售收入:Net sales、 △Unearned revenue

对应从客户那边收到钱的形式:Cash received from customers、 △A/R

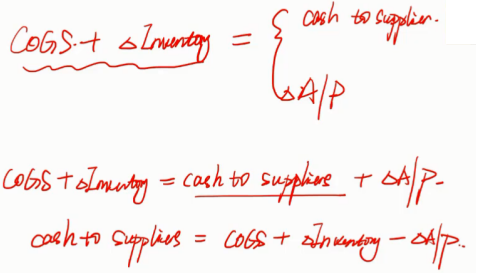

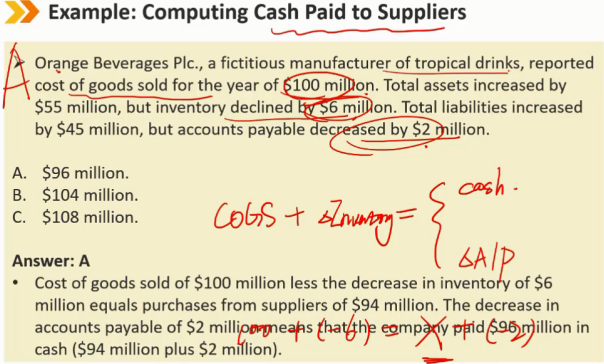

<2> Cash paid to suppliers = COGS + △Inventory - △A/P

付给供货商的现金 = COGS + 存货的变动值 - 应付费用的变动值

从供货商那里收到的货物:COGS(销售出去了的)、△Inventory(未销售出去的)

给供货商钱的形式:Cash paid to suppliers、△A/P

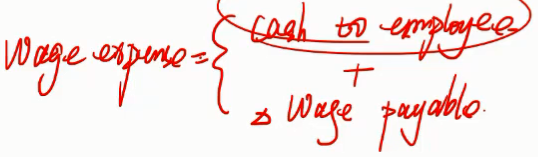

<3> Cash paid to employees = Wage expense - △Wage payable

支付给员工的现金 = 工资费用 - △应付职工薪酬

工资费用:付给员工的现金,应付职工薪酬的变动值

<4> Cash paid for interests = Interest expense - △lnterest payable

支付利息的现金 = 利息费用 - △应付利息

<5> Cash paid for income tax = Income tax expense - △Tax payable

支付所得税的现金 = 所得税费用 - △应付税款

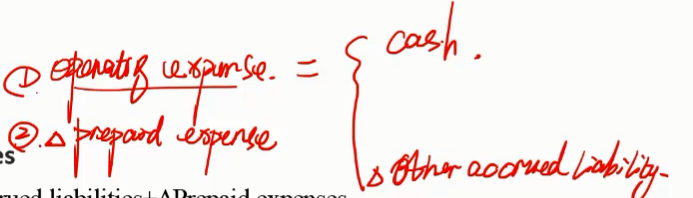

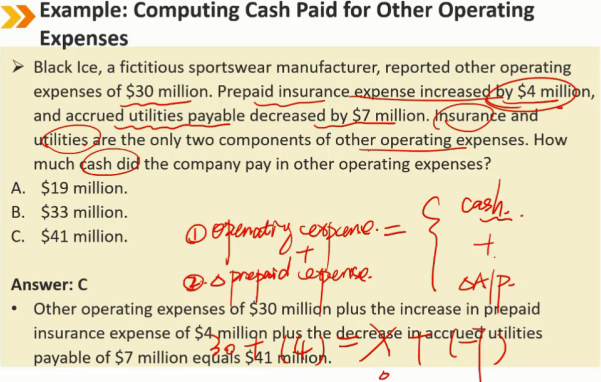

<6> Cash paid for other operating expenses = Other operating expense - △Other accrued liabilities + △Prepaid expenses

支付其他营业费用的现金 = 其他营业费用 - △其他应计负债 + △预付费用

营业费用的分类:Other operating expense(当前花费的)、△Prepaid expenses(预先支付的)

营业费用的支付方式:Cash(已经支付的)、△Other accrued liabilities(还未支付的)

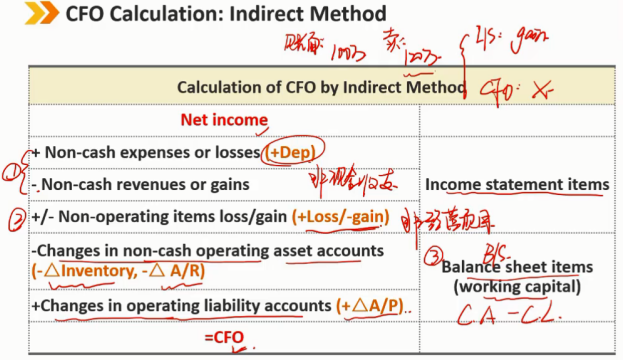

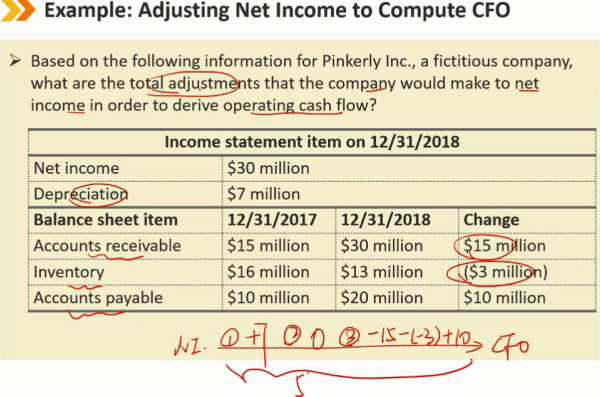

(2)CFO Calculation: Indirect Method

调整原则:从net income调整到CFO,如果有的项目在net income中有,在CFO中没有,需要剔除,如果在CFO中有体现,在net income中没有,则需要加回来

1.非现金的收支

Non-cash expenses or losses(例如折旧):在计算net income时减去了,在计算CFO时应该加回来

Non-cash revenues or gains(非现金收入):在计算net income时加上了,则在计算CFO时应该减去

2.非经营性的项目

例如:处置厂房得到 Gain 20万,在利润表例会增加20万,但是该收入应该算CFI中,所以计算CFO时应该减去

3.资产负债表中的涉及的项目是流动项目,流动资产和流动负债中非现金的科目

花20万购买存货,现金减少20万,存货增加20万,因为存货没有卖出去,所以NI的变化是0,现金减少20万导致CFO减少20万,于是通过NI调整到CFO需要减去存货的变动值

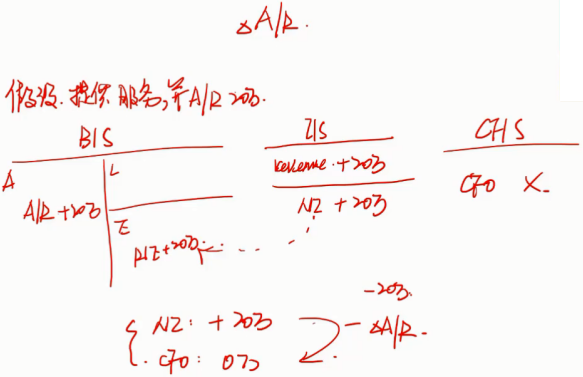

提供服务获得应收账款20万,服务已经提供,所以NI增加20万,但是现金还未流入,所以CFO是0,于是NI调整到CFO需要减去应收账款的变动值

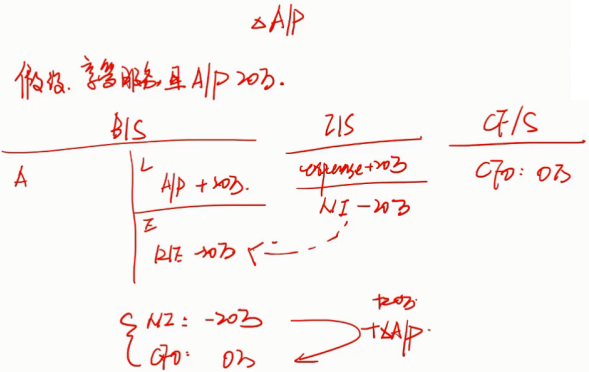

别人提供服务,我们有20万的应付账款,此时NI为-20万,CFO为0,所以从NI调整CFO需要加上应付账款的变动值

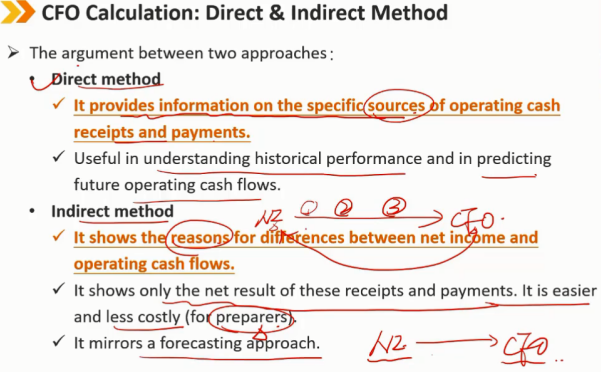

(3)The argument between two approaches:两种方法的讨论

・直接法: - 它提供有关经营现金具体来源的信息收支情况。 - 有助于了解历史业绩和预测未来经营现金流。 ・间接法: - 它显示了净收入和经营现金流之间差异的原因。 - 它只显示这些收支的净结果。它更容易,成本更低(对于准备者)。 - 它反映了一种预测方法。

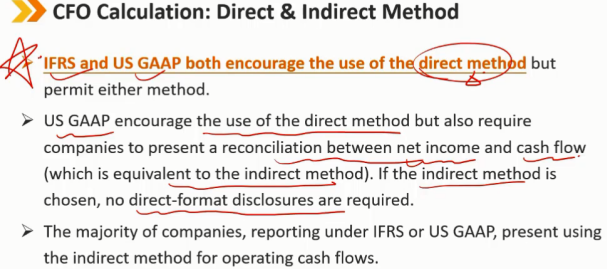

国际财务报告准则和美国公认会计准则都鼓励使用直接法,但允许使用任何一种方法

美国公认会计原则鼓励使用直接法,但也要求公司在净收入和现金流量之间进行对账(相当于间接法)。如果选择间接法,则无需直接法格式的披露

根据国际财务报告准则或美国公认会计原则报告的大多数公司采用间接法计算经营现金流量

2.2 CFI Calculation:

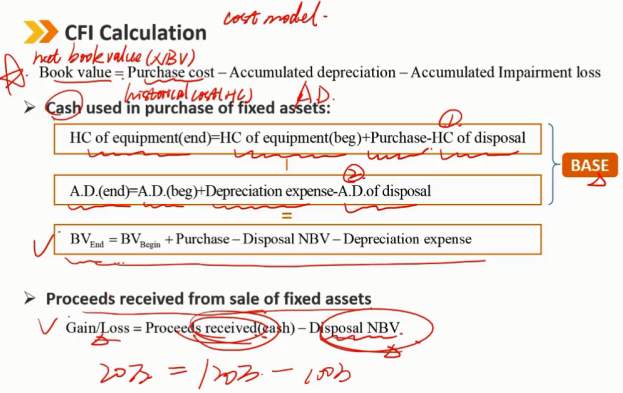

Cost model:成本法估计固定资产价值

Book value = Purchase cost - Accumulated depreciation - Accumulated Impairment loss

账面价值 = 历史成本 - 累计折旧 - 累计减值

历史成本:Historical cost, Purchase cost

账面价值:Book value , Net book value, carrying amount, carrying value

累计折旧:A.D.

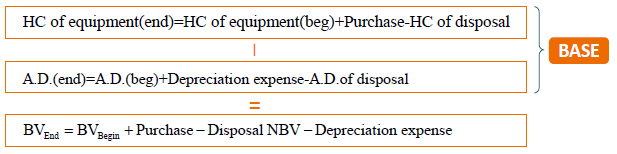

Cash used in purchase of fixed assets:

历史成本和累计折旧都是资产负债表的科目,满足BASE法则

通过BASE计算历史成本和累计折旧,两式相减

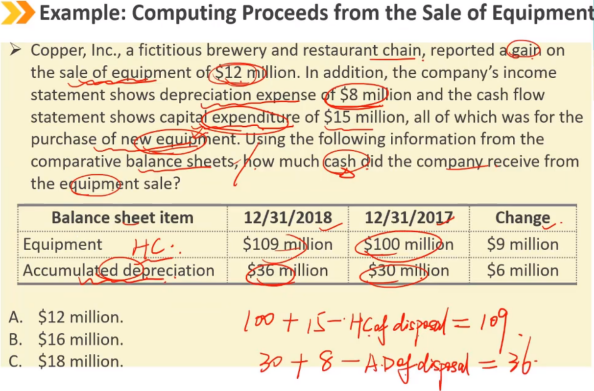

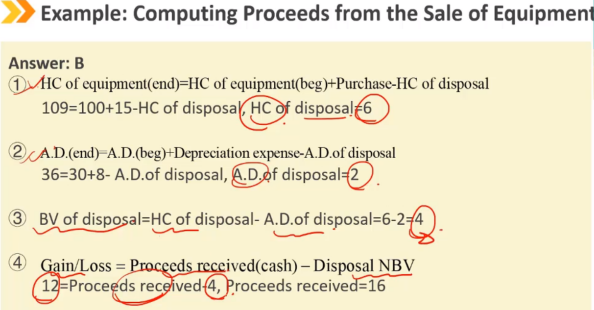

Proceeds received from sale of fixed assets:出售固定资产所得收益

Gain / Loss = Proceeds received(cash) - Disposal NBV

收益 / 损失 = 收到的收益(现金)- 处置资产的账面价值

例如:处置一项资产获得120万,该资产的账面价值是100万,则获得20万收益

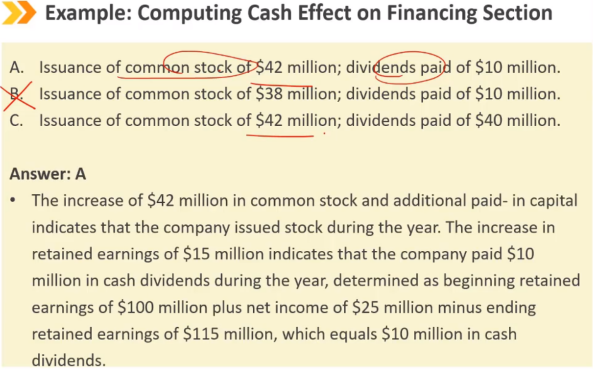

2.3 CFF Calculation:

Long-term debt and common stock:发行股票和债券融到的钱数计算

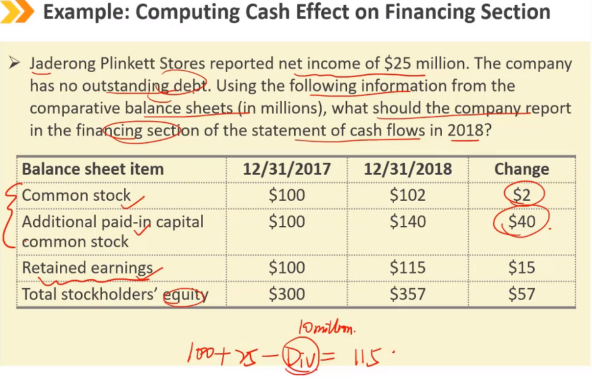

Issuance of common stock = Ending common stock + Ending additional paid-in capital - Opening common stock - Opening additional paid-in capital

发行股票融到的现金 = 期末普通股股本 + 期末资本公积 - 期初普通股股本 - 期初资本公积

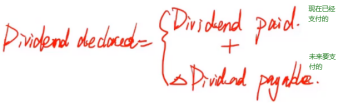

Dividend:股利计算

Dividend paid = Dividend declared - △Dividend payables

实际支付股利 = 宣告股利 - 应付股利的变动值

Ending R/E = Opening R/E + Net income - Dividend declared

期末的留存收益 = 期初的留存收益 + 净利润 - 宣告股利

注:因为这里的科目是利润表和资产负债表里的,所以得用宣告的股利,满足权责发生制,不能用实际支付的股利

3、Analysis of Cash Flow Statement:现金流量表的分析

3.1 Evaluation of the Sources and Uses of Cash:现金的来源和使用的评估

Step1: An overall assessment of the maior sources and uses of cash:对现金的主要来源和使用进行全面评估

- The major sources of cash for a company can vary with its stage of growth

- 公司的主要现金来源可能因其成长阶段而异

例如:初创型公司资金来源多为融资,发展到一定规模的企业其资金来源多为依靠自身经营

- It is desirable that operating cash flows are sufficient to cover capital expenditures

- 营业现金流应足以支付资本支出

Step 2: Within the operating section:在CFO板块

- Examine the most significant determinants of operating cash flow

- 检查经营现金流的最重要决定因素

例如:主要花在哪些方面,进货,发工资等等

- Examine the relationship between net income and operating cash flow

- 检查净利润和经营现金流之间的关系

例如:通过CFO检验净利润是不是有问题

- Examine the variability of both earnings and cash flow

- 检查收益和现金流的波动性

例如:可以看出每年该企业现金流是否稳定

Step 3: Within the investing section:在CFI板块

- How much cash is being invested for the future in PP&E and how much is put aside in liquid investments

- 有多少现金被投资于未来的固定资产投资,有多少资金被用于流动性投资

- If assets are being sold, it is important to determine why and to assess the effects on the company

- 如果出售资产,确定原因和评估对公司的影响很重要

Step 4: Within the financing section:在CFF板块

- Whether the company is raising capital or repaying capital

- 公司是否正在融资或偿还资金

- What the nature of its capital sources are

- 其资本来源的性质是什么(债券比例,股票比例)

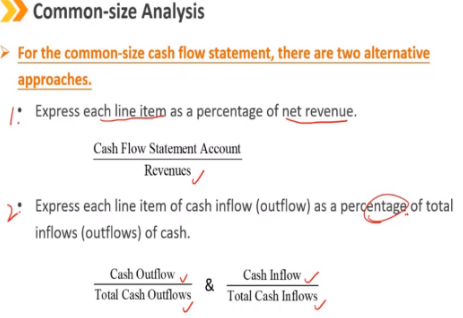

3.2 Common-Size Analysis of the Statement of Cash Flows:现金流量表的同型分析

对于一般规模的现金流量表,有两种同型的分析方法 1、分母是比上净收入 2、根据现金流的流入和流出进行分类,分母对应比上总流入或总流出

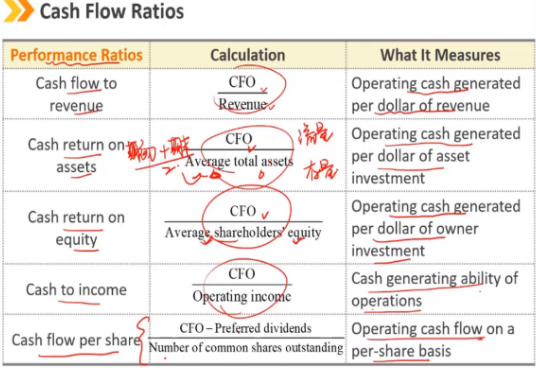

3.3 Cash Flow Ratios:现金流量比率指标

表现类指标 1、1美元收入可以产生多少CFO 2、投入1美元资产可以产生多少CFO 3、1美元的equity的投资可以产生多少CFO 4、通过日常经营可以获取现金的能力 5、每1股普通股可以产生多少CFO

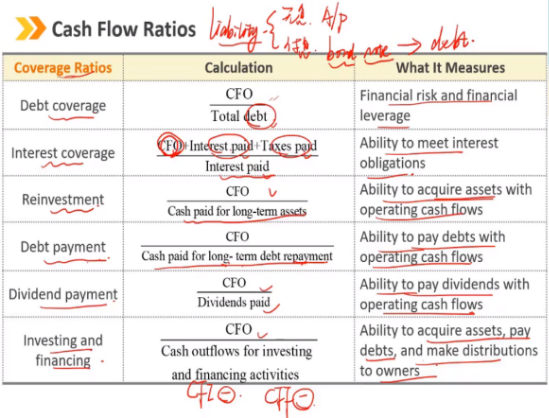

覆盖比率:看看CFO是否足以覆盖掉这些支出 1、衡量企业财务上的风险和杠杆 2、衡量的是CFO支付利息的能力,因为CFO在计算的时候已经减去了利息和税,所以在计算这项比率时需要先加回利息和税之后,再计算覆盖比率 3、衡量的是CFO购买资产的能力 4、衡量的是CFO偿付负债的能力(repayment是偿付本金) 5、衡量的是CFO支付股利的能力 6、衡量的是CFO是否可以覆盖CFI和CFF的流出

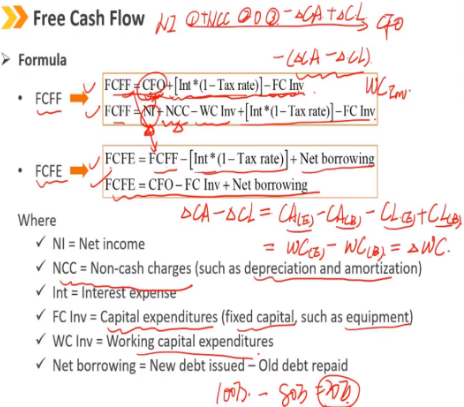

3.4 Free Cash Flow:自由现金流

Definition:The excess of operating cash flow over capital expenditures.

经营现金流超过资本支出的部分,即企业在满足运营之外多挣出来的可自由支配的现金流

Free cash flow to firm(FCFF):公司自由现金流(FCFF)

- Cash flow available to the company's suppliers of debt and equity capital after all operating expenses( including income taxes) have been paid and necessary investments in working capital and fixed capital have been made.

- 支付所有运营费用(包括所得税)并对营运资本和固定资本进行必要投资后,公司债务和股本供应商可获得的现金流。

Free cash flow to equity(FCFE):股东自由现金流(FCFE)

- Cash flow available to the company's common stockholders after all operating expenses and borrowing costs( principal and interest) have been paid and necessary investments in working capital and fixed capital have been made.

- 支付所有运营费用和借款成本(支付给债权人的本金和利息)以及对营运资本和固定资本进行必要投资后,公司普通股股东可获得的现金流。

NI = Net income NCC = Non-cash charges( such as depreciation and amortization) 非现金的费用:折旧和摊销的费用 Int= Interest expense 利息费用:CFO中已经将这部分减去了,对于计算公司自由现金流FCFF来说,需要把这部分加回来,它也算是整个公司可以支配的现金流,但是这项要扣税,所以为 Int *(1-Tax rate),对于股东来说,这部分不是股东可以自由支配的现金流,必须支付给债权人的 FC Inv = Capital expenditures( fixed capital, such as equipment) 资本支出:购买固定资产(机器设备、厂房等)的花销 WC Inv = Working capital expenditures 营运资本 Working Captical 的支出 Net borrowing = New debt issued - Old debt repaid 净融资金额:新发行债券融到的钱减去偿付老债券的金额,这部分也是股东可以自由支配的现金流

Summary:

【推荐】国内首个AI IDE,深度理解中文开发场景,立即下载体验Trae

【推荐】编程新体验,更懂你的AI,立即体验豆包MarsCode编程助手

【推荐】抖音旗下AI助手豆包,你的智能百科全书,全免费不限次数

【推荐】轻量又高性能的 SSH 工具 IShell:AI 加持,快人一步

· 被坑几百块钱后,我竟然真的恢复了删除的微信聊天记录!

· 没有Manus邀请码?试试免邀请码的MGX或者开源的OpenManus吧

· 【自荐】一款简洁、开源的在线白板工具 Drawnix

· 园子的第一款AI主题卫衣上架——"HELLO! HOW CAN I ASSIST YOU TODAY

· Docker 太简单,K8s 太复杂?w7panel 让容器管理更轻松!