# 预测财政收入,2014、2015(y) 神经网络,用到data_1

import os

import numpy as np

import pandas as pd

from sklearn.linear_model import LassoLars

from sklearn.linear_model import Lasso

from keras.models import Sequential

from keras.layers.core import Dense, Activation

import matplotlib.pyplot as plt

filepath = "C:/Users/Lenovo/Desktop/data(1).csv"

data = pd.read_csv(filepath)

l=['x3','x5','x7','x11','y']

data_1=data[l].copy()

print(data_1)

data_1.index = range(1994,2014)

data_train=data_1.loc[range(1994,2014)].copy()

data_train_normal=(data_train-data_train.mean())/data_train.std() # 数据标准化,按列索引(列名)计算

y_class=l.pop()

x_train=data_train_normal[l] # 特征数据提取

y_train=data_train_normal[y_class] #标签数据提取

# 构造神经网络模型

nn_model=Sequential() # create the NN-model

nn_model.add(Dense(input_dim=4,units=12)) #

nn_model.add(Activation('relu')) #

nn_model.add(Dense(1)) # 最后一层不激活,直接输出。或者说把激活函数看作f(x)=x

nn_model.compile(loss='mean_squared_error', optimizer='adam',metrics=['accuracy'])

#net.fit(train_data[:,:3],train_data[:,3],epochs=10,batch_size=1)#keras 2.0之前版本

nn_model.fit(x_train,y_train,epochs=1000,batch_size=16,verbose=1)#keras 2.0,推荐,verbose=0,不显示过程,默认等于1显示过程

# 预测,还原结果

x=((data_1[l]-data_train[l].mean())/data_train[l].std()).values

data_1['y_pred']=nn_model.predict(x)*data_train['y'].std()+data_train['y'].mean()

# GM模型,预测

def GM11(x0): #自定义灰色预测函数

x1 = x0.cumsum() #1-AGO序列

x1 = pd.DataFrame(x1)

z1 = (x1 + x1.shift())/2.0 #紧邻均值(MEAN)生成序列

z1 = z1[1:].values.reshape((len(z1)-1,1)) # 转成矩阵

B = np.append(-z1, np.ones_like(z1), axis = 1) # 列合并-z1和形状同z1的1值矩阵 19X2

Yn = x0[1:].reshape((len(x0)-1, 1)) # 转成矩阵 19

[[a],[b]] = np.dot(np.dot(np.linalg.inv(np.dot(B.T, B)), B.T), Yn) #计算参数,基于矩阵运算,np.dot矩阵相乘,np.linalg.inv矩阵求逆

f = lambda k: (x0[0]-b/a)*np.exp(-a*(k-1))-(x0[0]-b/a)*np.exp(-a*(k-2)) #还原值

delta = np.abs(x0 - np.array([f(i) for i in range(1,len(x0)+1)])) # 残差绝对值序列

C = delta.std()/x0.std()

P = 1.0*(np.abs(delta - delta.mean()) < 0.6745*x0.std()).sum()/len(x0)

return f, a, b, x0[0], C, P #返回灰色预测函数、a、b、首项、方差比、小残差概率

#ax1=plt.subplot(211)

#ax1.plot(data_1['y'],'b-o')

#ax1.legend()

#ax2=plt.subplot(212)

#ax2.plot(data_1['y_pred'],'r-*')

#ax2.legend()

plt.plot(data_1['y'],'b-o')

plt.plot(data_1['y_pred'],'r-*')

plt.legend()

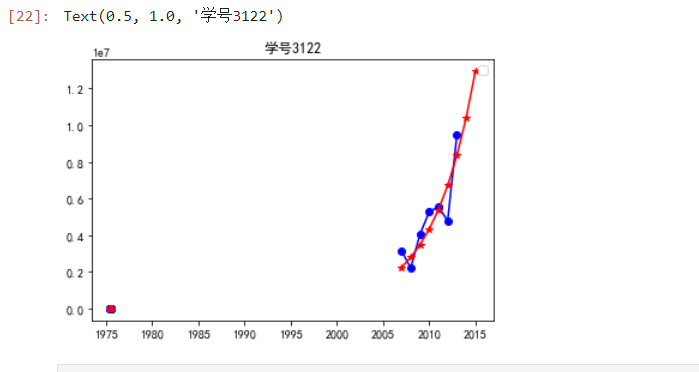

# # 政府性基金收入采用GM11预测2006-2015年份收入,并和原值2006-2013比较

x0 = np.array([3152063, 2213050, 4050122, 5265142,5556619, 4772843,9463330])

f, a, b, x00, C, P = GM11(x0) # 得到预测函数f,可计算接下来预测值(和序号相关,按序预测)

len(x0)

p=pd.DataFrame(x0,index=range(2007,2014),columns=['y']) # 'y'要带上中括号

p.loc[2014]=None

p.loc[2015]=None

p['y_pred']=[f(i+1) for i in range(len(p))]

p=p.round(2)

p.index=pd.to_datetime(p.index,format='%Y')

#for i in range(len(p)):

# print(i+1)

plt.plot(p['y'],'b-o')

plt.plot(p['y_pred'],'r-*')

plt.legend()

#plt.show()

plt.rcParams['font.sans-serif']=['SimHei']

plt.rcParams['axes.unicode_minus']=False

plt.plot(data_1['y'],'b-o')

plt.plot(data_1['y_pred'],'r-*')

plt.legend()

# # 政府性基金收入采用GM11预测2006-2015年份收入,并和原值2006-2013比较

x0 = np.array([3152063, 2213050, 4050122, 5265142,5556619, 4772843,9463330])

f, a, b, x00, C, P = GM11(x0) # 得到预测函数f,可计算接下来预测值(和序号相关,按序预测)

len(x0)

p=pd.DataFrame(x0,index=range(2007,2014),columns=['y']) # 'y'要带上中括号

p.loc[2014]=None

p.loc[2015]=None

p['y_pred']=[f(i+1) for i in range(len(p))]

p=p.round(2)

p.index=pd.to_datetime(p.index,format='%Y')

#for i in range(len(p)):

# print(i+1)

plt.plot(p['y'],'b-o')

plt.plot(p['y_pred'],'r-*')

plt.legend()

plt.title('学号3122')