[Machine Learning] Diagnosing Bias vs. Variance

In this section we examine the relationship between the degree of the polynomial d and the underfitting or overfitting of our hypothesis.

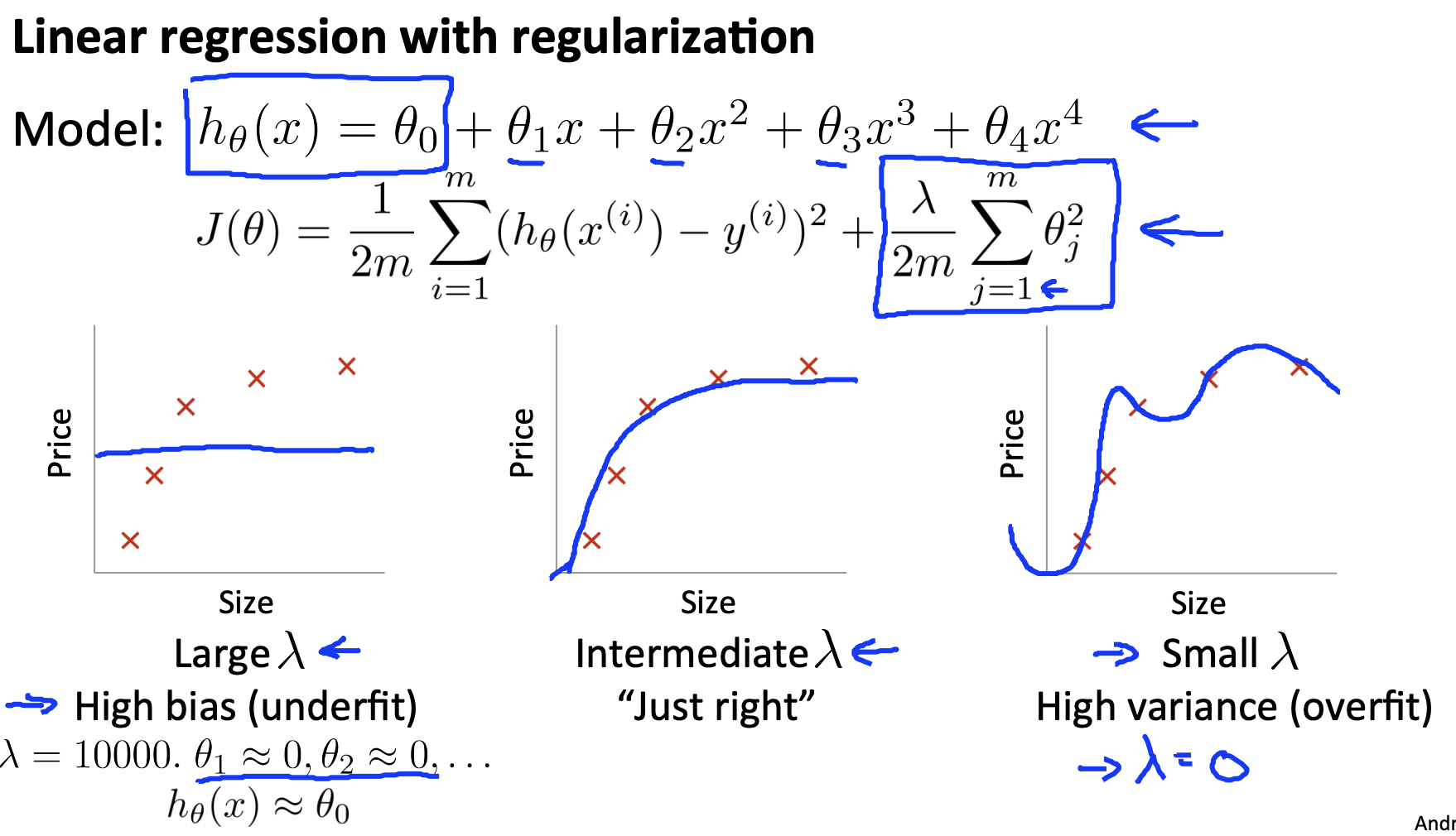

- We need to distinguish whether bias or variance is the problem contributing to bad predictions.

- High bias is underfitting and high variance is overfitting. Ideally, we need to find a golden mean between these two.

The training error will tend to decrease as we increase the degree d of the polynomial.

At the same time, the cross validation error will tend to decrease as we increase d up to a point, and then it will increase as d is increased, forming a convex curve.

Our decision process can be broken down as follows:

- Getting more training examples: Fixes high variance

- Trying smaller sets of features: Fixes high variance

- Adding features: Fixes high bias

- Adding polynomial features: Fixes high bias

- Decreasing λ: Fixes high bias

- Increasing λ: Fixes high variance.

Diagnosing Neural Networks

- A neural network with fewer parameters is prone to underfitting. It is also computationally cheaper.

- A large neural network with more parameters is prone to overfitting. It is also computationally expensive. In this case you can use regularization (increase λ) to address the overfitting.

Using a single hidden layer is a good starting default. You can train your neural network on a number of hidden layers using your cross validation set. You can then select the one that performs best.

Model Complexity Effects:

- Lower-order polynomials (low model complexity) have high bias and low variance. In this case, the model fits poorly consistently.

- Higher-order polynomials (high model complexity) fit the training data extremely well and the test data extremely poorly. These have low bias on the training data, but very high variance.

- In reality, we would want to choose a model somewhere in between, that can generalize well but also fits the data reasonably well.

浙公网安备 33010602011771号

浙公网安备 33010602011771号