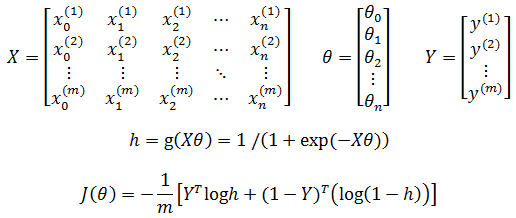

ML(4)——逻辑回归

Logistic Regression虽然名字里带“回归”,但是它实际上是一种分类方法,“逻辑”是Logistic的音译,和真正的逻辑没有任何关系。

模型

线性模型

由于逻辑回归是一种分类方法,所以我们仍然以最简的二分类为例。与感知机不同,对于逻辑回归的分类结果,y ∈ {0, 1},我们需要找到最佳的hθ(x)拟合数据。

这里容易联想到线性回归。线性回归也可以用于分类,但是很多时候,尤其是二分类的时候,线性回归并不能很好地工作,因为分类不是连续的函数,其结果只能是固定的离散值。设想一下有线性回归得到的拟合曲线hθ(x),当x→∞时,有可能y→∞,这就无法对y ∈ {0, 1}进行有效解释。

对于二分类,逻辑回归的目的是找到一个函数,使得无论x取何值,都有:

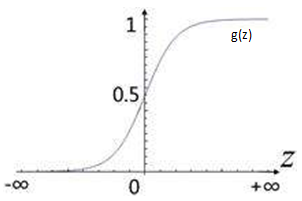

满足这个式子的典型函数是sigmoid函数,也称为logistic函数:

在sigmoid函数g(z)中:

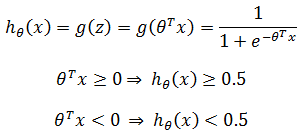

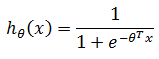

现在,将hθ(x)赋予sigmoid函数g(z)的特性:

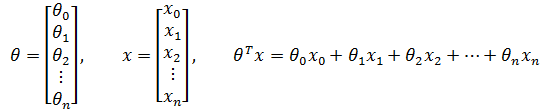

其中:

最终,逻辑回归的模型函数:

假设给定一些输入,现在需要根据逻辑回归模型预测肿瘤是否是良性,最终得到hθ(x) = 0.8,可以用概率表述:

上式表示在当前输入下,y=1的概率是0.8,y=0的概率是0.2,因为是分类,所以判断y = 1。

需要注意的是,sigmoid函数不是样本点的分隔曲线,它表示的是逻辑回归的测结果;θTx才是分隔曲线,它将样本点分为θTx ≥ 0和θTx < 0两部分:

分隔曲线

Sigmoid函数,最终模型

由此看来,逻辑回归的线性模型同样是找到最佳的θ,使两类样本点分离,这就在很大程度上和感知机相似。

多项式模型

直观地看,线性模型的决策边界就是将两类样本点分离开的分隔曲线,我们之前已经多次接触过,只是没有给它起一个专业的名字。假设在一个模型中,hθ(x) = g(θ0 + θ1x1 + θ2x2) = g(-3 + x1 + x2),那么决策边界就是 -3 + x1 + x2 = 0:

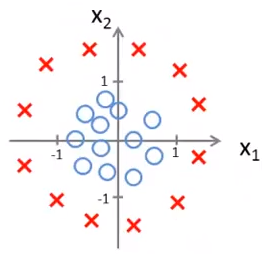

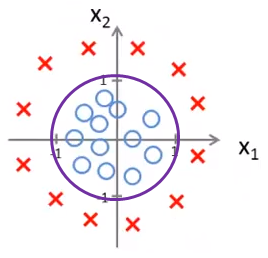

很多时候,直线并不能很好地作为决策边界,如下图所示:

此时需要使用多项式模型添加更多的特征:

这相当于添加了两个新的特征:

深入了解不同函数的特征有助于选择正确的模型。添加的特征越多,曲线越复杂,对训练样本的拟合度越高,同时也更容易导致过拟合而丧失泛化性:

关于过拟合及其处理,可参考《ML(附录3)——数据拟合和正则化》。

多分类

我们已经知道了二分类的模型,然而实际问题中往往不只是二分类,那么逻辑回归如何处理多分类呢?

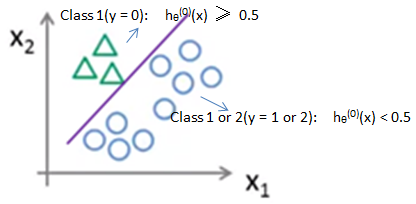

一种可行的方法就是化繁为简,将多分类转换为二分类:

如上图所示,三分类转换为三个二分类,其中上标表示分类的类别:

对于输入x,其预测结果是所有hθ(x)中值最大的一个。对于最后的预测结论,以上面的三分类为例,如果输入一个标签为2的特征集,对于hθ(0)(x) 来说,hθ(0)(x) < 0.5:

对于hθ(1)(x) 来说,hθ(1)(x) < 0.5:

对于hθ(3)(x) 来说,hθ(3)(x) ≥ 0.5:

因此,对于输入x,其预测结果是所有hθ(x)中值最大的一个。至于每个样本标签值是多少,无所谓了,在训练每个hθ(i)(x)前,都需要把y(i) 转换为1,其余转换为0。

在上面的图组中也可以看出,对于有k个标签的多分类,需要训练k个不同的逻辑回归模型。

学习策略

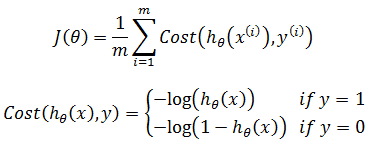

在感知机中,模型函数使用了sign,由于sign是阶跃函数,不易优化,所以为了求得损失函数,我们使用函数间隔进行了一系列转换。对于逻辑回归,由于函数本身是连续曲线,所以不会存在这样的问题,其J(θ)使用对数损失函数。对数损失函数的原型:

将其用在逻辑回归上:

这里的对数是以e为底的对数,即:

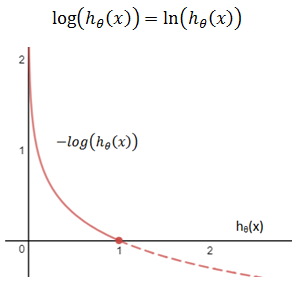

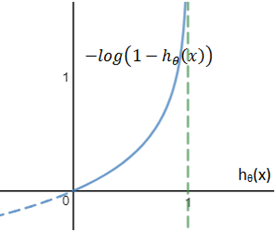

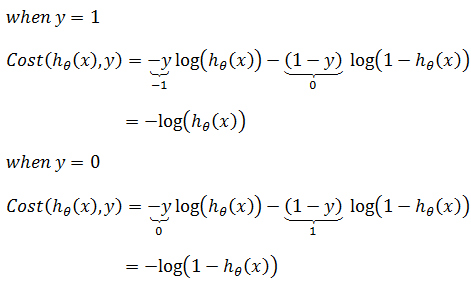

注意,0 < hθ(x) < 1。上图是y = 1时的costfunction,可以看到,当hθ(x)→1时,Cost(hθ(x), y)→0;当hθ(x)→0时,Cost(hθ(x),y)→∞。也就是说当分类是1时,sigmoid的值越接近于1,损失值越小;sigmoid的值越接近于0,损失值越大。损失值越大,分类点越接近决策面,其分类越模糊。与此类似,下图是 y = 0时的cost function:

Cost function可以把y = 1和y=1两种情况合并到一起:

理解这种形式需要再次将y分开:

最后得到J(θ)的最终形式:

注意,这里hθ(x)是sigmoid函数:

如果写成矩阵的形式:

上式中,hθ(x)的操作对应矩阵中的每个元素,1-Y,log hθ(x)也一样,可参照后文的代码实现来理解。

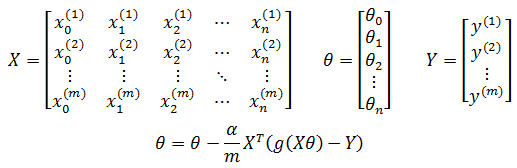

算法

与之前的算法一样,我们的目的是找到最佳的θ使得J(θ)最小化,将求解θ转换为最优化问题,即:

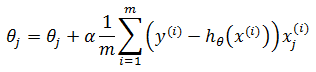

梯度下降

梯度下降是一个适用范围很广的方法,这里同样可以使用梯度下降求解θ:

关于梯度下降的更多内容可参考《ML(附录1)——梯度下降》。

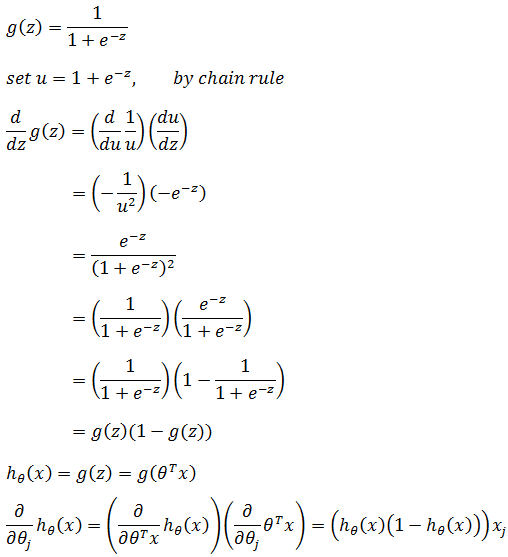

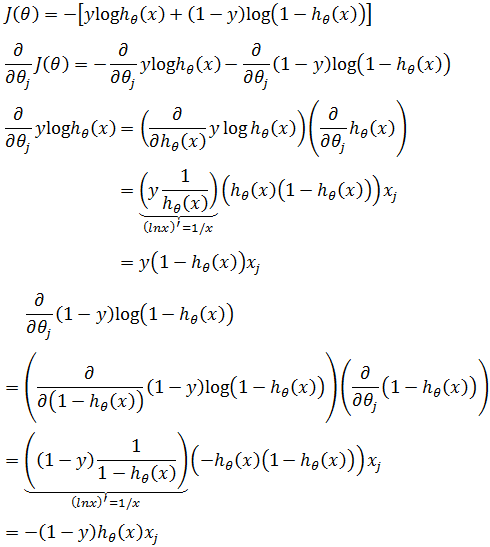

在对J(θ)求偏导时先做一些准备工作,计算sigmoid函数的导数(关于偏导和一元函数的导数,可参考《多变量微积分》和《单变量微积分》的相关章节):

现在计算m=1时J(θ)的偏导,此时可以删除上标:

推广到m个样本:

在《机器学习实战》中提到对极大似然数使用梯度上升求最大值,最后得到:

这和对损失函数采用梯度下降求最小值是一样的,因为损失函数使用了似然数的负数形式,Cost(X, Y) = -logP(Y|X),所以对-logP(Y|X)梯度下降和对+logP(Y|X)梯度上升将得到同样的结果。

对于多项式模型,需要预先添加特征,使得每个θj都有唯一的xj对应:

如果用矩阵表示:

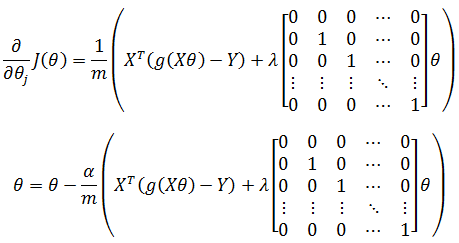

在此基础上使用L2正则化(关于正则化,可参考《ML(附录3)——过拟合与欠拟合》):

代码实现

ex2data1.txt:

1 34.62365962451697,78.0246928153624,0 2 30.28671076822607,43.89499752400101,0 3 35.84740876993872,72.90219802708364,0 4 60.18259938620976,86.30855209546826,1 5 79.0327360507101,75.3443764369103,1 6 45.08327747668339,56.3163717815305,0 7 61.10666453684766,96.51142588489624,1 8 75.02474556738889,46.55401354116538,1 9 76.09878670226257,87.42056971926803,1 10 84.43281996120035,43.53339331072109,1 11 95.86155507093572,38.22527805795094,0 12 75.01365838958247,30.60326323428011,0 13 82.30705337399482,76.48196330235604,1 14 69.36458875970939,97.71869196188608,1 15 39.53833914367223,76.03681085115882,0 16 53.9710521485623,89.20735013750205,1 17 69.07014406283025,52.74046973016765,1 18 67.94685547711617,46.67857410673128,0 19 70.66150955499435,92.92713789364831,1 20 76.97878372747498,47.57596364975532,1 21 67.37202754570876,42.83843832029179,0 22 89.67677575072079,65.79936592745237,1 23 50.534788289883,48.85581152764205,0 24 34.21206097786789,44.20952859866288,0 25 77.9240914545704,68.9723599933059,1 26 62.27101367004632,69.95445795447587,1 27 80.1901807509566,44.82162893218353,1 28 93.114388797442,38.80067033713209,0 29 61.83020602312595,50.25610789244621,0 30 38.78580379679423,64.99568095539578,0 31 61.379289447425,72.80788731317097,1 32 85.40451939411645,57.05198397627122,1 33 52.10797973193984,63.12762376881715,0 34 52.04540476831827,69.43286012045222,1 35 40.23689373545111,71.16774802184875,0 36 54.63510555424817,52.21388588061123,0 37 33.91550010906887,98.86943574220611,0 38 64.17698887494485,80.90806058670817,1 39 74.78925295941542,41.57341522824434,0 40 34.1836400264419,75.2377203360134,0 41 83.90239366249155,56.30804621605327,1 42 51.54772026906181,46.85629026349976,0 43 94.44336776917852,65.56892160559052,1 44 82.36875375713919,40.61825515970618,0 45 51.04775177128865,45.82270145776001,0 46 62.22267576120188,52.06099194836679,0 47 77.19303492601364,70.45820000180959,1 48 97.77159928000232,86.7278223300282,1 49 62.07306379667647,96.76882412413983,1 50 91.56497449807442,88.69629254546599,1 51 79.94481794066932,74.16311935043758,1 52 99.2725269292572,60.99903099844988,1 53 90.54671411399852,43.39060180650027,1 54 34.52451385320009,60.39634245837173,0 55 50.2864961189907,49.80453881323059,0 56 49.58667721632031,59.80895099453265,0 57 97.64563396007767,68.86157272420604,1 58 32.57720016809309,95.59854761387875,0 59 74.24869136721598,69.82457122657193,1 60 71.79646205863379,78.45356224515052,1 61 75.3956114656803,85.75993667331619,1 62 35.28611281526193,47.02051394723416,0 63 56.25381749711624,39.26147251058019,0 64 30.05882244669796,49.59297386723685,0 65 44.66826172480893,66.45008614558913,0 66 66.56089447242954,41.09209807936973,0 67 40.45755098375164,97.53518548909936,1 68 49.07256321908844,51.88321182073966,0 69 80.27957401466998,92.11606081344084,1 70 66.74671856944039,60.99139402740988,1 71 32.72283304060323,43.30717306430063,0 72 64.0393204150601,78.03168802018232,1 73 72.34649422579923,96.22759296761404,1 74 60.45788573918959,73.09499809758037,1 75 58.84095621726802,75.85844831279042,1 76 99.82785779692128,72.36925193383885,1 77 47.26426910848174,88.47586499559782,1 78 50.45815980285988,75.80985952982456,1 79 60.45555629271532,42.50840943572217,0 80 82.22666157785568,42.71987853716458,0 81 88.9138964166533,69.80378889835472,1 82 94.83450672430196,45.69430680250754,1 83 67.31925746917527,66.58935317747915,1 84 57.23870631569862,59.51428198012956,1 85 80.36675600171273,90.96014789746954,1 86 68.46852178591112,85.59430710452014,1 87 42.0754545384731,78.84478600148043,0 88 75.47770200533905,90.42453899753964,1 89 78.63542434898018,96.64742716885644,1 90 52.34800398794107,60.76950525602592,0 91 94.09433112516793,77.15910509073893,1 92 90.44855097096364,87.50879176484702,1 93 55.48216114069585,35.57070347228866,0 94 74.49269241843041,84.84513684930135,1 95 89.84580670720979,45.35828361091658,1 96 83.48916274498238,48.38028579728175,1 97 42.2617008099817,87.10385094025457,1 98 99.31500880510394,68.77540947206617,1 99 55.34001756003703,64.9319380069486,1 100 74.77589300092767,89.52981289513276,1

Octave

%% Machine Learning Online Class - Exercise 2: Logistic Regression

%

% Instructions

% ------------

%

% This file contains code that helps you get started on the logistic

% regression exercise. You will need to complete the following functions

% in this exericse:

%

% sigmoid.m

% costFunction.m

% predict.m

% costFunctionReg.m

%

% For this exercise, you will not need to change any code in this file,

% or any other files other than those mentioned above.

%

%% Initialization

clear ; close all; clc

%% Load Data

% The first two columns contains the exam scores and the third column

% contains the label.

data = load('ex2data1.txt');

X = data(:, [1, 2]); y = data(:, 3);

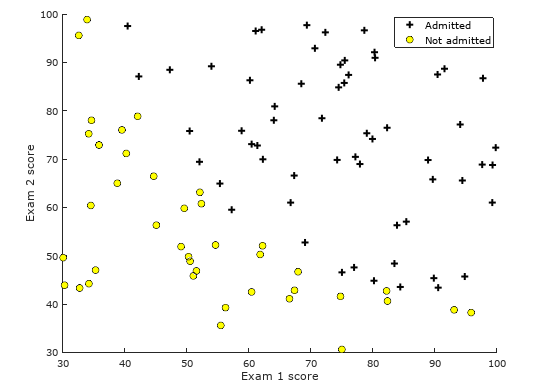

%% ==================== Part 1: Plotting ====================

% We start the exercise by first plotting the data to understand the

% the problem we are working with.

fprintf(['Plotting data with + indicating (y = 1) examples and o ' ...

'indicating (y = 0) examples.\n']);

plotData(X, y);

% Put some labels

hold on;

% Labels and Legend

xlabel('Exam 1 score')

ylabel('Exam 2 score')

% Specified in plot order

legend('Admitted', 'Not admitted')

hold off;

fprintf('\nProgram paused. Press enter to continue.\n');

pause;

%% ============ Part 2: Compute Cost and Gradient ============

% In this part of the exercise, you will implement the cost and gradient

% for logistic regression. You neeed to complete the code in

% costFunction.m

% Setup the data matrix appropriately, and add ones for the intercept term

[m, n] = size(X);

% Add intercept term to x and X_test

X = [ones(m, 1) X];

% Initialize fitting parameters

initial_theta = zeros(n + 1, 1);

% Compute and display initial cost and gradient

[cost, grad] = costFunction(initial_theta, X, y);

fprintf('Cost at initial theta (zeros): %f\n', cost);

fprintf('Expected cost (approx): 0.693\n');

fprintf('Gradient at initial theta (zeros): \n');

fprintf(' %f \n', grad);

fprintf('Expected gradients (approx):\n -0.1000\n -12.0092\n -11.2628\n');

% Compute and display cost and gradient with non-zero theta

test_theta = [-24; 0.2; 0.2];

[cost, grad] = costFunction(test_theta, X, y);

fprintf('\nCost at test theta: %f\n', cost);

fprintf('Expected cost (approx): 0.218\n');

fprintf('Gradient at test theta: \n');

fprintf(' %f \n', grad);

fprintf('Expected gradients (approx):\n 0.043\n 2.566\n 2.647\n');

fprintf('\nProgram paused. Press enter to continue.\n');

pause;

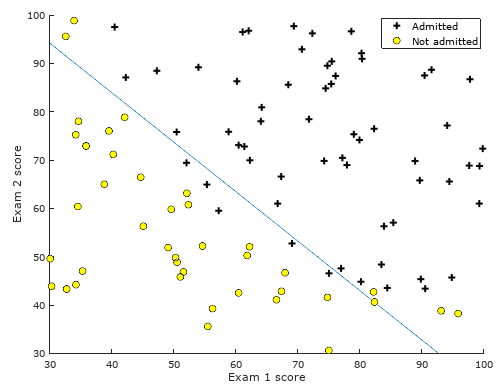

%% ============= Part 3: Optimizing using fminunc =============

% In this exercise, you will use a built-in function (fminunc) to find the

% optimal parameters theta.

% Set options for fminunc

options = optimset('GradObj', 'on', 'MaxIter', 400);

% Run fminunc to obtain the optimal theta

% This function will return theta and the cost

[theta, cost] = fminunc(@(t)(costFunction(t, X, y)), initial_theta, options);

% Print theta to screen

fprintf('Cost at theta found by fminunc: %f\n', cost);

fprintf('Expected cost (approx): 0.203\n');

fprintf('theta: \n');

fprintf(' %f \n', theta);

fprintf('Expected theta (approx):\n');

fprintf(' -25.161\n 0.206\n 0.201\n');

% Plot Boundary

plotDecisionBoundary(theta, X, y);

% Put some labels

hold on;

% Labels and Legend

xlabel('Exam 1 score')

ylabel('Exam 2 score')

% Specified in plot order

legend('Admitted', 'Not admitted')

hold off;

fprintf('\nProgram paused. Press enter to continue.\n');

pause;

%% ============== Part 4: Predict and Accuracies ==============

% After learning the parameters, you'll like to use it to predict the outcomes

% on unseen data. In this part, you will use the logistic regression model

% to predict the probability that a student with score 45 on exam 1 and

% score 85 on exam 2 will be admitted.

%

% Furthermore, you will compute the training and test set accuracies of

% our model.

%

% Your task is to complete the code in predict.m

% Predict probability for a student with score 45 on exam 1

% and score 85 on exam 2

prob = sigmoid([1 45 85] * theta);

fprintf(['For a student with scores 45 and 85, we predict an admission ' ...

'probability of %f\n'], prob);

fprintf('Expected value: 0.775 +/- 0.002\n\n');

% Compute accuracy on our training set

p = predict(theta, X);

fprintf('Train Accuracy: %f\n', mean(double(p == y)) * 100);

fprintf('Expected accuracy (approx): 89.0\n');

fprintf('\n');

plotData.m

function plotData(X, y) %PLOTDATA Plots the data points X and y into a new figure % PLOTDATA(x,y) plots the data points with + for the positive examples % and o for the negative examples. X is assumed to be a Mx2 matrix. % Create New Figure figure; hold on; % Instructions: Plot the positive and negative examples on a % 2D plot, using the option 'k+' for the positive % examples and 'ko' for the negative examples. pos = find(y==1); neg = find(y == 0); plot(X(pos, 1), X(pos, 2), 'k+','LineWidth', 2, 'MarkerSize', 7); plot(X(neg, 1), X(neg, 2), 'ko', 'MarkerFaceColor', 'y', 'MarkerSize', 7); hold off; end

sigmoid.m

function g = sigmoid(z) %SIGMOID Compute sigmoid function % g = SIGMOID(z) computes the sigmoid of z. % You need to return the following variables correctly g = ones(size(z)) ./ (1 + exp(-1 * z)); end

costFunction.m

function [J, grad] = costFunction(theta, X, y) %COSTFUNCTION Compute cost and gradient for logistic regression % J = COSTFUNCTION(theta, X, y) computes the cost of using theta as the % parameter for logistic regression and the gradient of the cost % w.r.t. to the parameters. % Initialize some useful values m = length(y); % number of training examples % You need to return the following variables correctly J = 0; grad = zeros(size(theta)); % Instructions: Compute the cost of a particular choice of theta. % You should set J to the cost. % Compute the partial derivatives and set grad to the partial % derivatives of the cost w.r.t. each parameter in theta % % Note: grad should have the same dimensions as theta % % % use intrator to compue J % for i = 1:m % theta_X = X(i,:) * theta; % h = 1 / (1 + exp(-1 * theta_X)); % J += y(i) * log(h) + (1 - y(i)) * log(1 - h); % end % J /= -1 * m; % use matrix to compute gradient h = sigmoid(X * theta); J = (y' * log(h) + (1 - y)' * log(1 - h)) / (-1 * m); #J /= -1 * m; grad = X' * (h - y) / m; end

Python

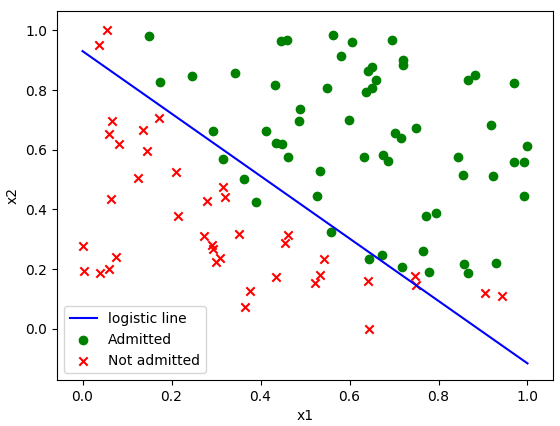

1 from __future__ import division 2 import numpy as np 3 import random 4 import matplotlib.pyplot as plt 5 6 def train(X, Y, iterateNum=10000000, alpha=0.003): 7 ''' 8 :param X: 训练样本的特征集 9 :param Y: 训练样本的标签 10 :param iterateNum: 梯度下降的迭代次数 11 :param alpha: 学习率 12 :return:theta 13 ''' 14 m, n = np.shape(X) 15 theta = np.zeros((n + 1, 1)) 16 # 在第一列添加x0 17 X_new = np.c_[np.ones(m), X] 18 19 for i in range(iterateNum): 20 m = np.shape(X_new)[0] 21 h = h_function(X_new, theta) 22 theta -= alpha * (np.dot(X_new.T, h - Y) / m) 23 24 if i % 100000 == 0: 25 print('\t---------iter=' + str(i) + ', J(θ)=' + str(J_function(X_new, Y, theta))) 26 27 print( str(J_function(X_new, Y, theta))) 28 return theta 29 30 def h_function(X, theta): 31 return sigmoid(np.dot(X, theta)) 32 33 def sigmoid(X): 34 return 1 / (1 + np.exp(-X )) 35 36 # 计算J(θ) 37 def J_function(X, Y, theta): 38 h = h_function(X, theta) 39 J_1 = np.dot(Y.T, np.log(h)) 40 J_2 = np.dot(1 - Y.T, np.log(1 - h)) 41 m = np.shape(X)[0] 42 J = (-1 / m) * (J_1 + J_2) 43 44 return J 45 46 def predict(x, theta): 47 if h_function(x, theta) >= 0.5: 48 return 1 49 else: 50 return 0 51 52 # 归一化处理 53 def normalization(X): 54 m, n = np.shape(X) 55 X_new = np.zeros((m, n)) 56 57 for j in range(n): 58 max = np.max(X[:,j]) 59 min = np.min(X[:,j]) 60 d_value = max - min 61 for i in range(m): 62 X_new[i, j] = (X[i, j] - min) / d_value 63 64 return X_new 65 66 def plot_datas(X, Y, theta): 67 plt.figure() 68 69 # 绘制分隔直线 g = 0 70 x1 = [0, 1] 71 x2 = [(-1 / theta[2]) * (theta[0] + theta[1] * x1[0]), 72 (-1 / theta[2]) * (theta[0] + theta[1] * x1[1])] 73 plt.xlabel('x1') 74 plt.ylabel('x2') 75 76 plt.plot(x1, x2, color='b') 77 78 # 绘制数据点 79 admit_x1, admit_x2 = [],[] 80 not_admit_x1, not_admit_x2 = [],[] 81 for i in range(len(X)): 82 if (Y[i] == 1): 83 admit_x1.append(X[i][0]) 84 admit_x2.append(X[i][1]) 85 else: 86 not_admit_x1.append(X[i][0]) 87 not_admit_x2.append(X[i][1]) 88 89 plt.scatter(admit_x1, admit_x2, color='g') 90 plt.scatter(not_admit_x1, not_admit_x2, marker='x', color='r') 91 92 plt.legend(['logistic line', 'Admitted', 'Not admitted']) 93 plt.show() 94 95 if __name__ == '__main__': 96 train_datas = np.loadtxt('ex2data1.txt', delimiter=',') 97 X = train_datas[:,[0, 1]] 98 X = normalization(X) 99 Y = train_datas[:,[2]] 100 theta = train(X, Y) 101 102 print(theta) 103 plot_datas(X, Y, theta)

对于样本数据,上面的梯度下降并不是非常有效,无论是否预处理数据(归一化或其他方法),都必须反复调整学习率和迭代次数。如果学习率过大,算法将不会收敛;如果过小,算法收敛的十分缓慢,需要增加迭代次数。代码中的参数最终将使算法收敛于0.203。

Sklearn

1 from sklearn.linear_model import LogisticRegression 2 import numpy as np 3 4 if __name__ == '__main__': 5 train_datas = np.loadtxt("ex2data1.txt", delimiter=',') 6 X_train = train_datas[:,[0, 1]] 7 Y_train = train_datas[:,[2]] 8 9 logistic = LogisticRegression() 10 logistic.fit(X_train, Y_train) 11 12 theta = [logistic.intercept_[0], logistic.coef_[0]] 13 print(theta)

参考:

Ng视频《Logistic Regression》

周志华《机器学习》

《机器学习导论》

Peter Flach《机器学习》

作者:我是8位的

出处:http://www.cnblogs.com/bigmonkey

本文以学习、研究和分享为主,如需转载,请联系本人,标明作者和出处,非商业用途!

扫描二维码关注公众号“我是8位的”

浙公网安备 33010602011771号

浙公网安备 33010602011771号