scorecardpy 介绍

前语:平时计算变量IV值时也有调用过scorecardpy库,不过总体来说使用次数不多,对此功能也不是很熟悉,一般都是使用自己内部的库,但是涉及到去其他公司建模,或者是一个封闭的环境时,常常不能使用自己的东西,这就得使用toad或者scorecardpy,下面简单介绍一下,不过着重点还是一下三点:

(1)将iv(输出是一个字典)输出结果,转化成pd.df;iv参数的使用;

(2)转换评分卡 ,scorecardpy内置的模型时sklearn 的逻辑回归,如果使用其他的,比如statsmodels.api 的逻辑回归,又该如何应对;

(3)如果使用scorecardpy,整个建模流程是如何。

下面开始本次学习之旅,以及解决上面三个问题。

一、导入数据

使用的是scorecardpy内置的数据作为例子

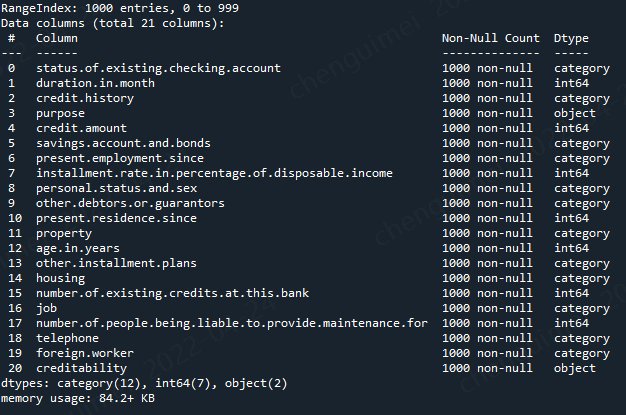

import scorecardpy as sc # 加载德国信用卡相关数据集 dat = sc.germancredit()

dat.info()

二、计算变量iv

看其他的介绍文档里面,这一步是变量刷选,但是我觉得首先要对变量的整体情况有一定了解,再去刷选变量,所以这一步先计算变量iv

使用函数是sc.woebin()

sc.woebin?? def woebin(dt, y, x=None, var_skip=None, breaks_list=None, special_values=None, stop_limit=0.1, count_distr_limit=0.05, bin_num_limit=8, # min_perc_fine_bin=0.02, min_perc_coarse_bin=0.05, max_num_bin=8, positive="bad|1", no_cores=None, print_step=0, method="tree", ignore_const_cols=True, ignore_datetime_cols=True, check_cate_num=True, replace_blank=True, save_breaks_list=None, **kwargs):

woebin()可针对数值型和类别型变量生成最优分箱结果,方法可选择决策树分箱、卡方分箱或自定义分箱。其他各参数的含义如下:

- var_skip: 设置需要跳过分箱操作的变量;

- breaks_list: 切分点列表,默认为空。如果非空,则按设置的切分点进行分箱处理;

- special_values: 设置需要单独分箱的值,默认为空;

- count_distr_limit: 设置分箱占比的最小值,一般可接受范围为0.01-0.2,默认值为0.05;

- stop_limit: 当IV值的增长率小于所设置的stop_limit,或卡方值小于qchisq(1-stoplimit, 1)时,停止分箱。一般可接受范围为0-0.5,默认值为0.1;

- bin_num_limit: 该参数为整数,代表最大分箱数。

- positive: 指定样本中正样本对应的标签,默认为"bad|1";

- no_cores: 设置用于并行计算的 CPU 数目;

- print_step: 该参数为非负数,默认值为1。若print_step>0,每次迭代会输出变量名。若iteration=0或no_cores>1,不会输出任何信息;

- method: 设置分箱方法,可设置"tree"(决策树)或"chimerge"(卡方),默认值为"tree";

- ignore_const_cols: 是否忽略常数列,默认值为True,即忽略常数列;

- ignore_datetime_cols: 是否忽略日期列,默认值为True,即忽略日期列;

- check_cate_num: 检查类别变量中枚举值数目是否大于50,默认值为True,即自动进行检查。若枚举值过多,会影响分箱过程的速度;

- replace_blank: 设置是否将空值填为None,默认为True。

一般设置这三个参数即可,其余的使用默认参数

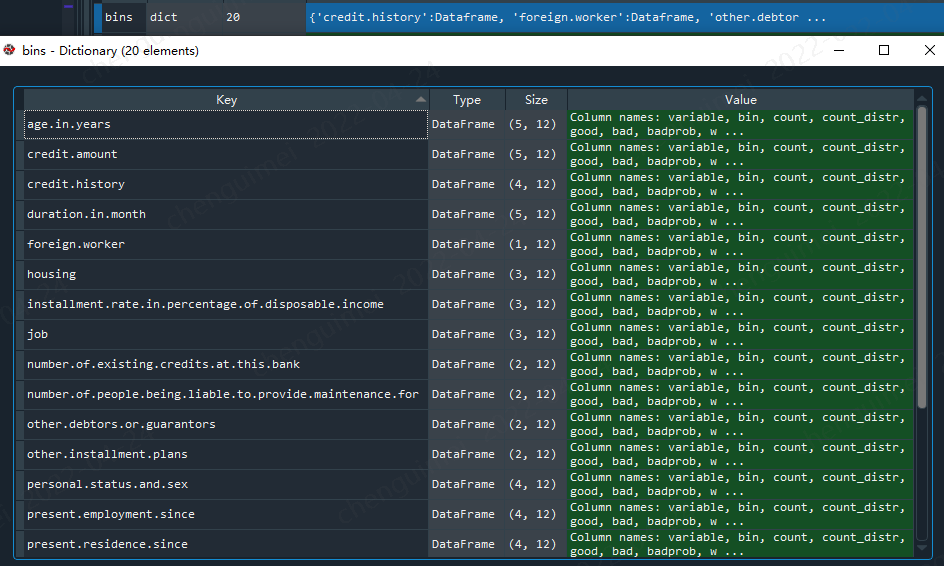

#如果special_values=-1000,可以这样表示,就会将-1000作为单独的一箱 bins = sc.woebin(dat, y="creditability",count_distr_limit=0.05, bin_num_limit=5)

我们需要将dict转为pd.df

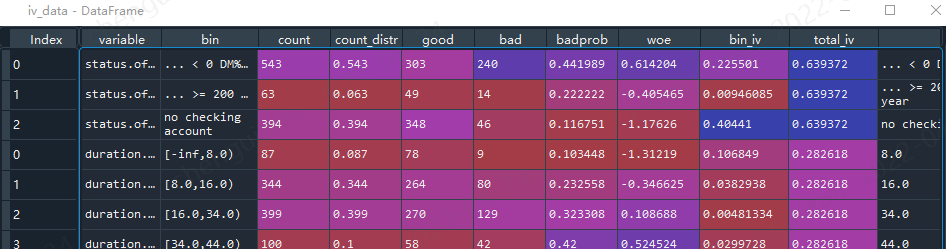

import pandas as pd iv_data = pd.DataFrame() for i in dat.columns[0:-1]: iv_data = iv_data.append(bins[i])

这样就比较好看。且容易分析比较

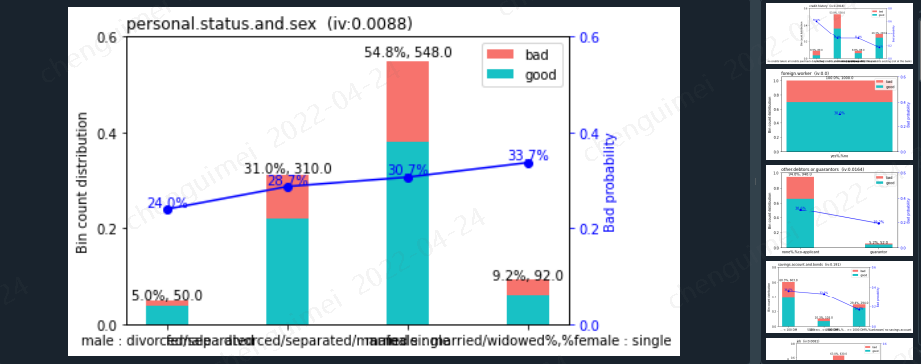

当然你也可以使用画图的形式(但是图片占用内存过大,且当变量特别多时候,看起来也很困难,因此我一般不使用),就会输出每个变量的分箱图片。

sc.woebin_plot(bins)

调箱可以这样处理,breaks_list,参数是dict形式

breaks_adj = { 'age.in.years': [26, 35, 40], 'other.debtors.or.guarantors': ["none", "co-applicant%,%guarantor"] } bins_adj = sc.woebin(dat, y="creditability", breaks_list=breaks_adj) bins_adj['age.in.years']

三、划分数据集

sc内置了一个划分数据集的函数,但其实是使用df.sample()函数,里面也2个参数,可以自己设置

train, test = sc.split_df(dat, 'creditability').values() #def split_df(dt, y=None, ratio=0.7, seed=186)

四、刷选变量

先介绍sc里面的用法,var_filter根据IV 值小于0.02,或缺失率大于95%,或同值率(除空值外)大于95% 去剔除变量

def var_filter(dt, y, x=None, iv_limit=0.02, missing_limit=0.95, identical_limit=0.95, var_rm=None, var_kp=None, return_rm_reason=False, positive='bad|1')

其中各参数含义如下:

- varrm可设置强制保留的变量,默认为空;

- varkp可设置强制剔除的变量,默认为空;

- return_rm_reason可设置是否返回剔除原因,默认为不返回(False);

- positive可设置坏样本对应的值,默认为“bad|1”。

dt_s = sc.var_filter(dat, y="creditability")

其实更建议手动挑选,因为做评分卡需要模型有可解释性,也就是要求模型入模变量符合业务解释,要求单调性等等,单纯的iv可能选择不了最符合的。

不过变量很多时,可以用来做初刷。

五、woe转换

使用woebin_ply()函数对变量进行woe变换,最后变量是以woe结尾

cols = list(dt_s.columns) train_woe = sc.woebin_ply(train[cols], bins_adj) test_woe = sc.woebin_ply(test[cols], bins_adj) train_woe.columns ''' Index(['creditability', 'credit.history_woe', 'purpose_woe', 'other.debtors.or.guarantors_woe', 'duration.in.month_woe', 'present.employment.since_woe', 'savings.account.and.bonds_woe', 'installment.rate.in.percentage.of.disposable.income_woe', 'status.of.existing.checking.account_woe', 'age.in.years_woe', 'housing_woe', 'other.installment.plans_woe', 'credit.amount_woe', 'property_woe'], dtype='object') '''

六、模型训练

需要注意,lr.coef_,lr.intercept_ ,转换成评分卡时候能够用得到。

y_train = train_woe.loc[:,'creditability'] X_train = train_woe.loc[:,train_woe.columns != 'creditability'] y_test = test_woe.loc[:,'creditability'] X_test = test_woe.loc[:,train_woe.columns != 'creditability'] # 逻辑回归 ------ from sklearn.linear_model import LogisticRegression lr = LogisticRegression(penalty='l1', C=0.9, solver='saga', n_jobs=-1) lr.fit(X_train, y_train) lr.coef_ lr.intercept_ # 预测 train_pred = lr.predict_proba(X_train)[:,1] test_pred = lr.predict_proba(X_test)[:,1]

有一个系数为0,说明该系数对应的变量是没有用处的。

当然我们也可以使用statsmodels.api 的逻辑回归

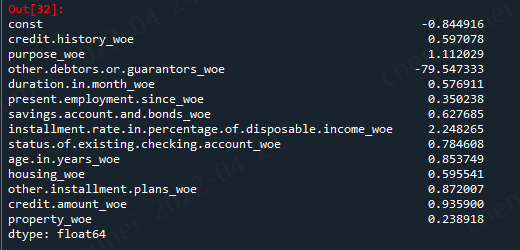

import pandas as pd import matplotlib.pyplot as plt #导入图像库 import matplotlib import seaborn as sns import statsmodels.api as sm from sklearn.metrics import roc_curve, auc from sklearn.model_selection import train_test_split target_train = y_train.map({'good':0,'bad':1}) target_test = y_test.map({'good':0,'bad':1}) X1=sm.add_constant(X_train) #在X前加上一列常数1,方便做带截距项的回归 logit=sm.Logit(target_train.values,X1.astype(float)) result=logit.fit() result.summary() result.params

但是有一个变量的系数是负值,意味着这些变量之间存在着共线性,我们需要将次去掉

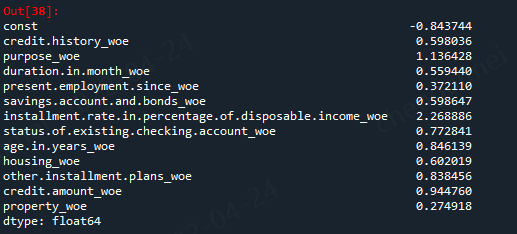

model_cols = ['credit.history_woe', 'purpose_woe', #'other.debtors.or.guarantors_woe', 'duration.in.month_woe', 'present.employment.since_woe', 'savings.account.and.bonds_woe', 'installment.rate.in.percentage.of.disposable.income_woe', 'status.of.existing.checking.account_woe', 'age.in.years_woe', 'housing_woe', 'other.installment.plans_woe', 'credit.amount_woe', 'property_woe'] X1=sm.add_constant(X_train[model_cols]) #在X前加上一列常数1,方便做带截距项的回归 logit=sm.Logit(target_train.values,X1.astype(float)) result=logit.fit() result.summary() result.params

这样子就OK了

#预测 #训练集 resu_01 = result.predict(X1) #测试集 X2 = sm.add_constant(X_test) resu_02 = result.predict(X2.astype(float))

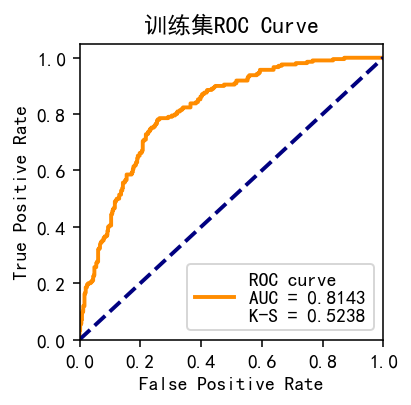

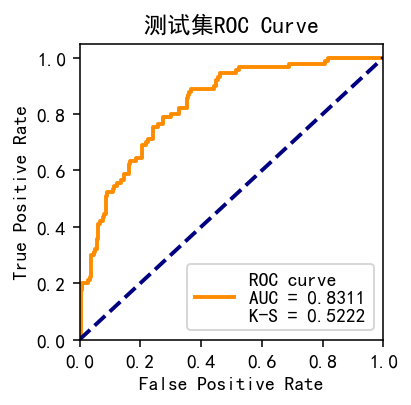

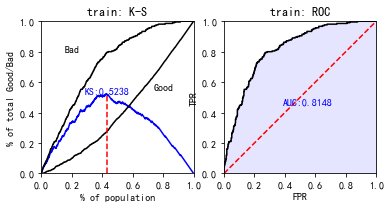

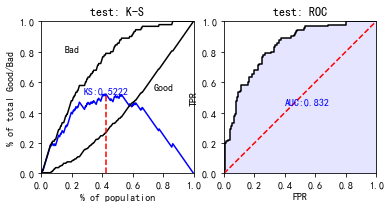

查看模型效果

#构建一个画auc和ks的图像 from sklearn.metrics import roc_curve,auc import matplotlib.pyplot as plt plt.rcParams['font.sans-serif'] = ['SimHei'] def plot_roc(p1, p,string): ''' 目标:计算出分类模型的ks值 变量: self:模型fit(x,y),如(self=tree.fit(x,y)) data:一般是训练集(不包括label)或者是测试集(也是不包括label) y:label的column_name 返回:训练集(或者测试集)的auc的图片 ''' fpr, tpr, p_threshold = roc_curve(p1, p, drop_intermediate=False, pos_label=1) df = pd.DataFrame({'fpr': fpr, 'tpr': tpr, 'p': p_threshold}) df.loc[0, 'p'] = max(p) ks = (df['tpr'] - df['fpr']).max() roc_auc = auc(fpr, tpr) fig = plt.figure(figsize=(2.8, 2.8), dpi=140) ax = fig.add_subplot(111) ax.plot(fpr, tpr, color='darkorange', lw=2, label='ROC curve\nAUC = %0.4f\nK-S = %0.4f' % (roc_auc, ks) ) ax.plot([0, 1], [0, 1], color='navy', lw=2, linestyle='--') ax.set_xlim([0.0, 1.0]) ax.set_ylim([0.0, 1.05]) ax.set_xlabel('False Positive Rate') ax.set_ylabel('True Positive Rate') ax.set_title(string) ax.legend(loc="lower right") plt.close() return fig

分别对比两种不同方式的效果

#statsmodels.api plot_roc(target_train.values, resu_01,'训练集ROC Curve') #训练集 plot_roc(target_test, resu_02,'测试集ROC Curve')

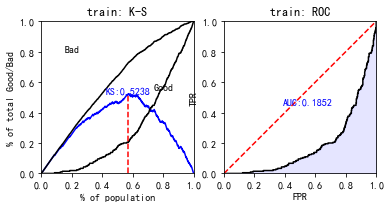

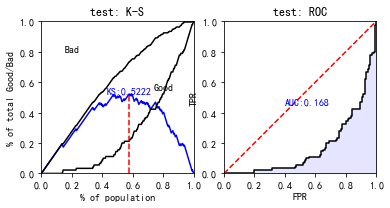

使用perf_eva()函数对模型效果进行计算及可视化,基于预测的概率值和label值,提供KS(kolmogorov-smirnow), ROC, lift以及precision-recall四种评估指标:

#使用sc自带的 train_perf = sc.perf_eva(y_train, train_pred, title = "train") test_perf = sc.perf_eva(y_test, test_pred, title = "test")

这个auc看着好奇怪啊,估计是预测数据取预测good的概率,下面我们更改一下:

train_pred = lr.predict_proba(X_train)[:,0] test_pred = lr.predict_proba(X_test)[:,0] train_perf = sc.perf_eva(y_train, train_pred, title = "train") test_perf = sc.perf_eva(y_test, test_pred, title = "test")

现在数据就正常多了。

七、评分卡

scorecard()函数,生成的结果为各变量名及其分箱、对应得分组成的字典

def scorecard(bins, model, xcolumns, points0=600, odds0=1/19, pdo=50, basepoints_eq0=False, digits=0)

各参数含义如下:

- bins:由`woebin`得到的分箱信息;

- model:LogisticRegression模型对象;

- points0:基准分数,默认值为600;

- odds0: 基准 Odds(好坏比),与真实违约概率对应,可换算得到违约概率,Odds = p/(1-p)。默认值为 1/19;

- pdo: Points toDouble theOdds,即Odds变成2倍时,所增加的信用分。默认值为50;

- basepoints_eq0:设置是否要把basepoints均分给每个变量的得分,默认为False,即不进行均分。但大多数评分卡倾向于所有分数均为正数,所以可手动改为True。

使用sklearn的逻辑回归这样转换

dat.creditability.value_counts(normalize=True) ''' good 0.7 bad 0.3 ''' card = sc.scorecard(bins_adj, lr, X_train.columns,odds0=0.3/0.7)

使用statsmodels.api,则需要提供lr.coef_,lr.intercept_ 这两个系数

import numpy as np result.intercept_ = np.array([result.params.const]) result.coef_ = np.array([result.params[1:].values]) card1 = sc.scorecard(bins_adj, result,model_cols,odds0=0.3/0.7)

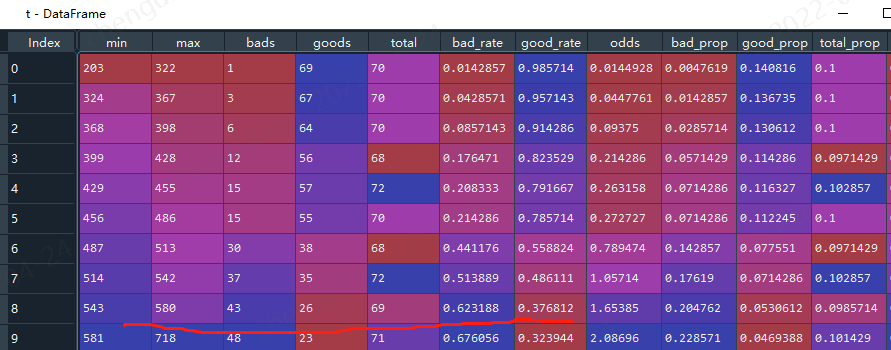

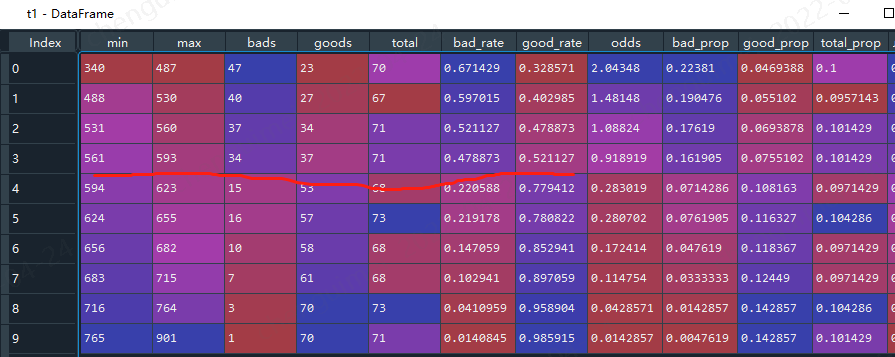

转换之后,我们还需要验证,基础分为600,那么当分数等于600时候,逾期率就应该是0.3,本次使用toad的ks函数验证

#首先转换分数 #sc内置 train_score = sc.scorecard_ply(train, card, print_step=0) test_score = sc.scorecard_ply(test, card, print_step=0) import toad t = toad.metrics.KS_bucket(train_score.iloc[:,0].values, target_train, bucket=10, method = 'quantile') #statsmodels train_score_01 = sc.scorecard_ply(train, card1, print_step=0) test_score_01 = sc.scorecard_ply(test, card1, print_step=0) t1 = toad.metrics.KS_bucket(train_score_01.iloc[:,0].values, target_train, bucket=10, method = 'quantile')

使用sklearn的看着好变扭啊,最终是分数越高,逾期概率越高,

上面二者看着基本符合分数等于600时候,逾期率是0.3。

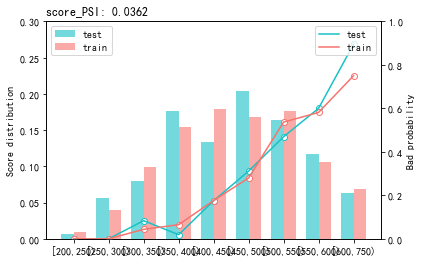

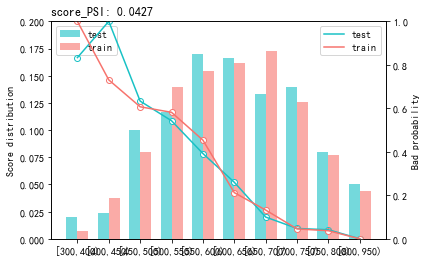

最后用perf_psi()得到该评分卡在测试数据集上的表现

#sc sc.perf_psi( score = {'train':train_score, 'test':test_score}, label = {'train':target_train, 'test':target_test} ) #statsmodels sc.perf_psi( score = {'train':train_score_01, 'test':test_score_01}, label = {'train':target_train, 'test':target_test} )

浙公网安备 33010602011771号

浙公网安备 33010602011771号